Kinder Morgan (KMI) Valuation Check As US$20b Project Pipeline And Dividend Growth Plans Draw Investor Focus

Kinder Morgan Inc Class P KMI | 31.70 31.70 | +0.16% 0.00% Pre |

Kinder Morgan (KMI) is back in focus after management outlined about US$10b of gas pipeline projects through mid 2030 and an additional US$10b in potential expansions, alongside plans for a ninth consecutive annual dividend increase.

The stock’s recent moves suggest momentum has been building, with a 14.9% 30 day share price return, a 19.8% 90 day share price return and a 1 year total shareholder return of 25.3% alongside these fresh growth and dividend plans.

If Kinder Morgan’s energy infrastructure build out has your attention, you might also want to see which other power related companies are standing out in our 24 power grid technology and infrastructure stocks.

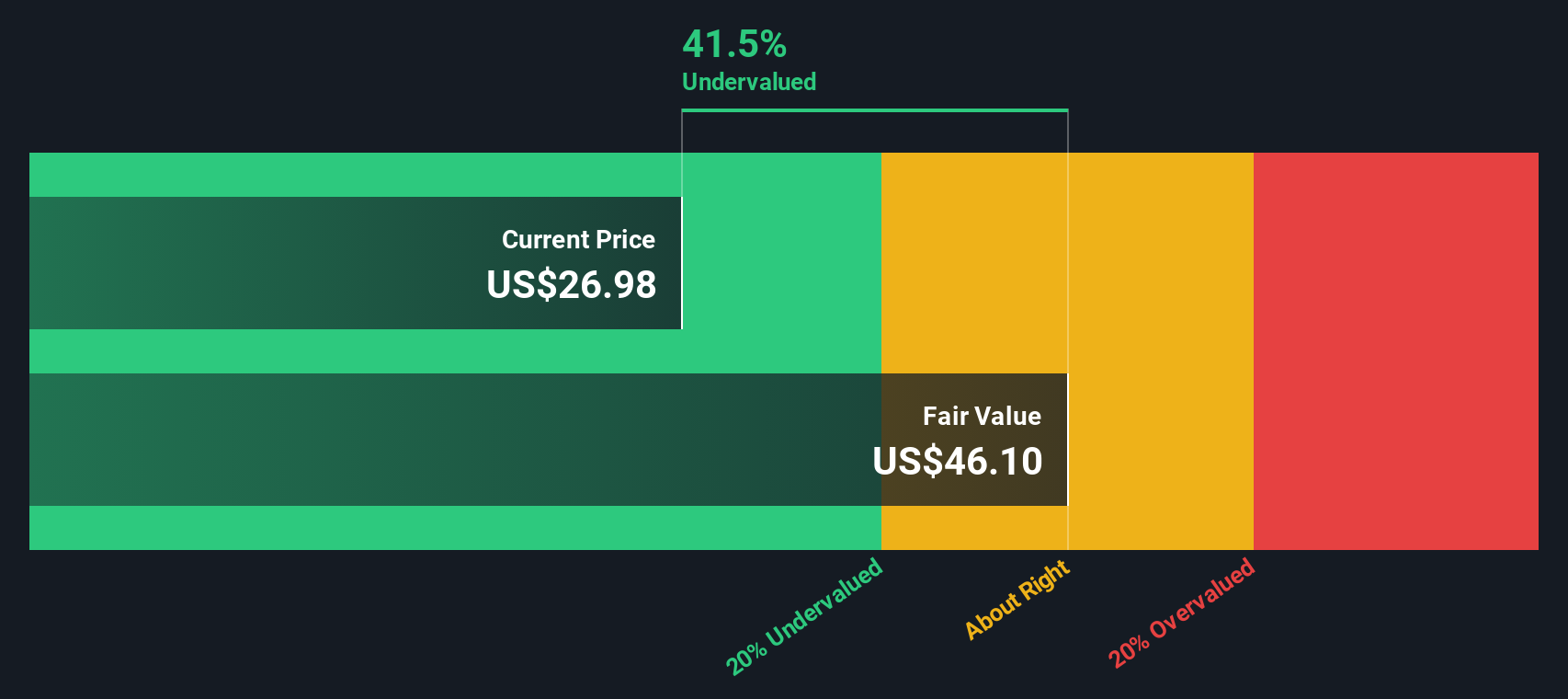

With Kinder Morgan trading near its analyst price target yet flagged with a sizeable intrinsic discount, the key question is simple: is this pipeline giant still trading below its underlying value, or has the market already priced in years of future growth?

Most Popular Narrative: 1% Overvalued

The most followed Kinder Morgan narrative puts fair value at about $31.76 per share, just under the last close of $32.13, and builds its case around earnings quality, pipeline exposure and updated analyst assumptions.

Recent Street research has focused on Kinder Morgan's valuation framework, with several firms adjusting price targets and ratings in light of updated P/E and margin assumptions. Here is how bullish and cautious views are shaping up around the same set of data points.

Want to see what sits underneath that tight fair value range? The narrative leans on measured growth, firm margin assumptions and a richer future earnings multiple. Curious how those inputs fit together to back a price just under today’s level?

Result: Fair Value of $31.76 (OVERVALUED)

However, this hinges on assumptions that could be tested, including Kinder Morgan’s sizeable US$32.3b net debt load and the risk of overbuild or lower-rate recontracting in key regions.

Another View: DCF Points To A Deeper Discount

While the popular narrative has Kinder Morgan at roughly 1% overvalued around $31.76 per share, our DCF model tells a different story, putting fair value closer to $49.81. That 35.5% gap suggests the real debate is whether cash flows or multiples are giving the clearer signal.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Kinder Morgan for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 56 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With one narrative hinting at a mild premium and another suggesting a bigger discount, it is worth moving quickly to test the numbers yourself, including 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Kinder Morgan has sharpened your focus, do not stop here, the screener can help you quickly spot other opportunities that might fit your style just as well.

- Target potential value opportunities by reviewing our 56 high quality undervalued stocks that pair quality fundamentals with pricing that may merit a closer look.

- Lock in potential income ideas by scanning through 13 dividend fortresses that could appeal if regular payouts are high on your priority list.

- Prioritise resilience by checking companies in the 81 resilient stocks with low risk scores that score well on stability and risk metrics before they move further onto the market’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.