Is Varonis Systems (VRNS) Fully Priced On Its Rebound Or Still A Bargain?

Varonis Systems, Inc. VRNS | 0.00 |

Varonis Systems (VRNS) is back in focus after recent trading, giving investors a fresh chance to reassess this data security software stock in light of its recent share performance and underlying financial profile.

The recent 7.1% 1 day share price return and 13.0% 30 day share price return put Varonis Systems back on traders’ radars, although the 1 year total shareholder return declined 30.1%. This suggests that recent momentum contrasts with a weaker longer term record.

If this rebound in Varonis Systems has you rethinking your tech exposure, it may be a good time to broaden your watchlist with 35 AI small caps.

With Varonis Systems trading near its recent rebound and showing an intrinsic value estimate that is 13.0% below the current share price, investors have to ask: is there real upside left here or is the market already pricing in future growth?

Most Popular Narrative: 3.5% Undervalued

Varonis Systems is trading at $35.03 versus a narrative fair value of $36.32, so this widely followed view sees only modest upside anchored in specific growth and margin assumptions.

Continued SaaS transition and high NRR (notably for SaaS customers), combined with robust upsell momentum across cloud and multi-cloud environments, enhance ARR visibility and predictability. This is described as driving durable earnings and margin expansion as the SaaS mix climbs and operational leverage improves post-transition.

Investments in R&D and expansion of platform capabilities (for example, next-gen database security, MDDR, AI-driven integrations with Microsoft Copilot and OpenAI, cross-platform coverage for AWS, Azure, Snowflake, Databricks, and others) are said to be increasing customer wallet share and accelerating new logo acquisition, supporting consistent top-line and free cash flow growth.

Want to see what underpins that fair value for Varonis Systems? The narrative leans heavily on sustained double digit revenue growth, rising margins, and a rich future earnings multiple. Curious how those ingredients combine to justify only a small discount to today’s price? The full story connects these projections into one tight valuation case.

Result: Fair Value of $36.32 (UNDERVALUED)

However, the Varonis Systems story still depends on its SaaS transition not weighing too heavily on margins, and on larger platforms not squeezing its competitive position.

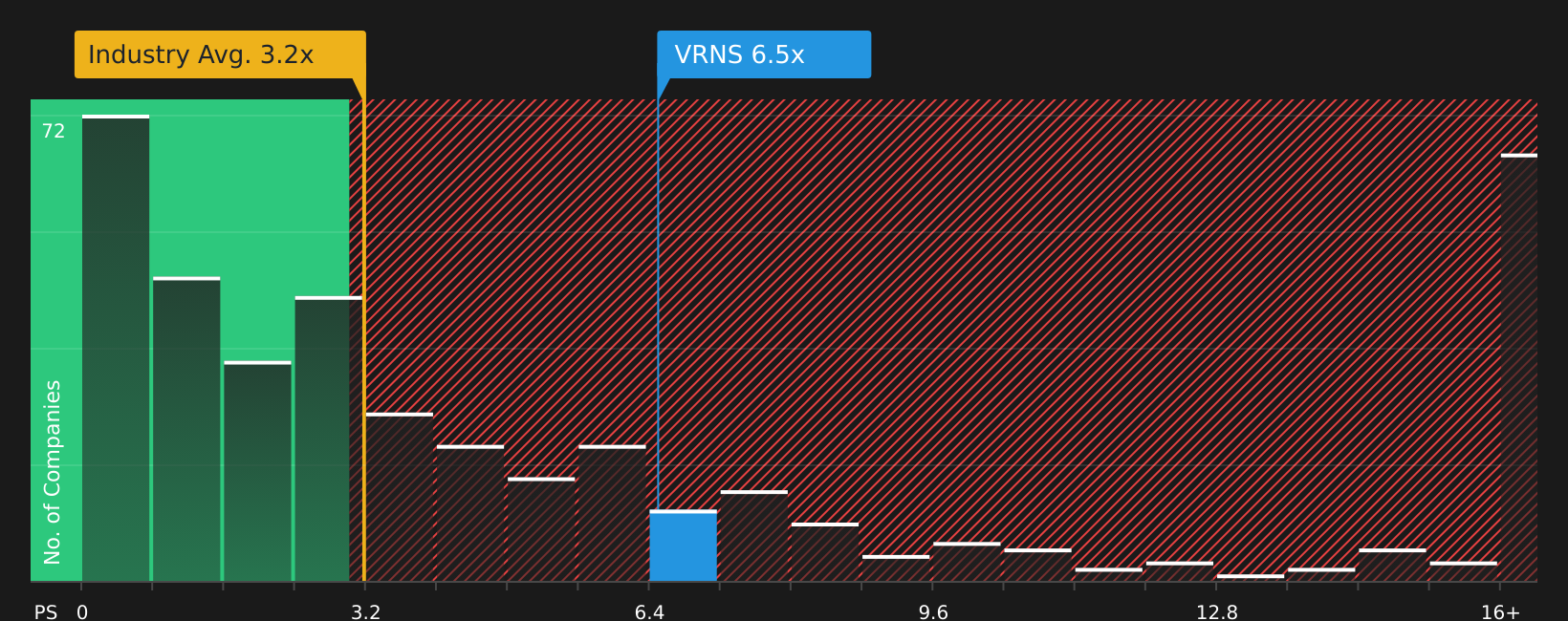

Another View: Varonis Systems Looks Expensive on Sales

While our DCF work suggests Varonis Systems is trading about 13% below an estimated future cash flow value of $40.28, the simple sales based view tells a different story. The current P/S ratio is 6.1x versus 5.3x for peers and 3.2x for the broader US software group.

Our fair ratio sits at 5.2x, which is lower than where the stock trades now. Anyone leaning on sales multiples is therefore looking at a valuation that reflects more optimism than either peers or that fair ratio imply. This raises the question of which lens you trust more when risk and return do not fully line up.

Next Steps

Seeing both optimism and concern around Varonis Systems, it makes sense to review the underlying data yourself and decide how the risk reward trade off looks. To round out your view, take a close look at the balance of potential upside and downside flagged in our 2 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Varonis Systems?

If Varonis Systems has sharpened your thinking, do not stop there. The right mix of other opportunities could make a real difference to your portfolio.

- Target potential mispricings by scanning companies that combine quality with discounts using the 44 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks that feature robust payouts in the 7 dividend fortresses.

- Reduce portfolio stress by focusing on resilient businesses with sturdier risk profiles through the 67 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.