Littelfuse (LFUS) Valuation Check After Mixed Results Guidance And Dividend Announcement

Littelfuse, Inc. LFUS | 346.54 | +0.30% |

Littelfuse (LFUS) shares are in focus after the company reported fourth quarter and full year 2025 results, issued first quarter 2026 sales guidance of US$625 million to US$645 million, and affirmed a US$0.75 dividend.

The earnings release, new first quarter 2026 sales guidance and confirmed dividend appear to be landing against a supportive backdrop, with a 30 day share price return of 12.99% and a 1 year total shareholder return of 33.85% suggesting momentum has been building recently.

If Littelfuse’s move has you looking at other electronic and auto related names, this could be a useful moment to scan auto manufacturers for additional ideas.

So with Littelfuse shares up strongly over the past year and the stock trading only slightly below the US$321.25 analyst target, is the recent net loss already reflected in the price, or is the market quietly betting on future growth?

Most Popular Narrative: 3.7% Undervalued

At a last close of $296.17 versus a narrative fair value of $307.50, Littelfuse is framed as modestly undervalued, with that view built on detailed growth and margin assumptions.

The rapid buildout of renewable energy infrastructure, grid storage, and sustainable grid ecosystems is resulting in double-digit sales growth and a robust opportunity pipeline for Littelfuse, positioning the company to benefit from continued secular tailwinds and expanding its addressable market, which should positively impact both revenues and margins.

Curious what sits behind that growth story? The most followed narrative leans heavily on rising earnings power, richer margins, and a future valuation multiple that has to compress meaningfully. If you want to see exactly how those moving parts stack up to reach a fair value above today’s price, check the full narrative to see the assumptions laid out line by line.

Result: Fair Value of $307.50 (UNDERVALUED)

However, that upbeat story could unravel if power semiconductor demand weakens further, or if acquisitions and new technologies prove harder to integrate than expected.

Another View: Rich P/E Puts Pressure On The Story

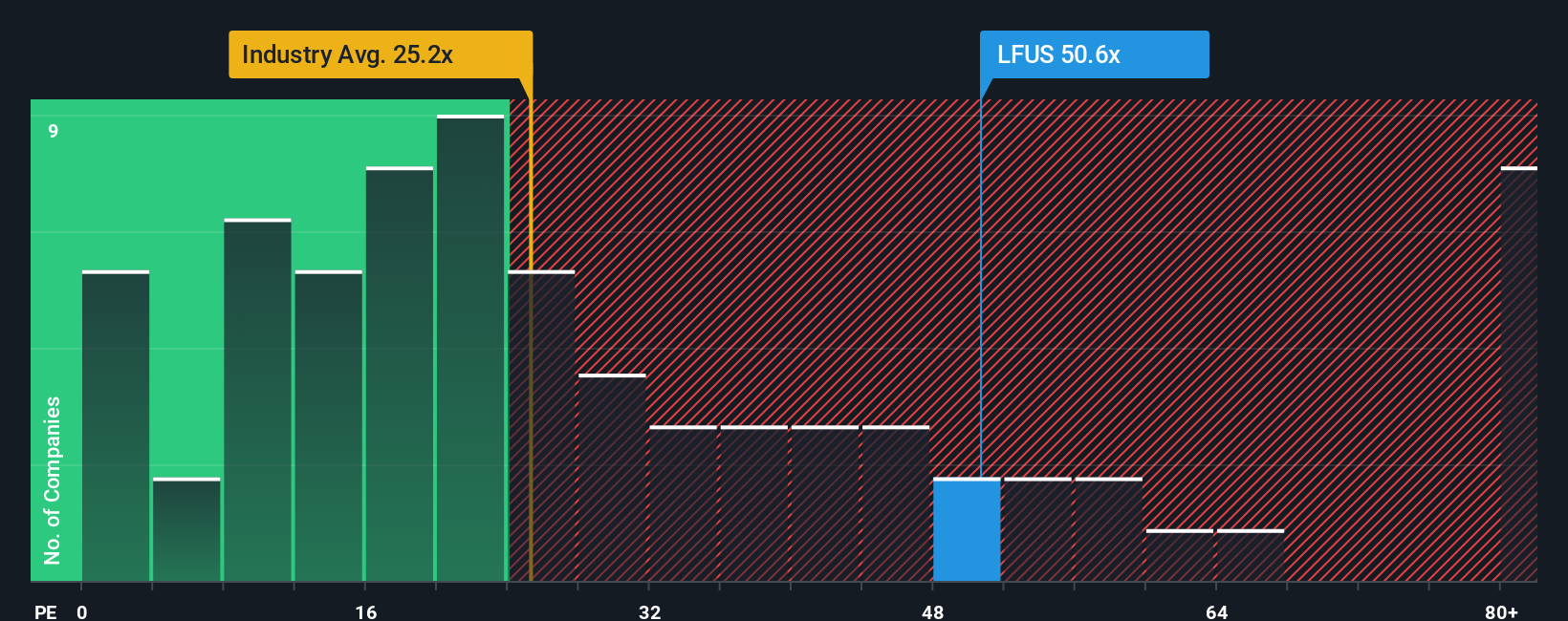

That 3.7% “undervalued” narrative sits awkwardly next to Littelfuse’s current P/E of 62.2x, which is well above the US Electronic industry average of 27.1x, a peer average of 46x, and a fair ratio of 30.2x that the market could eventually gravitate toward. With the share price already above the SWS DCF estimate of $293.46, do you see more room for optimism here, or more valuation risk?

Build Your Own Littelfuse Narrative

If you see the numbers differently or just prefer to test your own assumptions directly against the data, you can build a complete narrative in a few minutes and tailor every input to your view: Do it your way.

A great starting point for your Littelfuse research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Littelfuse has caught your attention, do not stop there. Use the Simply Wall St Screener to quickly surface focused stock ideas without scrolling through endless tickers.

- Scan these 3511 penny stocks with strong financials to find smaller companies that already show stronger financial footing than many tiny peers.

- Explore the development of artificial intelligence by checking these 24 AI penny stocks that are directly tied to this technology trend.

- Look for potential mispricings with these 876 undervalued stocks based on cash flows that screen for companies priced below what their cash flows might suggest.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.