Is XPO's (XPO) Steady Revenue Hiding Deeper Profitability Challenges?

XPO, Inc. XPO | 199.09 | +2.33% |

- XPO reported second quarter and six-month 2025 earnings, showing flat year-over-year sales at US$2.08 billion for the quarter but a decrease in net income to US$106 million from US$150 million, following the completion of a US$10 million share buyback.

- Despite continued investment in its own shares, XPO's declining net income and earnings per share likely signaled challenges with profitability, highlighting the impact of operational headwinds amid stable revenue.

- With earnings falling despite steady revenues and the recently completed share repurchase, we'll explore how these profit pressures affect XPO's outlook.

Find companies with promising cash flow potential yet trading below their fair value.

XPO Investment Narrative Recap

For investors to remain constructive on XPO, belief in the company's ability to drive long-term margin expansion through operational efficiency and technological investments is crucial, especially given its concentrated exposure to cyclical US LTL freight markets. The latest earnings report, which revealed flat revenue but declining net income and EPS despite share buybacks, brought profit pressures to the forefront; these results highlight short-term margin risks rather than materially altering the main long-term catalyst of technology-led efficiency gains.

The recent Q2 2025 earnings announcement stands out as most relevant, as it underscores the challenge of sustaining profitability even when revenues remain steady. This earnings softness, following a share repurchase, keeps the spotlight on execution risk tied to labor costs, freight demand, and the company's ability to translate operational enhancements into bottom-line improvement as volumes fluctuate.

Yet, the critical factor investors should be alert to is the potential for prolonged end-market weakness that could...

XPO's narrative projects $9.2 billion revenue and $657.8 million earnings by 2028. This requires 4.6% yearly revenue growth and a $312.8 million earnings increase from $345.0 million currently.

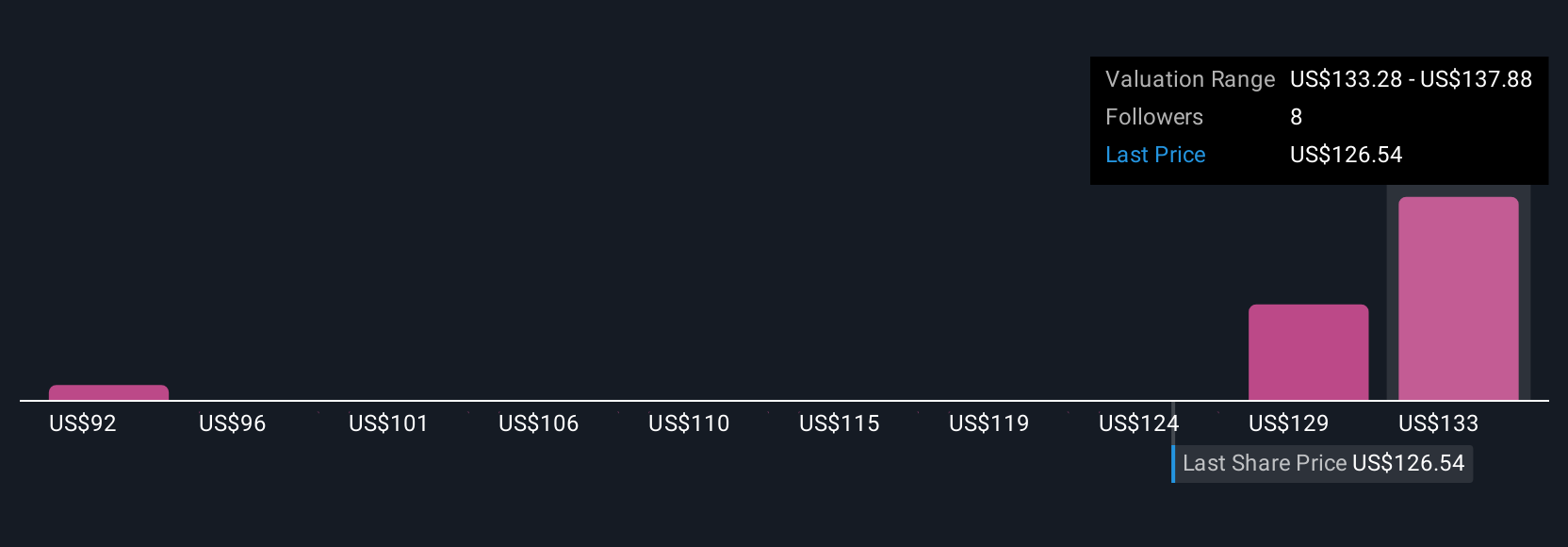

Uncover how XPO's forecasts yield a $137.88 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members provided three fair value estimates for XPO, ranging from US$91.89 to US$137.88 per share. As these opinions vary widely, it's worth noting that compressed earnings and margin volatility are drawing heightened attention given the recent financial results.

Explore 3 other fair value estimates on XPO - why the stock might be worth as much as 9% more than the current price!

Build Your Own XPO Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your XPO research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free XPO research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate XPO's overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 27 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.