Leidos (LDOS) Earnings Growth Exceeds 5-Year Average, Reinforcing Bullish Valuation Narrative

Leidos Holdings, Inc. LDOS | 158.82 | +1.80% |

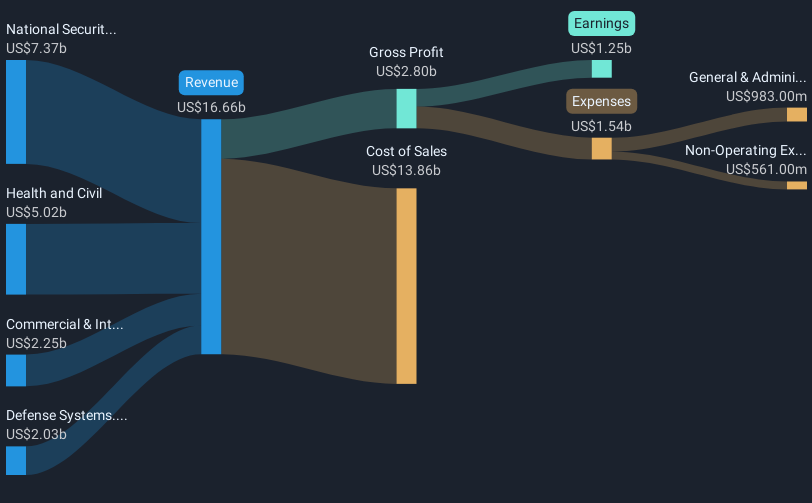

Leidos Holdings (LDOS) posted 16.9% earnings growth for the past year, outpacing its five-year average of 13.7% per year. Net profit margin also improved to 8.1% from last year’s 7.4%, while management continues to deliver high-quality results. Looking ahead, consensus expects earnings to increase by 3.5% per year and revenue by 2.7%, both trailing the broader U.S. market averages.

See our full analysis for Leidos Holdings.Next, we will see how these headline numbers compare to the current market narratives and whether consensus views are supported or challenged by the latest results.

Recurring Service-Based Revenues Enhance Earnings Stability

- Leidos’ business mix has shifted further toward recurring, service-based and software-driven revenue streams, including areas like health IT, logistics, and cloud-native platforms. This transition creates more predictability for future profits because these segments offer reliable cash flow and enhance earnings visibility.

- According to analysts' consensus view, this trend supports higher valuation multiples, as recurring revenues and improved profit stability allow the market to assign greater value to Leidos’ future earnings.

- Consensus narrative notes the importance of recurring revenues in insulating against market swings and highlights that higher-quality contracts, particularly those that integrate AI and modernization efforts, contribute to net margin durability.

- This shift is considered a foundation for maintaining long-term profitability, even if headline revenue growth slows in comparison with the broader market.

See the full consensus narrative on how recurring revenues support a resilient profit outlook. 📊 Read the full Leidos Holdings Consensus Narrative.

Disciplined Valuation Shows Discount to Peers

- Leidos trades at a P/E ratio of 18.2x, below both the industry average (25x) and its peer average (40.2x). The recent share price of $199.55 remains well under the DCF fair value estimate of $308.55.

- Analysts' consensus view links this discounted valuation to the company’s consistent margin profile and sustained growth, presenting Leidos as a compelling value compared to industry peers.

- This valuation gap reflects expectations for continued margin expansion but also acknowledges that growth rates for both revenue (2.7% projected per year) and earnings (3.5% per year) are now trailing the broader U.S. market.

- Market participants appear willing to assign a lower multiple as long as Leidos maintains earnings quality and profit stability. However, a material slowdown or missed integration targets could close this value gap quickly.

Profit Margins Stand Strong Amid Industry Pressures

- Net profit margin improved to 8.1%, up from last year’s 7.4%, despite widespread industry margin pressures and consolidation that could have weighed on results.

- Analysts' consensus view finds this improved margin especially meaningful because it comes as Leidos increases exposure to premium-priced digital and AI-driven contracts.

- Consensus highlights government-funded projects and modernization initiatives, such as air traffic automation, as key drivers supporting not only margin durability but also enhanced contract win rates and future pipeline stability.

- Even as profit margins are expected to edge down (to 8.1% in three years), the current resilience demonstrates Leidos' ability to defend profitability while some rivals may face greater compression.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Leidos Holdings on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Looking at the data from a unique angle? Shape your own view and add your perspective in just a few minutes. Do it your way

A great starting point for your Leidos Holdings research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

While Leidos Holdings continues to post solid profitability and margin gains, the company’s slower projected growth now trails broader U.S. market averages.

If you’re seeking stocks with more consistent growth momentum and steadier gains, check out stable growth stocks screener (2078 results) designed for investors focused on reliable, expanding performance through changing markets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.