Is Williams (WMB) Turning Natural Gas Infrastructure Into a Shelter From Commodity Volatility?

Williams Companies, Inc. WMB | 0.00 |

- Recently, Williams Companies was cited alongside Kinder Morgan and MPLX as a midstream operator that has held up well despite oil-price swings, largely due to its fee-based, long-term contracts and extensive U.S. natural gas pipeline network.

- The coverage emphasized that Williams’ focus on natural gas infrastructure tied to growing “cleaner” energy demand may appeal to investors seeking lower commodity exposure and more predictable cash flows.

- Next, we’ll consider how Williams’ fee-based resilience to oil volatility informs its existing investment narrative around gas growth and contracted projects.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Williams Companies Investment Narrative Recap

To own Williams, you need to be comfortable with a story built around long-term, fee-based natural gas infrastructure and relatively limited direct oil-price exposure. The recent commentary grouping Williams with other resilient midstream names reinforces that narrative but does not materially change the near term picture: contracted gas growth projects remain the key catalyst, while permitting and policy risks around new pipelines still look like the most important near term overhang.

Among recent announcements, the progress on the Northeast Supply Enhancement project, including the April 2026 groundbreaking in Brooklyn, ties directly into that gas growth narrative. NESE’s planned capacity addition on Transco highlights how Williams is leaning into demand for gas-fired power and reliability, even as regulatory and environmental scrutiny around such projects continues to shape timing, costs and the risk profile for its future cash flows.

Yet while cash flows look steadier today, investors should still understand how faster decarbonization policies could affect...

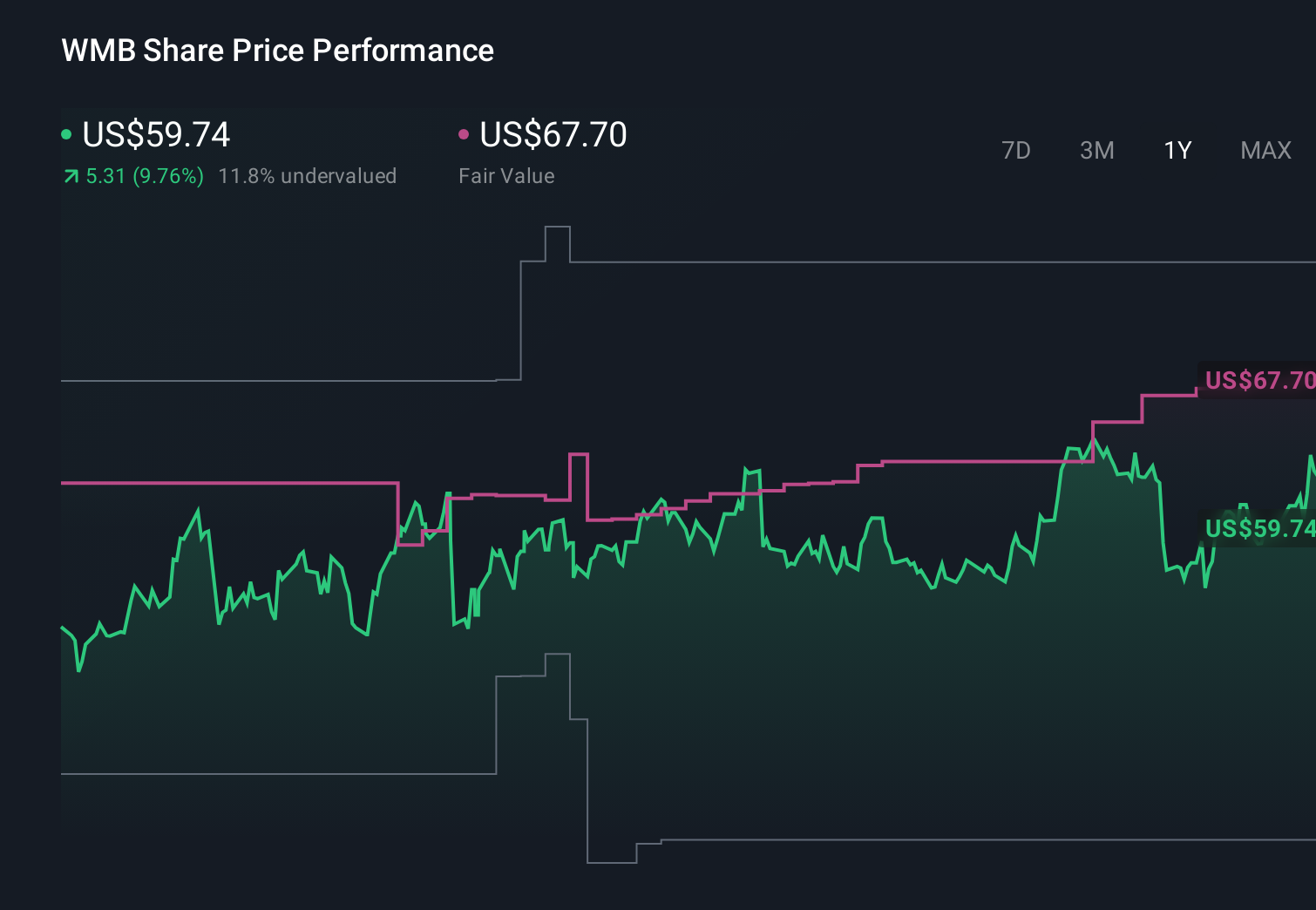

Williams Companies' narrative projects $16.3 billion revenue and $3.9 billion earnings by 2029.

Uncover how Williams Companies' forecasts yield a $80.07 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$17.9 billion and earnings US$4.8 billion by 2029, so if you are weighing those upbeat expectations against today’s cleaner energy demand story and rising ESG risks, this new fee based resilience narrative might either strengthen their case or expose how much could still change.

Explore 5 other fair value estimates on Williams Companies - why the stock might be worth 14% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Williams Companies research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Williams Companies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Williams Companies' overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.