Jefferies Financial Group (JEF) Stock Valuation After Optimistic Q2 Outlook And Insider Buying

Jefferies Financial Group Inc. JEF | 0.00 |

Jefferies Financial Group (JEF) has drawn attention after analyst commentary pointed to favorable conditions for its investment banking and capital markets segments ahead of fiscal Q2 results, alongside substantial recent insider share purchases.

The recent analyst optimism and insider buying sit alongside strong price momentum, with a 69.6% 3 month share price return and a 21.6% 1 year total shareholder return, signaling that sentiment has strengthened despite a small year to date pullback.

If Jefferies has caught your eye, it can also be useful to see what else is moving. You might start with a focused list of 20 top founder-led companies

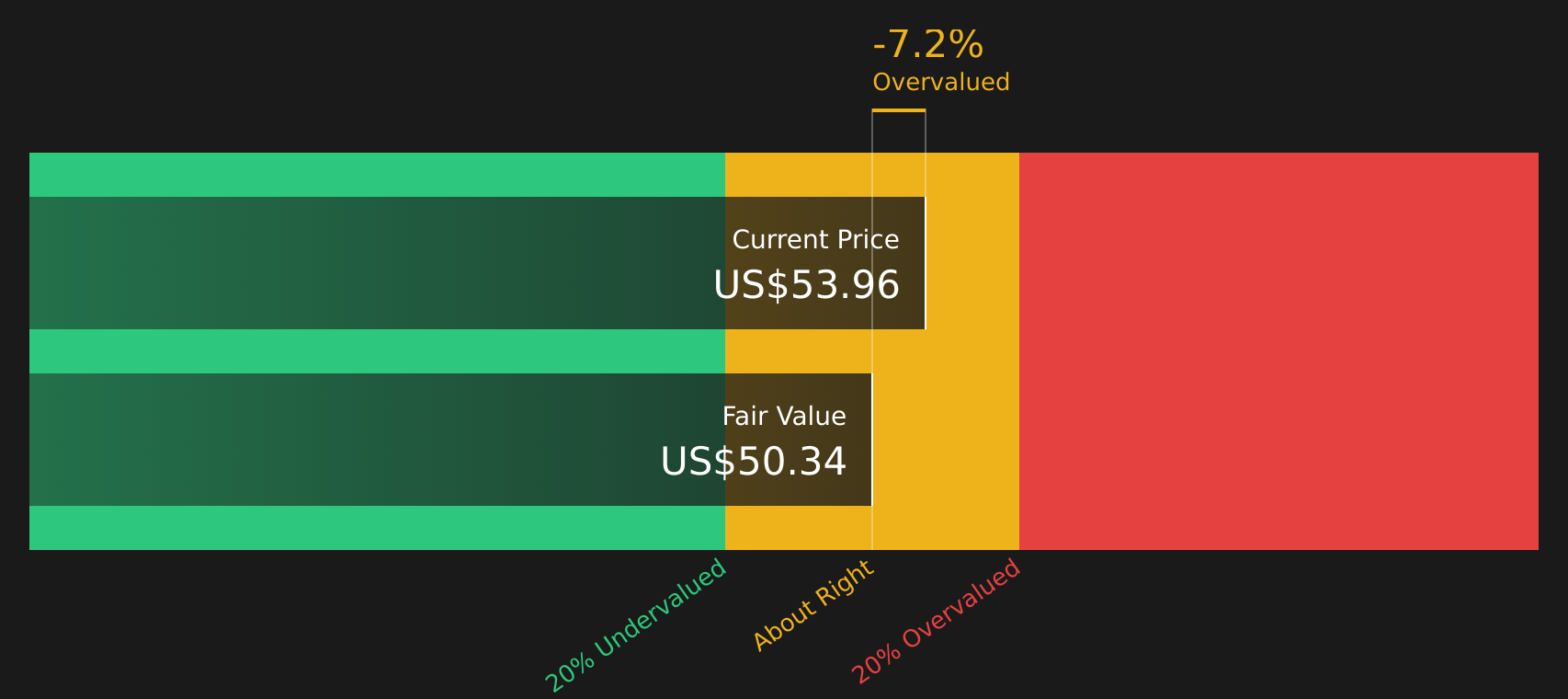

With Jefferies trading close to recent analyst targets and some models flagging a slight premium to intrinsic value, along with heavy insider buying and upbeat segment commentary, the question becomes: is there still a buying opportunity here, or is the market already pricing in future growth?

Price-to-Earnings of 19x: Is it justified?

Jefferies is trading on a P/E of 19x, which screens as expensive against its own fair P/E estimate and closer peer group, even though the share price is only slightly above analyst targets.

The P/E multiple compares the current share price with the company’s earnings per share. A higher figure usually reflects stronger growth expectations or a quality premium. For Jefferies, earnings are forecast to grow 11.7% per year and revenue 3.3% per year, both slower than the broader US market, which raises the question of whether investors are paying a premium for this profile.

Jefferies trades on a P/E of 19x versus a fair P/E estimate of 16.7x and a peer average of 15.5x. This implies the market is assigning a richer multiple than both the regression-based fair ratio and closer peers, even if it still sits well below the wider US Capital Markets industry average of 39.5x.

Result: Price-to-Earnings of 19x (OVERVALUED)

However, Jefferies still faces risks if investment banking activity cools or if current valuation multiples compress, which could challenge the recent share price momentum.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Cash Flows Paint A Different Picture

The SWS DCF model points in the same direction as the P/E work, with Jefferies trading at $61.66 compared with an estimated future cash flow value of $47.07. That gap suggests less room for error if earnings or returns on equity come in below forecasts.

Before you lean too much on any one approach, it is worth pressure testing the assumptions behind the cash flow model Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Jefferies Financial Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Does the mix of optimism and concern in this setup match your own view, or does it feel stretched? Act quickly to test the assumptions that matter to you, and weigh the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Jefferies feels fully priced to you, do not stop here. Broaden your watchlist with focused stock ideas that fit different goals and risk levels.

- Target income first and scan for companies that may support future payouts through 8 dividend fortresses.

- Hunt for potential mispricing by reviewing companies flagged in the screener containing 20 high quality undiscovered gems.

- Prioritise resilience by checking stocks highlighted in the 70 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.