Keurig Dr Pepper (KDP) Reaffirms Guidance And Prepares Split, Is The Stock Fully Valued?

Keurig Dr Pepper KDP | 0.00 |

Keurig Dr Pepper (KDP) is in the spotlight after announcing key leadership changes and reaffirming its 2026 earnings guidance, while also preparing to split into two independent companies: Beverage Co. and Global Coffee Co.

Recent leadership changes and preparation for the coffee and beverage split have come alongside a 30-day share price return of 9.07% and a 90-day share price return of 29.57%, while the 1-year total shareholder return sits at 1.87%. This suggests that shorter term momentum has been stronger than longer term results.

If you are considering how Keurig Dr Pepper fits alongside other ideas, this can be a good moment to broaden your search and uncover 20 top founder-led companies

With Keurig Dr Pepper up 20.1% year to date and trading only slightly below analyst targets, the key question now is whether the planned split and leadership changes leave hidden value on the table, or if the stock already reflects future growth.

Most Popular Narrative: 70% Undervalued

The most widely followed narrative for Keurig Dr Pepper places fair value at about $33.53 per share, slightly above the last close of $33.30. It hinges on how earnings and revenue forecasts play out under a long term growth plan.

The analysts have a consensus price target of $33.53 for Keurig Dr Pepper based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $42.0, and the most bearish reporting a price target of just $28.0.

Want to see what justifies a fair value well above today’s price? The narrative leans on faster revenue growth, firmer margins and a reset earnings multiple. The precise mix of those assumptions is where the story gets interesting.

Result: Fair Value of $33.53 (UNDERVALUED)

However, the Keurig Dr Pepper story still faces pressure from a softer U.S. Coffee segment and rising input costs, which could challenge margins if conditions persist.

Another View: How Keurig Dr Pepper Looks On Earnings

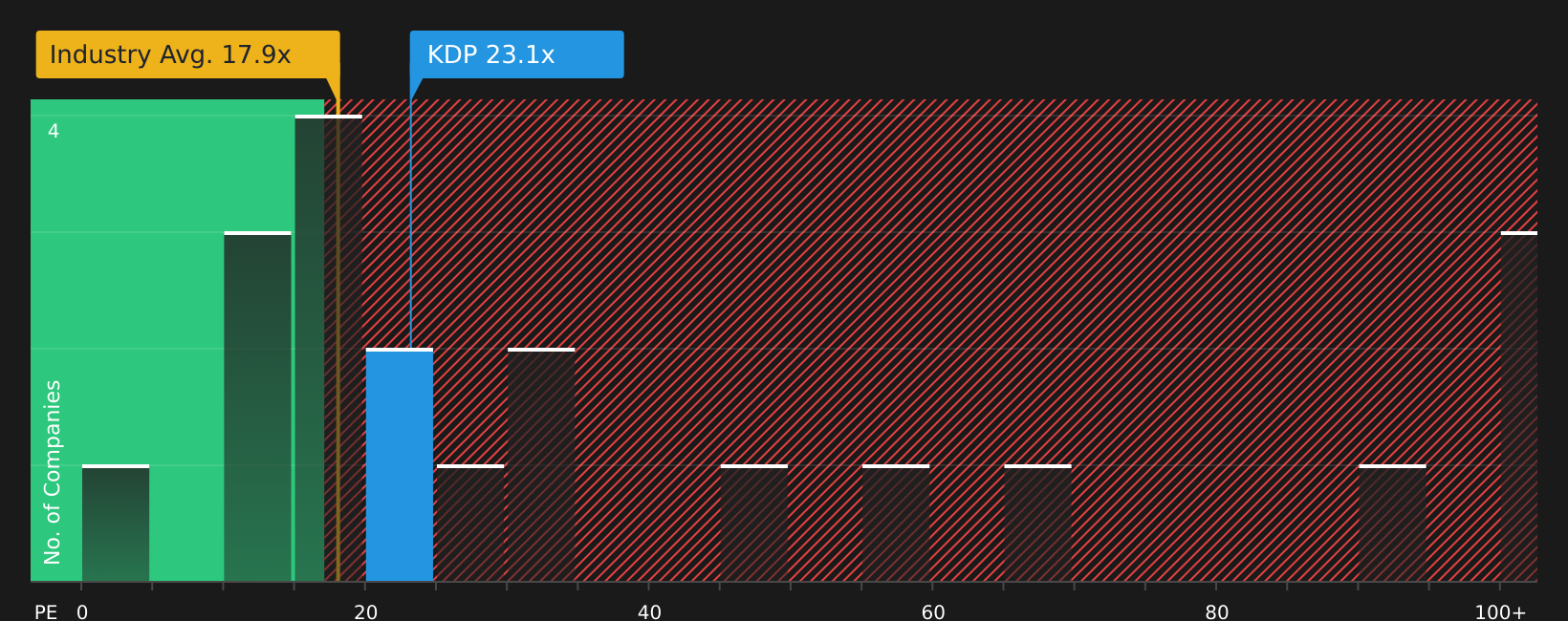

The earlier fair value work paints Keurig Dr Pepper as 50.7% below an estimated intrinsic value, yet the current P/E ratio of 24.7x tells a tougher story. It sits well above the Global Beverage industry at 17x and slightly above an estimated fair ratio of 23.2x. This points to less clear upside and more sensitivity if expectations cool.

That kind of premium can reflect confidence in the earnings path, but it also leaves less room for error. The real question is whether you think the market will move closer to the industry level or toward the fair ratio over time, and how comfortable you are with that trade off, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment on Keurig Dr Pepper clearly mixed, this is a good moment to act quickly, review the full picture yourself, and weigh both the upside and the risks highlighted in 2 key rewards and 1 important warning sign.

Looking for more ideas beyond Keurig Dr Pepper?

If you are weighing what to do next after reviewing Keurig Dr Pepper, this is a good time to scan other opportunities and avoid leaving potential ideas on the table.

- Target income first by reviewing dependable payers and their resilience using the 7 dividend fortresses.

- Hunt for mispriced quality by running a fresh search through the 44 high quality undervalued stocks.

- Round out your watchlist with off-the-radar companies that show solid fundamentals using the screener containing 18 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.