Is WTW’s Strong Q1 and AI Push Quietly Rewriting Willis Towers Watson’s Competitive Playbook?

Willis Towers Watson WTW | 0.00 |

- Willis Towers Watson recently reported past first-quarter 2026 results, with revenue rising to US$2,412 million and net income to US$297 million, alongside higher basic and diluted earnings per share from continuing operations year over year.

- At the same time, the company deepened its AI focus and leadership bench through the Newfront integration and senior appointments, signalling an effort to align technology, talent and growth plans across North America.

- We’ll now examine how WTW’s stronger Q1 earnings and expanded AI leadership reshape its existing investment narrative and future expectations.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Willis Towers Watson Investment Narrative Recap

To own Willis Towers Watson, you need to believe it can turn its advisory, broking and benefits platforms into resilient, compounding earnings, helped by disciplined cost control and AI driven productivity. The latest Q1 results, with higher revenue and earnings per share, support that thesis in the near term, but the sharp share price pullback around slower organic growth shows the key short term catalyst remains evidence of sustained mid single digit growth, while competitive pricing and integration risks are still front of mind.

The appointment of Spike Lipkin as Chief AI Officer and Gordon Wintrob as Head of AI Acceleration looks particularly relevant here, because it ties directly to WTW’s effort to use AI and automation to improve efficiency and scalability across Health, Wealth & Career and Risk & Broking. For investors watching whether technology can offset pricing pressure and help protect margins, this AI leadership build out sits right at the intersection of the current growth catalyst and the risk of service commoditization.

Yet while AI leadership might support efficiency, investors should also be aware that...

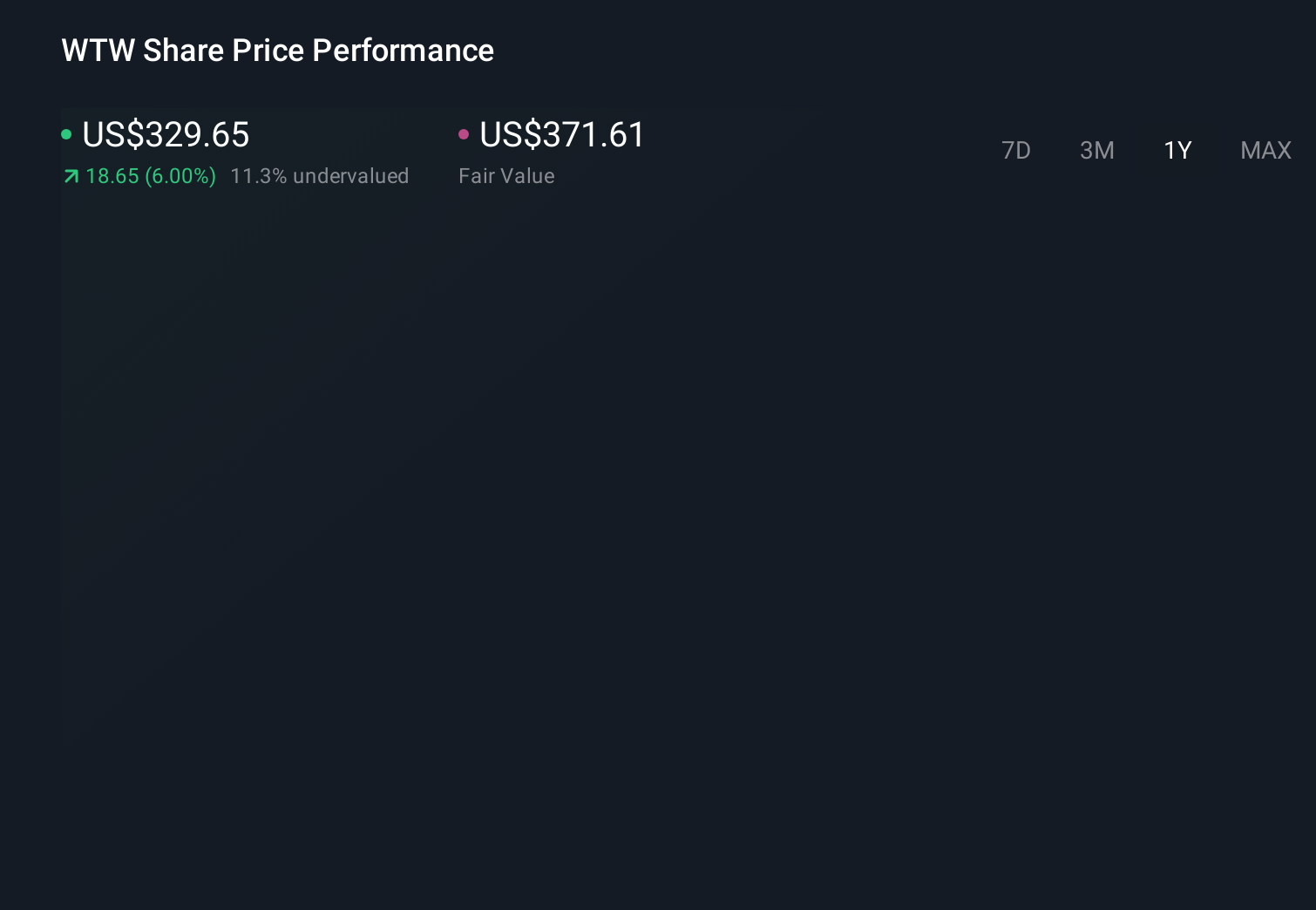

Willis Towers Watson's narrative projects $11.9 billion revenue and $1.8 billion earnings by 2029. This requires 6.9% yearly revenue growth and about a $0.2 billion earnings increase from $1.6 billion today.

Uncover how Willis Towers Watson's forecasts yield a $354.74 fair value, a 38% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span roughly US$224 to US$355 per share, showing how widely individual views can differ. Against that backdrop, the recent focus on AI driven efficiency and integration progress raises important questions about how WTW can defend pricing power and margins that readers may want to explore further.

Explore 2 other fair value estimates on Willis Towers Watson - why the stock might be worth as much as 38% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Willis Towers Watson research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Willis Towers Watson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Willis Towers Watson's overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.