Is Waters (WAT) Price Attractive After Recent Life Sciences Coverage And Mixed Valuation Signals

Waters Corporation WAT | 0.00 |

- If you are looking at Waters and wondering whether the current share price reflects its underlying worth, the key question is how that price lines up with the company’s fundamentals.

- The stock last closed at US$371.15, with returns of 4.5% over the past month, 6.1% over the past year, and 41.0% over three years. Year to date the share price is down 2.8%, and over the past week it is marginally down 0.2%.

- Recent coverage around Waters has focused on its role in life sciences and analytical instruments. This continues to frame how investors think about its long term positioning and helps explain why the share price has moved in spurts rather than in a straight line, as sentiment reacts to how the company is perceived within its sector.

- On Simply Wall St’s 6 point valuation checklist, Waters currently scores 2 out of 6. The next step is to look at what different valuation methods say about that score and how a broader view of the company’s story can give an even richer sense of value.

Waters scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

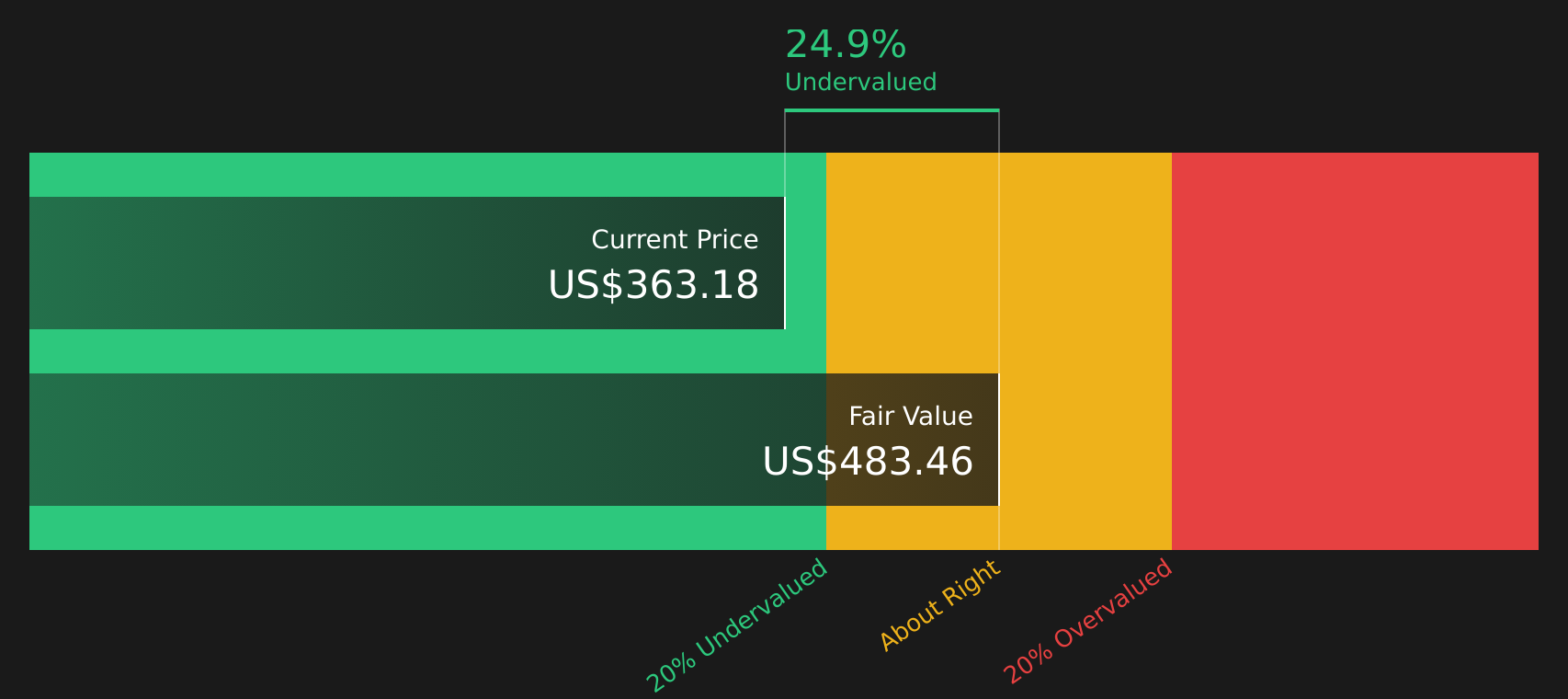

Approach 1: Waters Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a stock could be worth by projecting future cash flows and then discounting them back to today’s value using a required rate of return.

