Krystal Biotech (KRYS) Is Up 7.2% After Institutional Ownership Surges To Sector-Leading Levels

Krystal Biotech, Inc. KRYS | 0.00 |

- In recent months, Krystal Biotech has seen its institutional shareholding score reach the maximum of 10.00, with major investors such as ETHSX and BlackRock increasing their positions and lifting overall institutional ownership by 11.17% quarter-over-quarter.

- This sharp rise in institutional participation places Krystal Biotech at the top of its Biotechnology & Medical Research peer group for institutional backing, highlighting stronger professional investor interest despite limited disclosure of some valuation metrics.

- We’ll now examine how this surge in institutional ownership, alongside a P/E ratio of 44.93, influences Krystal Biotech’s investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Krystal Biotech Investment Narrative Recap

To own Krystal Biotech, you need to believe that VYJUVEK can support a durable rare disease franchise while the broader gene therapy pipeline matures. The spike in institutional ownership and a P/E of 44.93 do not directly change the near term focus on execution in new markets or the key risk around VYJUVEK concentration and treatment variability, but they do underline how closely professionals are watching these issues.

The recent series of VYJUVEK approvals in Europe, Japan, and most recently the UK is especially relevant here, because it underpins the growth story institutional investors are buying into while also amplifying reimbursement and pricing risks across multiple health systems. How effectively Krystal converts these new labels into consistent patient starts and renewals will go a long way toward validating, or challenging, the confidence implied by today’s valuation and ownership profile.

Yet, behind this optimism, there is a risk around unpredictable VYJUVEK treatment pauses and restarts that investors should be aware of, especially as...

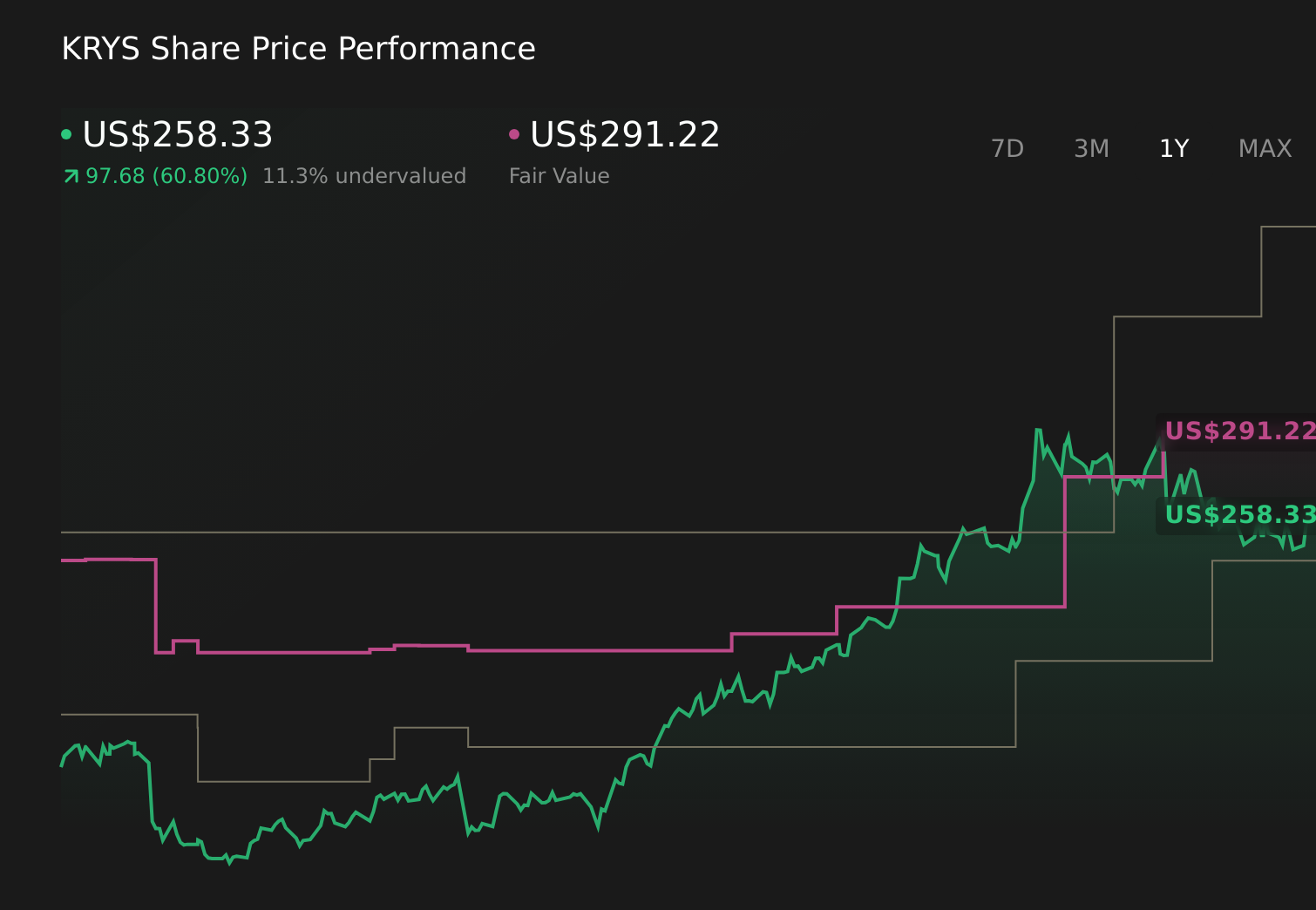

Krystal Biotech's narrative projects $1.0 billion revenue and $568.7 million earnings by 2029. This requires 34.5% yearly revenue growth and a $343.7 million earnings increase from $225.0 million today.

Uncover how Krystal Biotech's forecasts yield a $322.78 fair value, a 7% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts took a much more cautious view, assuming revenue of about US$797,200,000 and earnings of roughly US$310,000,000 by 2029, so this jump in institutional buying could eventually shift how you weigh that more pessimistic stance against your own expectations.

Explore 5 other fair value estimates on Krystal Biotech - why the stock might be worth 31% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Krystal Biotech research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Krystal Biotech research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Krystal Biotech's overall financial health at a glance.

Searching For A Fresh Perspective?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 38 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.