Is Wells Fargo’s Upgrade Reframing EPD’s LPG Export Network as a Core Competitive Edge?

Enterprise Products Partners L.P. EPD | 0.00 |

- In May 2026, Wells Fargo upgraded Enterprise Products Partners, highlighting the partnership’s midstream infrastructure and its ability to benefit from changing global LPG trade patterns.

- The upgrade emphasizes how Enterprise’s export terminals and pipelines could play a central role as Europe and other regions adjust long-term energy sourcing.

- Next, we’ll explore how Wells Fargo’s confidence in Enterprise’s LPG export footprint may influence the partnership’s existing investment narrative.

Outshine the giants: these 12 early-stage AI stocks could fund your retirement.

Enterprise Products Partners Investment Narrative Recap

To own Enterprise Products Partners, you need to believe in the long term value of its integrated midstream network and its role in global LPG trade. Wells Fargo’s upgrade reinforces that thesis, but does not materially change the near term focus on bringing new export capacity online or the key risk around external factors such as tariffs and producer activity in the Permian Basin.

The most relevant recent announcement here is Enterprise’s Q1 2026 results, which showed higher pipeline and marine terminal volumes alongside steady earnings and continued unit buybacks. This operational backdrop matters for investors weighing Wells Fargo’s confidence in the LPG export footprint against ongoing risks tied to tariffs, debt levels and potential production shifts that could affect throughput and export activity.

Yet behind the appeal of growing LPG exports, investors should be aware of how changing tariff regimes could...

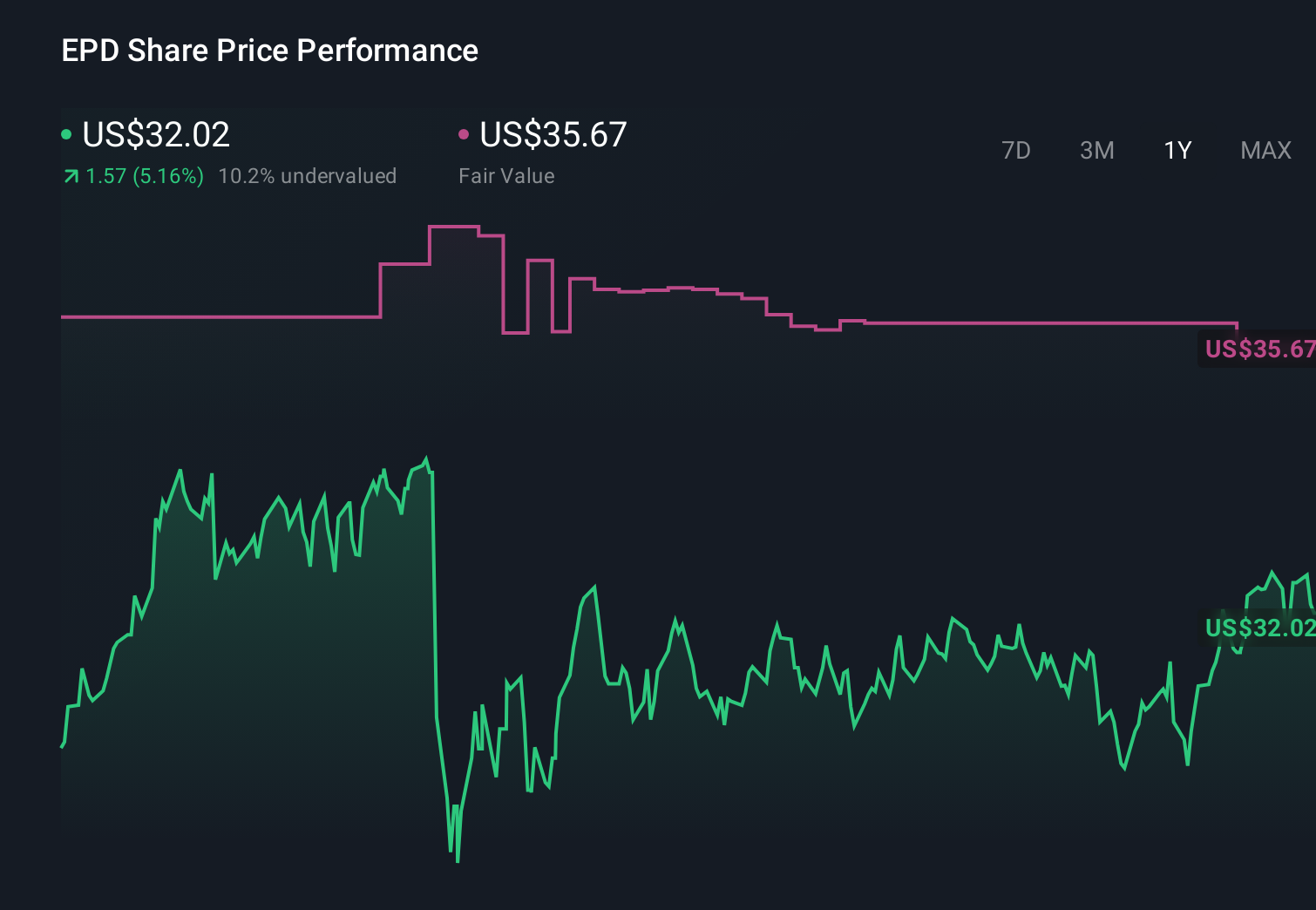

Enterprise Products Partners' narrative projects $60.5 billion revenue and $7.4 billion earnings by 2029. This requires 5.5% yearly revenue growth and a $1.6 billion earnings increase from $5.8 billion today.

Uncover how Enterprise Products Partners' forecasts yield a $40.85 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community span roughly US$34 to US$92 per unit, showing very different expectations for Enterprise’s future. Against this spread of views, the tariff and export related risks around LPG highlight why it can be useful to compare several independent perspectives before forming your own.

Explore 6 other fair value estimates on Enterprise Products Partners - why the stock might be worth 7% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Enterprise Products Partners research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Enterprise Products Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Enterprise Products Partners' overall financial health at a glance.

Contemplating Other Strategies?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.