Is United Parks & Resorts (PRKS) Fully Priced On Russell Index Removals And Weak Trends?

United Parks & Resorts Inc. PRKS | 0.00 |

Index removals put fresh focus on United Parks & Resorts stock

United Parks & Resorts (PRKS) has just been dropped from several Russell value oriented indexes, a shift that puts fresh attention on how index related fund flows and existing business pressures might intersect for the stock.

For context, United Parks & Resorts shares have been firming in recent months, with a 30 day share price return of 18.81% and a 90 day move of 41.80%. However, the 1 year total shareholder return is slightly down at 1.08% and the 3 year total shareholder return has declined 14.17%. This suggests that recent momentum contrasts with weaker long term outcomes.

If index changes and shifting sentiment have you reassessing your watchlist, it could be a good time to broaden your search with 20 top founder-led companies

Bulls point to United Parks & Resorts' recent share price rebound and solid annual revenue and net income figures, while bears highlight sluggish visitor trends and shrinking returns on capital. So which side does the current valuation actually support?

Most Popular Narrative: 9.9% Overvalued

Compared with United Parks & Resorts' last close at $48.44, the most followed narrative fair value of $44.09 suggests the stock price sits above that estimate, putting extra weight on the assumptions behind its long term story.

Real estate and hotel partnership opportunities centered on valuable, underutilized land holdings (for example, 400 acres adjacent to Orlando parks) have not been fully credited in the current valuation, presenting potential upside via new revenue streams and asset monetization.

Want to understand why this fair value still prices in upside levers like margins and earnings expansion, even with softer growth assumptions and a higher modeled P/E multiple? The full narrative lays out how these moving parts connect into one valuation story that differs from both the DCF output and today’s share price.

Result: Fair Value of $44.09 (OVERVALUED)

However, United Parks & Resorts still faces pressure from softer recurring revenue trends and higher marketing and operating costs, which could challenge the current fair value story.

Another View: DCF Versus United Parks & Resorts Narrative Fair Value

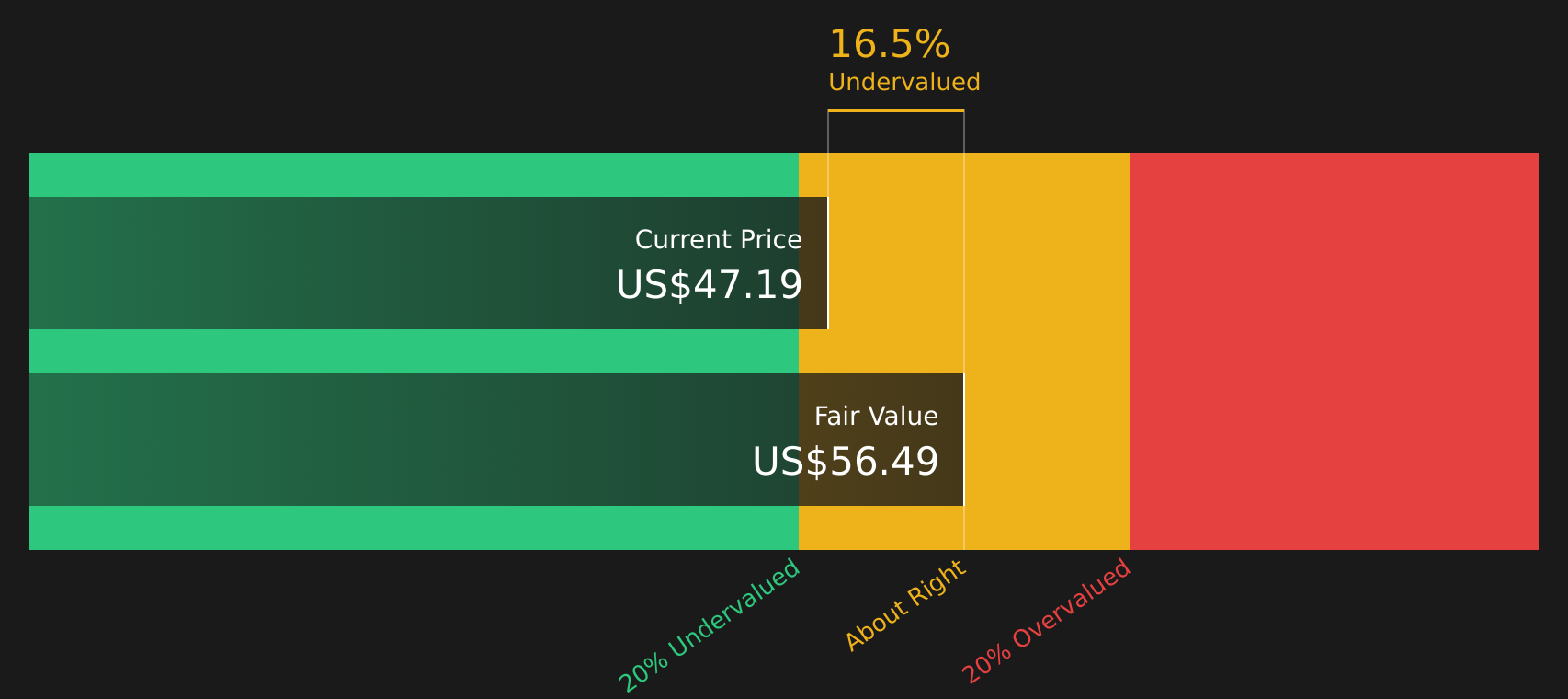

The narrative fair value of $44.09 suggests United Parks & Resorts is overvalued, but our DCF model points the other way, indicating the stock trades about 14% below an estimate of $56.49. When two frameworks disagree this much, which set of assumptions do you trust more?

Next Steps

Given the mixed sentiment around United Parks & Resorts, it makes sense to review the underlying data yourself and move quickly to shape your own view using 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond United Parks & Resorts?

If you stop with United Parks & Resorts, you risk missing other opportunities that could better fit your goals, risk comfort, and return expectations right now.

- Target resilient balance sheets by checking companies in the solid balance sheet and fundamentals stocks screener (47 results)

- Hunt for potential bargains with strong fundamentals using the screener containing 18 high quality undiscovered gems

- Prioritize stability and downside protection by reviewing the 73 resilient stocks with low risk scores

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.