Major Guam Defense Contract Could Be A Game Changer For Tutor Perini (TPC)

Tutor Perini Corporation TPC | 0.00 |

- Tutor Perini Corporation recently announced it secured a US$651.8 million task order from NAVFAC Pacific to harden critical electrical feeders at Naval Base Guam by replacing overhead distribution lines with underground, concrete-encased duct-bank circuits through a joint venture with its Guam-based subsidiary, Black Construction.

- This long-duration defense infrastructure project, which will be added to Tutor Perini’s second-quarter 2026 backlog, underscores the company’s role in complex Indo-Pacific military work and enhances visibility on future workloads.

- We’ll now examine how this sizeable Indo-Pacific defense contract, and its addition to backlog, influences Tutor Perini’s existing investment narrative.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

Tutor Perini Investment Narrative Recap

To own Tutor Perini, you need to believe the record US$21.1 billion backlog can be converted into steadier profits while legacy project risks and litigation remain contained. The new US$651.8 million Guam task order reinforces backlog and Indo Pacific defense exposure, but does not meaningfully change the near term execution risk around mega projects or the ongoing sensitivity to large, fixed price contracts.

The recent launch of share repurchases, with 277,578 shares bought back for US$19.99 million in early 2026, is the clearest recent signal on capital allocation alongside the Guam award. Against a backdrop of improving profitability and debt reduction, this combination of buybacks and long duration defense work may influence how investors weigh backlog quality against lingering margin and project risk.

Yet beneath the record backlog and headline contract wins, there is a concentration and execution risk profile that investors should be aware of...

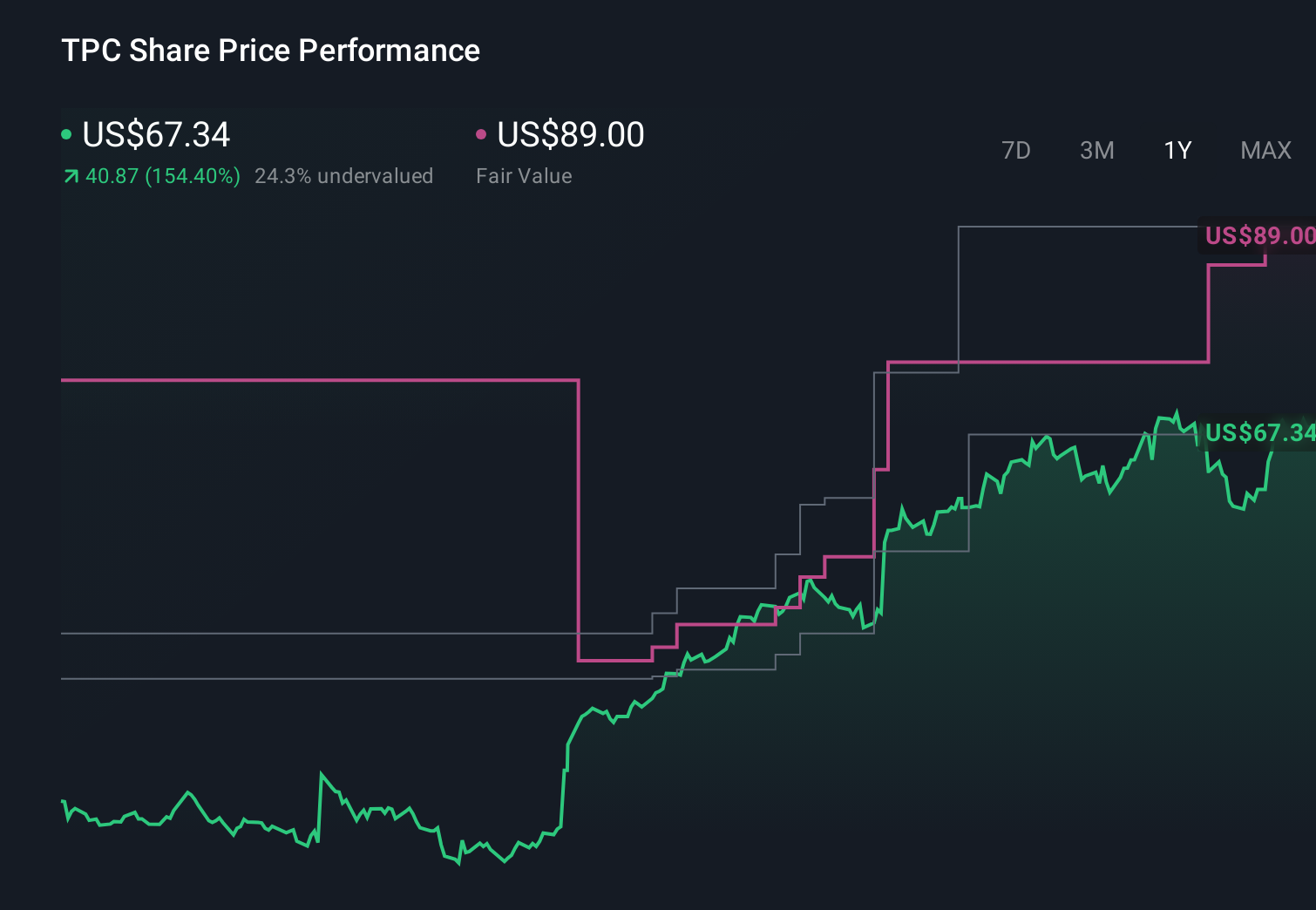

Tutor Perini's narrative projects $7.6 billion revenue and $483.9 million earnings by 2029. This requires 10.2% yearly revenue growth and a roughly $405.8 million earnings increase from $78.1 million today.

Uncover how Tutor Perini's forecasts yield a $113.25 fair value, a 45% upside to its current price.

Exploring Other Perspectives

Some of the most cautious analysts, who were assuming revenue of about US$7.9 billion and earnings of roughly US$299.6 million by 2029, focus on how labor shortages and rising workforce costs could squeeze margins even with large awards like Guam. Their view shows just how far opinions can differ and why it can be useful to compare several scenarios before deciding how this new contract might reshape expectations.

Explore 5 other fair value estimates on Tutor Perini - why the stock might be worth as much as 99% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Tutor Perini research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Tutor Perini research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Tutor Perini's overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.