Is Tripadvisor (TRIP) Fairly Valued After TheFork Sale And Board Changes?

TripAdvisor, Inc. TRIP | 0.00 |

Tripadvisor (TRIP) is back in focus after shareholders elected Laura Bisesto and Carl Sparks to the board at the June 29 AGM, following the agreed sale of TheFork to American Express for US$700 million.

Against this backdrop, Tripadvisor's 30 day share price return of 13.64% and 90 day share price return of 26.73% suggest momentum has picked up recently, even though the year to date share price return and one year total shareholder return remain in decline.

If Tripadvisor's reshaping has you thinking about other potential ideas, it could be worth scanning companies riding long term themes such as 20 top founder-led companies

With Tripadvisor trading at US$13.75 and an intrinsic value estimate implying a 64% discount, yet sitting only about 4% below the average analyst target, readers have to ask whether there is real upside left or whether the market is already pricing in future growth.

Most Popular Narrative: 4% Undervalued

Against Tripadvisor's last close of $13.75, the most widely followed narrative points to a fair value of $14.38, framing the recent reshaping and TheFork sale within a modest undervaluation based on projected cash flows.

Tripadvisor's focus on scaling its experiences marketplace (Viator and TheFork) takes advantage of global consumer shifts toward experiential travel, as rising international leisure travel from the expanding middle class and a preference for unique experiences are both enlarging the company's addressable market and supporting sustainable, above-industry growth rates, positively impacting long-term revenue and gross profit.

Want to see what sits underneath that fair value for Tripadvisor? The narrative leans heavily on experiences-led growth, higher margins and a richer earnings profile supported by a higher future profit multiple. Curious which specific revenue and profit assumptions need to land for that to hold up.

Result: Fair Value of $14.38 (UNDERVALUED)

However, Tripadvisor still faces pressure from weaker organic traffic in its core business and rising competition, which could weigh on revenue quality and margins if not addressed.

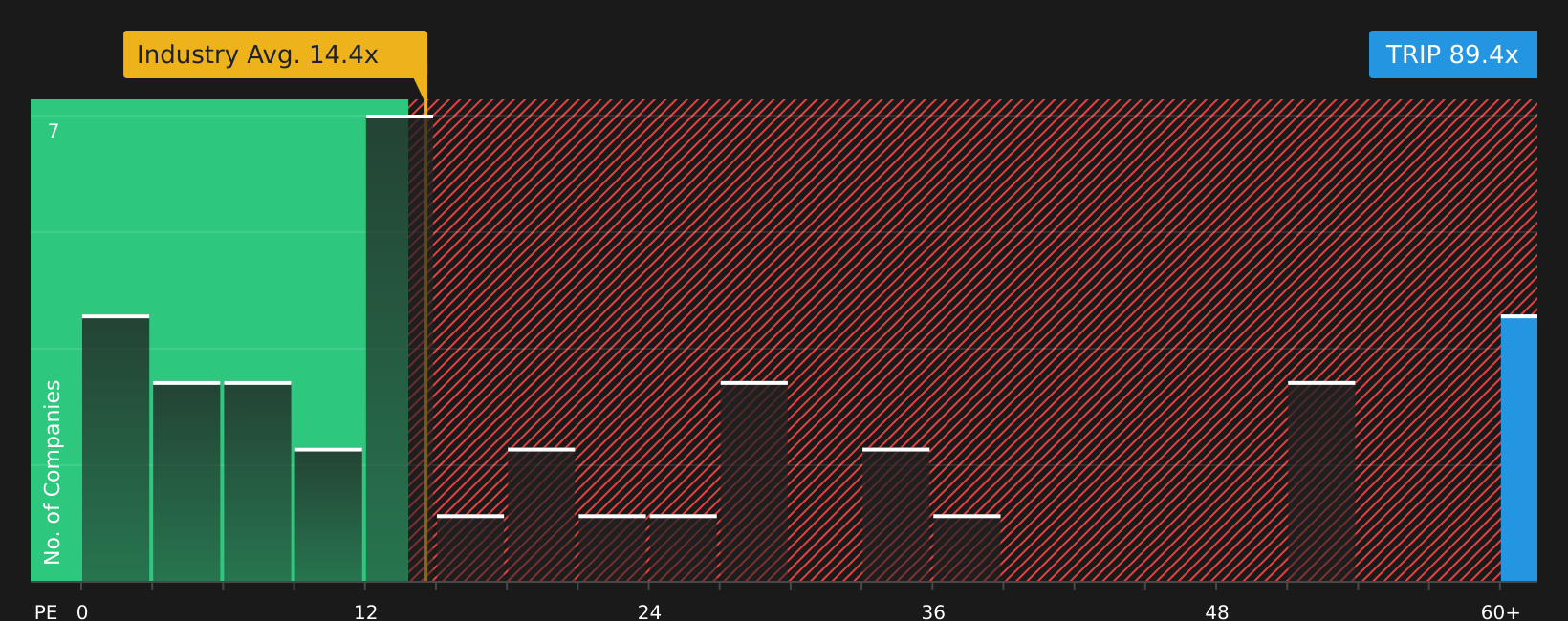

Another View: Tripadvisor Looks Expensive On Earnings

The first narrative around Tripadvisor leans on a fair value of $14.38 that points to modest undervaluation. On P/E though, the picture is very different, with the stock on 86x earnings compared with 20.1x for peers and 14.2x for the wider US Interactive Media and Services industry, while the fair ratio sits at 28x. That gap suggests a lot of optimism is already in the price, so the question is whether you are more comfortable with the cash flow story or the earnings multiples.

Next Steps

Seen enough conflicting signals around Tripadvisor to be unsure which side you land on? Act quickly by checking the full picture of potential downsides and upsides through the 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Tripadvisor?

If Tripadvisor has sharpened your thinking, do not stop there. Widen your watchlist now with stocks that match your preferred mix of value, quality and resilience.

- Target potential mispricings by scanning companies that currently look out of favor but are financially robust using the 41 high quality undervalued stocks

- Strengthen your income stream by reviewing companies that combine higher yields with balance sheet support through the 8 dividend fortresses

- Reduce portfolio stress by focusing on companies with steadier risk profiles and sturdier fundamentals via the 73 resilient stocks with low risk scores

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.