KKR (KKR) Could Be 15% Overvalued On Allyntra Launch

KKR & Co KKR | 0.00 |

KKR (KKR) has drawn fresh attention after unveiling Allyntra, a new precision engineered solutions platform focused on medical technology and advanced surgical applications. The platform is built around existing portfolio company Precipart and supported by additional committed capital.

At a share price of $96.91, KKR has seen a modest 7 day share price return of 0.98% and a 30 day share price return of 0.70%. The year to date share price return is down 24.82%, while the 3 year total shareholder return of 63.08% points to stronger longer term performance even as recent momentum has softened.

If developments like Allyntra have you thinking about where capital could move next in markets tied to technology and infrastructure, it may be worth scanning opportunities in 18 top founder-led companies

After KKR’s share price slide this year and the fresh push into medtech through Allyntra, today’s valuation work comes down to a simple issue: does the current risk reward still lean in favour of buyers?

Most Popular Narrative: 14.8% Overvalued

The most followed valuation narrative for KKR compares a fair value of $84.45 to the last close of $96.91, suggesting the current price sits meaningfully above that estimate while investors weigh the company’s long term capital compounding story.

Desde un enfoque Buffett puro:

KKR empieza a parecer menos un gestor de private equity y más un “compounder de capital permanente”.

Lectura final:

Valor intrínseco: ~$105 a $120 por acción

Basado SOLO en negocio recurrente

Con opcionalidad no valorada

There is a clear tension here. One fair value anchors closer to current pricing, another points higher, and both lean heavily on recurring earnings, insurance float and long dated capital. Want to see which revenue trend and profitability profile sit at the core of that $84.45 figure, and how the discount rate shapes the outcome.

Result: Fair Value of $84.45 (OVERVALUED)

However, this KKR narrative could be challenged if private credit losses bite harder than expected or if fundraising slows, putting pressure on fee-based earnings.

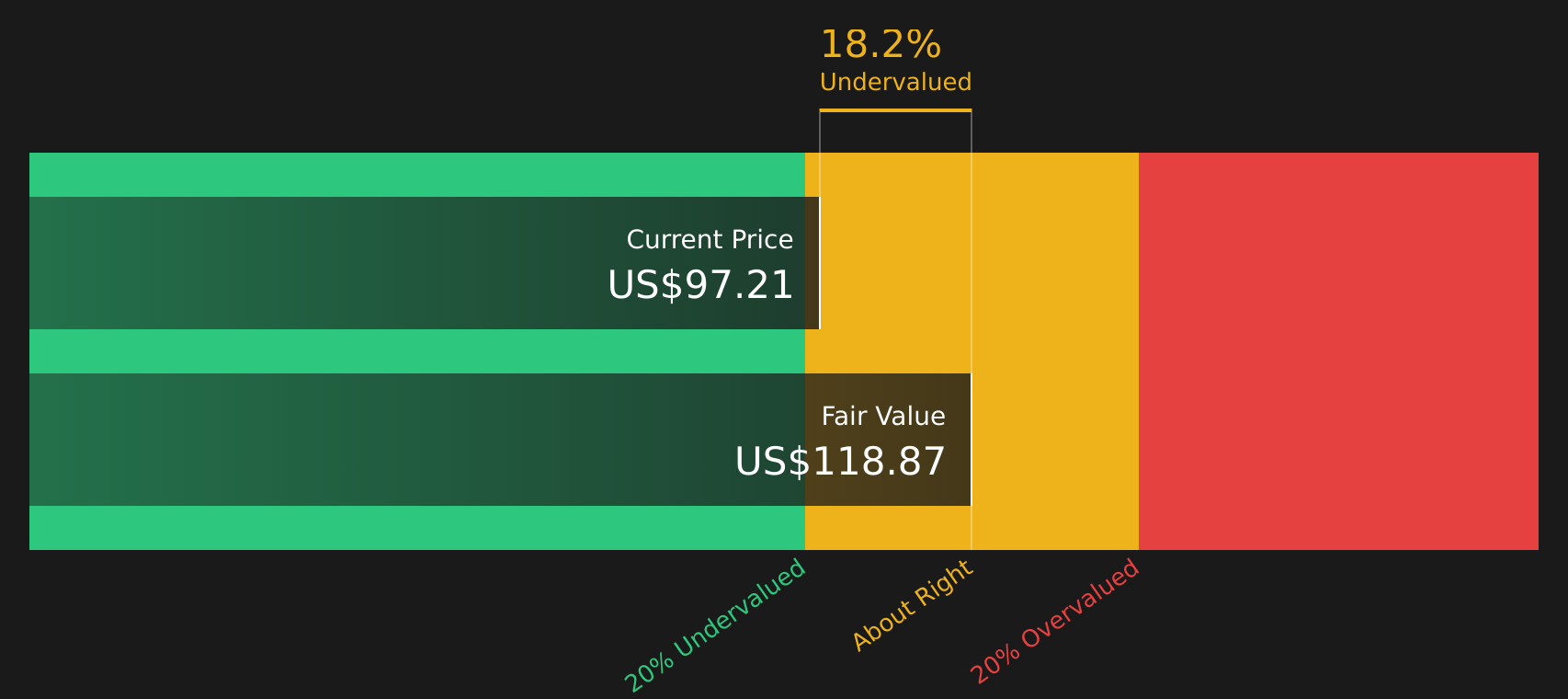

Another View: SWS DCF Model Points To Undervaluation

While the user generated memo frames KKR as roughly 14.8% overvalued at $96.91 versus a fair value of $84.45, the SWS DCF model points the other way, with an estimated future cash flow value of $118.63, or about 18.3% above the current price. Which set of assumptions feels more realistic to you?

For a closer look at how those future cash flows are treated and what sits behind that $118.63 figure, our DCF work is laid out in full in Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out KKR for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this combination of conviction and disagreement around KKR’s value leaves you undecided, take a moment to quickly review the full picture of potential upsides in 3 key rewards

Looking for more investment ideas beyond KKR?

If you want to stress test your view on KKR and see what else could deserve a spot on your watchlist, it is worth broadening the opportunity set with a few targeted screens.

- Spot potential mispricings early by scanning 46 high quality undervalued stocks where quality fundamentals and compressed valuations line up.

- Prioritise resilience by reviewing 80 resilient stocks with low risk scores that score well on stability and downside protection.

- Hunt for tomorrow’s standouts before the crowd pays attention by working through the screener containing 20 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.