For Waters, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections in $. The latest twelve month free cash flow is about $226.1 million. Analyst estimates are available for the next few years, and Simply Wall St extrapolates beyond that, with projected free cash flow reaching about $3.2 billion in 2035, adjusted back into today’s money using discount factors such as $825.5 million in 2026 and $1,483.5 million in 2030.

When all projected and discounted cash flows are added together, the model arrives at an estimated intrinsic value of about $483.33 per share. Compared with the recent share price of $371.15, the DCF output suggests Waters trades at a 23.2% discount to this estimate, which in this model indicates the stock may be undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Waters is undervalued by 23.2%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

Approach 2: Waters Price vs Earnings

For a profitable company, the P/E ratio is a useful way to see how much you are paying for each dollar of earnings, which makes it a common anchor for thinking about value. What counts as a “normal” P/E depends on what the market expects for future growth and how risky those earnings are perceived to be, with higher growth or lower risk often associated with higher P/E levels.

Waters currently trades on a P/E of 81.05x. That is above both the Life Sciences industry average P/E of 34.00x and the peer average of 26.19x. To add more context, Simply Wall St calculates a proprietary “Fair Ratio” for each stock. For Waters, this Fair Ratio is 30.36x, which is the P/E level that aligns with factors such as earnings growth, industry, profit margin, market cap and company specific risks.

Because the Fair Ratio folds in these fundamentals, it can be more informative than a simple comparison with peers or the broader industry. In this case, Waters’ current P/E of 81.05x sits meaningfully above the Fair Ratio of 30.36x, which points to the stock looking expensive on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Waters Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives bring that to life by letting you attach a clear story about Waters to the numbers you are seeing, including your view on fair value and on future revenue, earnings and margins.

On Simply Wall St’s Community page, Narratives link a company story to a financial forecast and then to a fair value. You can compare that fair value with the current share price to help decide whether the stock looks attractive or stretched against your own assumptions.

Narratives are updated automatically when new information appears, such as news or earnings, so the numbers and the storyline stay aligned without you needing to rebuild a model from scratch each time something changes.

For Waters, one investor narrative on the bullish side might lean toward a fair value around US$460.00 based on optimistic revenue growth, higher margins and a P/E of 49.2x by 2029. A more cautious narrative might anchor around US$330.00 with different assumptions for growth, margins and a future P/E of 35.5x. Seeing these side by side helps you quickly see which story feels closer to your own view.

For Waters however we will make it really easy for you with previews of two leading Waters Narratives:

Fair value in this bullish narrative: US$460.00

Implied discount vs last close (US$371.15): about 19.4% below this fair value estimate

Assumed revenue growth: 30.49%

- Assumes rapid adoption of new omics platforms and workflow solutions, with recurring revenue and higher margin products lifting long term profitability.

- Builds in benefits from the BD Biosciences and Diagnostic Solutions acquisition, including broader customer reach and modeled cost synergies.

- Requires confidence that by 2029 Waters can reach US$8.4b of revenue and US$1.4b of earnings while supporting a P/E of 49.2x on those earnings.

Fair value in this cautious narrative: US$330.00

Implied premium vs last close (US$371.15): about 12.5% above this fair value estimate

Assumed revenue growth: 34.13%

- Highlights reliance on mature product lines and the risk that customer budget pressure and alternative technologies weaken pricing power over time.

- Flags integration and execution risks around the BD acquisition, along with exposure to more volatile emerging markets and sensitive end markets such as academic and government research.

- Assumes Waters reaches about US$7.6b of revenue and US$1.4b of earnings by 2029, on a lower future P/E of 35.5x, which keeps the modeled upside in check relative to the current share price.

If you want to see how your own expectations stack up against these bullish and bearish stories, you can review the full set of narratives, adjust the assumptions and see how that changes the implied fair value for Waters, using See what the community is saying about Waters.

Do you think there's more to the story for Waters? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.