LandBridge (LB) Stock After Higher 2026 EBITDA Outlook Is The Valuation Discount Still There

LandBridge LB | 0.00 |

Why LandBridge (LB) Is Back on Investors’ Radar

LandBridge (LB) has drawn fresh attention after management lifted its full-year 2026 adjusted EBITDA outlook to a range of $210 million to $230 million, citing a more supportive macro backdrop.

Despite a 1-day share price return of 2.76% taking LandBridge to $69.29, the stock is still down 7.35% over 90 days and its 1-year total shareholder return has declined 3.78%. This suggests momentum has cooled, even as the upgraded 2026 EBITDA outlook and recent earnings miss keep debate focused on growth potential versus risk.

If you are weighing LandBridge’s setup alongside other opportunities tied to energy infrastructure and long-term projects, it can be useful to see how similar themes play out across 35 power grid technology and infrastructure stocks

With LandBridge shares at $69.29, an intrinsic value estimate that implies a 29.44% discount, and analyst targets sitting higher, you have to ask whether the pullback is mispricing future growth or if the market already has it right.

Most Popular Narrative: 13.8% Undervalued

At $69.29, the most followed narrative pegs LandBridge’s fair value closer to $80.43, putting a spotlight on how future projects and margins are expected to evolve.

LandBridge's capital-light model and focus on long-term, fee-based contracts (e.g., triple-net leases and surface use royalties now making up 94% of revenue) enhance free cash flow generation and lead to greater earnings resiliency, even in periods of commodity price weakness, positively affecting both EBITDA margins and cash flow stability.

Want to see what sits behind that confidence in long term cash flows? The narrative leans on rapid revenue expansion, surging earnings, and a future margin profile that looks very different from today.

Result: Fair Value of $80.43 (UNDERVALUED)

However, investors still need to factor in execution delays on projects like DBR Solar and LandBridge’s heavy concentration in the Permian, which could challenge that optimism.

Another Way to Look at Valuation

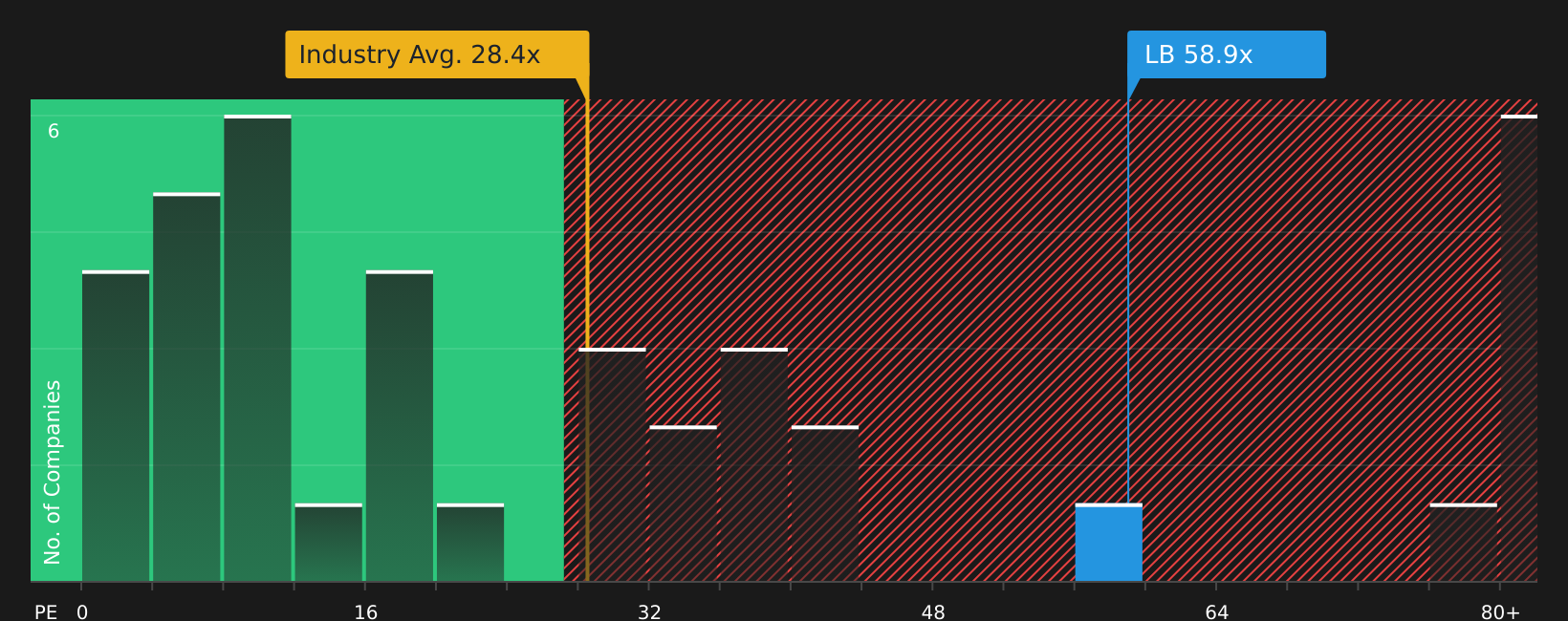

The narrative and intrinsic value work point to upside, but the current P/E of 60.9x tells a tougher story. It sits well above the US Real Estate industry at 28.5x, peers at 43.6x, and an estimated fair ratio of 47.1x. This tilts the risk toward overpaying if expectations cool.

That kind of gap between today’s P/E and the fair ratio is exactly where sentiment swings can bite. It is worth asking whether you are paying up for growth that is already in the price, or if this premium still feels comfortable for your time horizon and risk tolerance.

Next Steps

With the mix of optimism and caution in this story, it makes sense to move quickly and test the numbers for yourself. To see how the trade off between risks and rewards really looks for your own approach, start by checking the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you stop with just one stock, you may miss other opportunities that better fit your goals, risk comfort, and income needs across different parts of the market.

- Target steady compounding by reviewing companies trading below intrinsic estimates and backed by solid fundamentals through the 44 high quality undervalued stocks.

- Strengthen your income stream by scanning for high-yielding companies that aim to support consistent payouts using the 8 dividend fortresses.

- Dial back portfolio risk by focusing on companies with resilient finances and lower risk scores via the 70 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.