Is Warrior Met Coal's New Russell Growth Index Exposure Altering The Investment Case For HCC?

Warrior Met Coal, Inc. HCC | 0.00 |

- In late June 2026, Warrior Met Coal, Inc. (NYSE:HCC) was added to several Russell growth-oriented benchmarks, including the Russell 3000 Growth, 3000E Growth, 2500 Growth, 2000 Growth, and Russell Small Cap Comp Growth indexes, while being removed from the Russell 2000 Dynamic Index.

- This reshuffling into multiple growth and small-cap benchmarks could increase the company’s visibility with index-tracking funds and growth-focused institutional investors, potentially affecting trading volumes and investor perception of its growth profile.

- With Warrior Met Coal now included in several Russell growth indexes, we’ll examine how this new index exposure interacts with its existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Warrior Met Coal Investment Narrative Recap

To own Warrior Met Coal, you have to be comfortable with a pure-play metallurgical coal business whose fortunes are closely tied to global steel demand, Blue Creek’s ramp-up, and export markets. The new Russell growth index inclusions mainly affect who might trade the stock rather than those operational drivers, so they do not materially change the key near term catalyst of executing Blue Creek efficiently or the biggest risk around weaker steelmaking coal pricing and export demand.

Among recent announcements, the Blue Creek mine completion in January 2026 stands out as most relevant. It represents over US$1 billion of investment and a roughly 75% increase in nameplate capacity, directly linking Warrior’s future to how effectively it can place additional premium tons into export markets. That operational step change, more than index reshuffling, is likely to shape how investors weigh upside from higher volumes against the risks of an already challenged seaborne met coal market.

Yet beneath the index headlines, investors should be aware that Warrior’s growing dependence on export markets could...

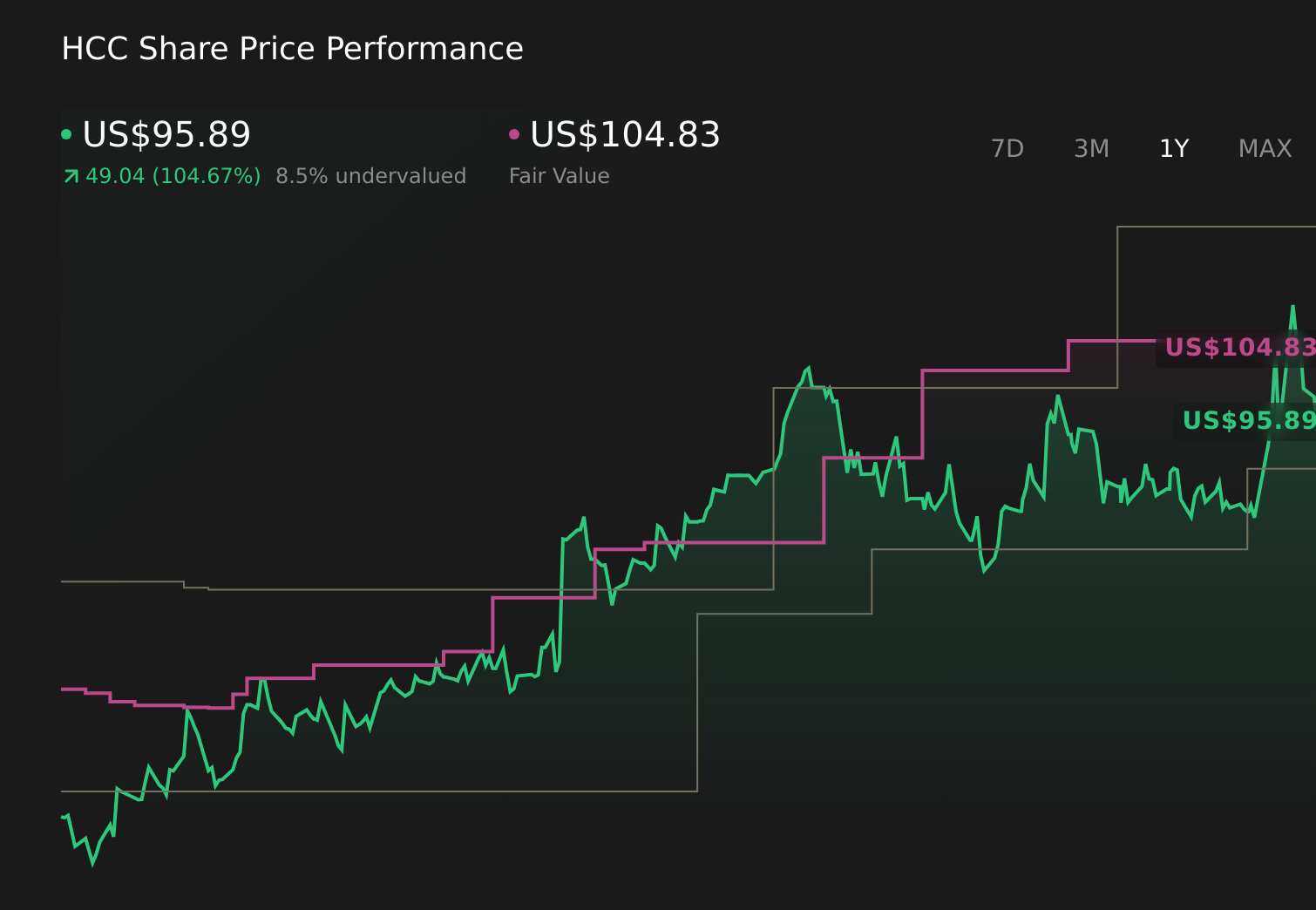

Warrior Met Coal's narrative projects $2.5 billion revenue and $543.8 million earnings by 2029. This requires 19.5% yearly revenue growth and about a $406 million earnings increase from $137.5 million.

Uncover how Warrior Met Coal's forecasts yield a $104.83 fair value, a 30% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling Warrior’s revenue at about US$2.7 billion and earnings near US$820.8 million by 2029, which is far more bullish than consensus. When you set that against the decarbonization and demand risks, and now layer in fresh Russell growth index inclusion, it underlines how differently you and other shareholders might interpret Warrior’s path from here.

Explore 4 other fair value estimates on Warrior Met Coal - why the stock might be worth just $104.83!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Warrior Met Coal research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Warrior Met Coal research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Warrior Met Coal's overall financial health at a glance.

Seeking Other Investments?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.