Krystal Biotech (KRYS) Rallies On Pipeline Optimism, Is The Stock Already Pricey?

Krystal Biotech, Inc. KRYS | 0.00 |

Krystal Biotech (KRYS) has drawn fresh attention after recent trading left the stock with a 1 day move of 3.5% and a past 3 months return of 46.7%. This has prompted closer scrutiny of fundamentals.

At a latest share price of $359.93, Krystal Biotech shows strong momentum, with a 30 day share price return of 18.9% and a 1 year total shareholder return of 152.4%, pointing to growing investor interest.

If this kind of momentum has your attention, it can be useful to scan a wider set of health focused AI opportunities using the 39 healthcare AI stocks.

With Krystal Biotech trading around $359.93 and an intrinsic value estimate that signals a sizable discount, yet sitting slightly above analyst targets, investors are left with a key question: Is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 11.5% Overvalued

Krystal Biotech closed at $359.93, while the most followed narrative pegs fair value at $322.78, pointing to a richer price than that framework implies.

The expansion of Krystal's pipeline, including imminent and near-term clinical readouts in lung disease (AATD, CF), ophthalmology, oncology (NSCLC), and aesthetics, leverages increased R&D productivity, which could drive future revenue growth and diversify earnings beyond a single product.

Favorable dynamics in global healthcare, such as greater willingness to reimburse curative, high-value genetic therapies and broadening awareness due to successful launches and patient outcomes, should support sustainable long-term revenue growth and premium pricing, boosting revenue visibility and potentially net margins.

Want to see how this pipeline story translates into that fair value? The core narrative leans on rapid top line expansion, rising profitability, and a richer future earnings multiple. The exact mix of those assumptions may surprise you.

Result: Fair Value of $322.78 (OVERVALUED)

However, Krystal Biotech's heavy reliance on VYJUVEK and the uncertainty around international reimbursement decisions both have the potential to unsettle that growth-focused narrative.

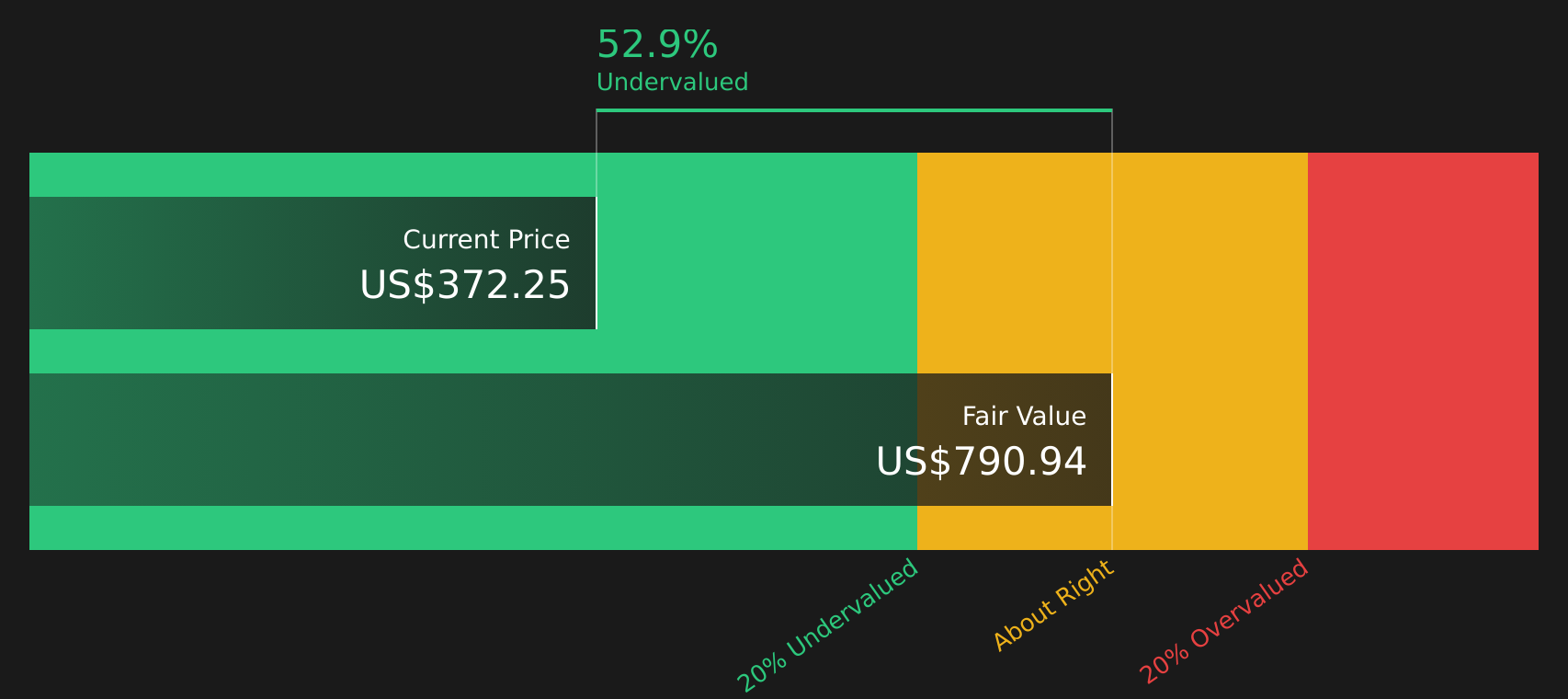

Another View: Krystal Biotech Through a Cash Flow Lens

The earlier section highlighted that Krystal Biotech trades around $359.93 compared with an analyst fair value of $322.78, which frames the stock as 11.5% richer than that narrative suggests. Our DCF model presents an estimated future cash flow value of $794.48, or roughly 54.7% above the current price. This comparison raises a key question: is the current pricing better interpreted as a premium on near term earnings, or as a discount to longer term cash flows?

To understand how this cash flow view is built and what would need to hold true for it to be reasonable, take a closer look at the SWS DCF model behind Krystal Biotech's valuation using the Look into how the SWS DCF model arrives at its fair value..

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Krystal Biotech for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between Krystal Biotech's perceived premium and its long term cash flow potential, it makes sense to move quickly, review the underlying data, and weigh both the downside and upside signals for yourself using the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Krystal Biotech?

If Krystal Biotech has sharpened your focus, do not stop here; broaden your watchlist now with a few targeted stock ideas that fit different goals.

- Lock in potential income by reviewing companies built around reliable payouts using the 9 dividend fortresses.

- Target quality at a sensible price by scanning companies that look attractively priced on fundamentals through the 43 high quality undervalued stocks.

- Dial back risk by focusing on businesses with steadier profiles using the 67 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.