Is Viasat (VSAT) Quietly Rewiring Its Defense-to-Media Mix With New Space Force Contract?

ViaSat, Inc. VSAT | 0.00 |

- In recent months, Viasat secured a multi-year prime contract under the US Space Force’s Protected Tactical SATCOM-Global program and expanded its commercial footprint through new partnerships in streaming, aviation connectivity, and in-flight advertising.

- This combination of long-duration government work and higher-margin commercial opportunities underscores how Viasat is trying to diversify revenue streams across defense and media.

- Next, we’ll examine how the new US Space Force contract could reshape Viasat’s investment narrative around growth, risk, and execution.

The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Viasat Investment Narrative Recap

To own Viasat, you need to believe its mix of government SATCOM contracts and commercial connectivity can eventually support sustainable cash generation despite high capex and competition. The new US Space Force Protected Tactical SATCOM-Global award reinforces the defense connectivity catalyst near term, but it does not remove the key risk that ongoing ViaSat-3 and Inmarsat investments keep leverage and free cash flow under pressure.

The Space Force contract stands out here because it bundles satellite build, launch, ground infrastructure, and five years of operations support, aligning tightly with the core thesis around secure, resilient connectivity. Compared with newer media and advertising partnerships, this program is more directly tied to the defense-driven catalyst that consensus analysts highlight, while also intersecting with the risk that regulatory and technical hurdles could complicate future GEO deployments.

Yet beneath this encouraging contract win, investors should be aware that growing regulatory scrutiny over new satellite launches could still...

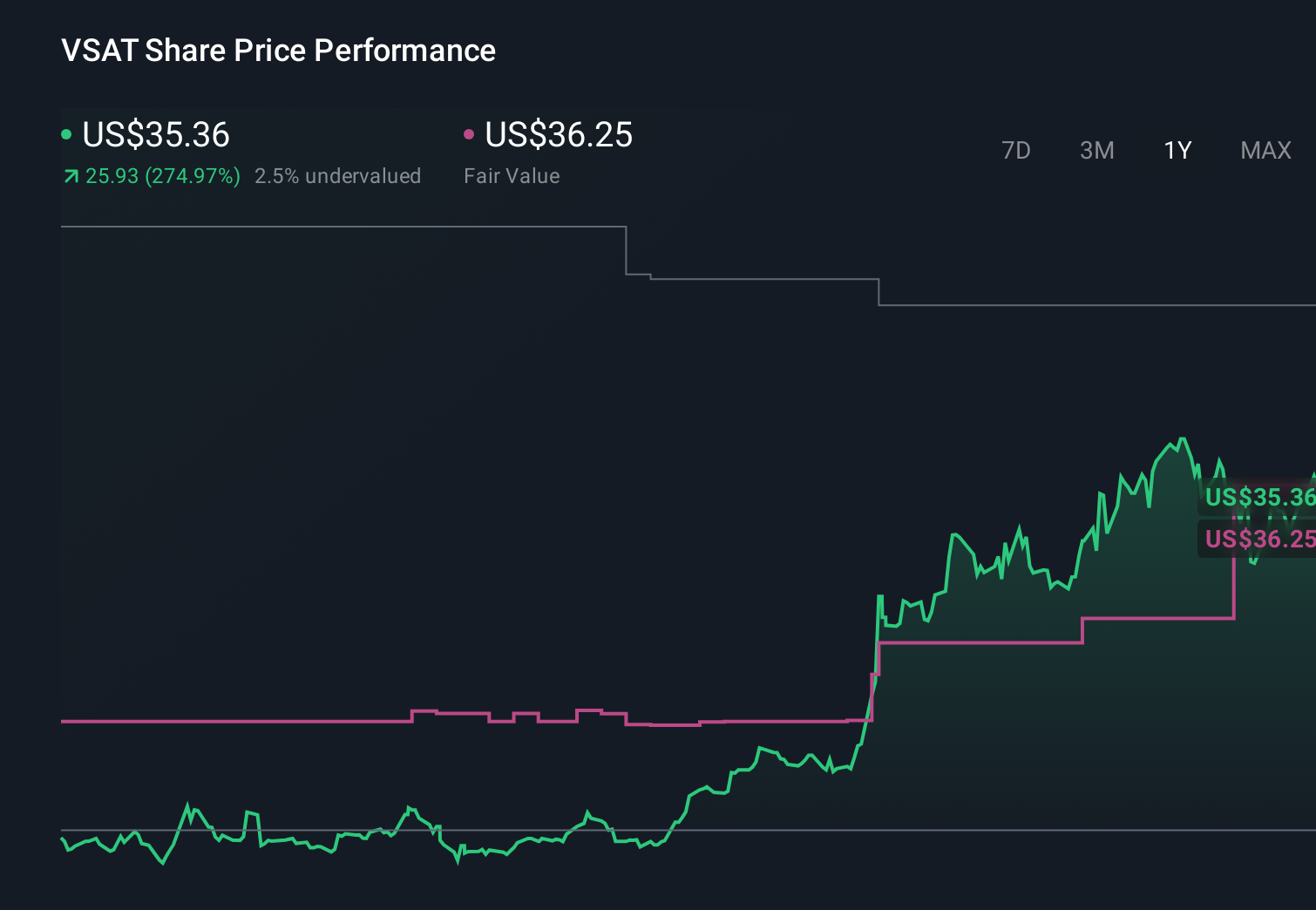

Viasat's narrative projects $5.3 billion revenue and $597.1 million earnings by 2029.

Uncover how Viasat's forecasts yield a $94.56 fair value, a 14% upside to its current price.

Exploring Other Perspectives

The most pessimistic analysts already assumed only about 3.3 percent annual revenue growth and continued losses, and they stress that tougher spectrum and orbital rules could blunt the impact of contracts like Protected Tactical SATCOM, so it is worth comparing that view with the possibility that regulatory headwinds on future GEO launches become even more important after this news.

Explore 8 other fair value estimates on Viasat - why the stock might be worth 41% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Viasat research is our analysis highlighting 3 important warning signs that could impact your investment decision.

- Our free Viasat research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Viasat's overall financial health at a glance.

No Opportunity In Viasat?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.