Las Vegas Sands (LVS) Q4 Revenue Growth Tests Bullish Community Narratives On Profit Margins

Las Vegas Sands Corp. LVS | 54.34 | +0.04% |

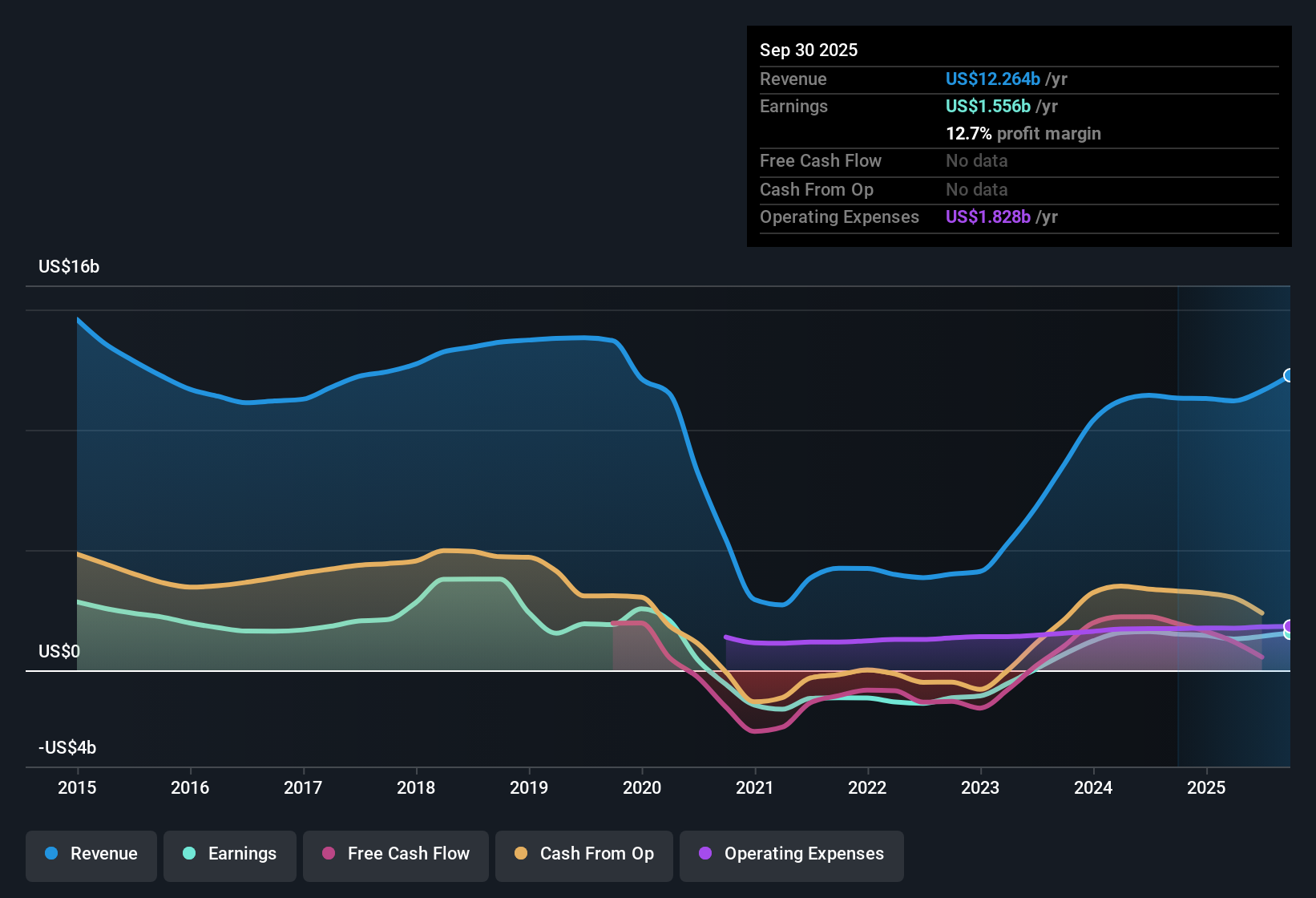

Las Vegas Sands (LVS) closed out FY 2025 with Q4 revenue of US$3.6b and basic EPS of US$0.59, alongside net income of US$395m that helped lift its trailing twelve month totals to US$13.0b of revenue and US$1.63b of net income. The company has seen quarterly revenue move from US$2.9b in Q4 2024 to US$3.6b in Q4 2025, while basic EPS over that span went from US$0.45 to US$0.59. This sets up a story where investors are weighing that earnings profile against slightly softer net margins.

See our full analysis for Las Vegas Sands.With the headline numbers on the table, the next step is to see how this earnings print lines up with the widely followed narratives around Las Vegas Sands, and where the story investors tell themselves might need an update.

TTM earnings climb to US$1.6b

- Over the last twelve months, Las Vegas Sands generated US$13.0b in revenue and US$1.63b in net income, with basic EPS at US$2.35, compared with US$11.3b revenue and US$1.45b net income a year earlier.

- Supporters of a bullish view often point to this earnings profile as a strength, and the data here leans in that direction:

- Earnings grew 12.5% over the past year and have averaged very strong annual growth over the past five years, while revenue growth is quoted at 4.8% per year, so profit growth has outpaced sales.

- Net profit margin sits at 12.5% versus 12.8% a year earlier, which means profitability has stayed close to prior levels rather than moving sharply away from that recent history.

Margins steady at 12.5% with higher quarterly run rate

- Q4 2025 revenue of US$3.6b and net income of US$395m imply a quarterly net margin close to the 12.5% level seen over the trailing twelve months, while quarterly revenue has moved from US$2.9b in Q4 2024 to US$3.6b in Q4 2025.

- Critics with a more bearish tilt might argue that a roughly stable margin limits the upside story, and the numbers give a mixed picture for that view:

- The trailing margin of 12.5% is only slightly below last year’s 12.8%, so the concern that profitability is weakening sharply is not strongly reflected in these figures.

- At the same time, net income in the latest four quarters of US$1.63b against revenue of US$13.0b leaves little sign of a margin breakout, which may matter to anyone hoping for a step change in profitability.

Mixed signals from 23.9x P/E and DCF fair value

- Las Vegas Sands trades on a 23.9x P/E, below a 33.2x peer average but above the 22x US Hospitality industry average, while a DCF fair value of US$27.95 sits well below the current share price of US$57.80 and analysts have an average target of US$69.98.

- What is interesting for investors leaning toward a bullish angle is how growth and valuation indicators line up against each other:

- Earnings are forecast to grow about 13.5% per year after a 12.5% increase over the past year, which lines up with that higher analyst target of US$69.98 compared with the current US$57.80 share price.

- On the other hand, the DCF fair value of US$27.95 and a flagged weakness in debt coverage by operating cash flow highlight that some valuation models and risk checks are more cautious than the higher growth and P/E comparisons might suggest.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Las Vegas Sands's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Las Vegas Sands pairs steady 12.5% margins and a 23.9x P/E with a DCF fair value of US$27.95 that sits well below its US$57.80 share price.

If that valuation gap makes you cautious about paying up here, you might instead put your capital to work by scanning our 53 high quality undervalued stocks, which aim to offer more attractive price tags relative to their fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.