Marathon Petroleum (MPC) Rallies Before Earnings, Is The Upside Already Priced In?

Marathon Petroleum Corporation MPC | 0.00 |

Recent Stock Move and Upcoming Earnings Focus

Marathon Petroleum (MPC) has drawn attention after a 2.2% gain in its latest session to $303.40, extending an 18% rise over the past month as investors look ahead to its August 4 earnings report.

For context, Marathon Petroleum’s recent 18% one month share price return builds on strong momentum, with a year to date share price return of 83.72% and a five year total shareholder return above 500%.

If strong recent gains in Marathon Petroleum have you thinking about where else momentum and cash flows might line up, it could be worth reviewing 34 power grid technology and infrastructure stocks.

After an 18% one month run and a share price near $303, is Marathon Petroleum still offering meaningful upside, or has the bulk of the opportunity already been priced in as earnings approach and valuation comes into focus?

Most Popular Narrative: 11.7% Overvalued

Compared with the last close at $303.40, the most followed narrative on Marathon Petroleum points to a fair value of $271.59 using a 7.11% discount rate.

Strategic portfolio optimization, including high return refinery "quick hit" projects and ongoing expansion in midstream logistics/NGL infrastructure (such as the Northwind Midstream acquisition), are enhancing operational flexibility and supporting incremental improvement in net margins and long term cash flow generation.

Want to see how this feeds into that $271.59 fair value for Marathon Petroleum? The narrative quietly leans on margin shifts, cash flow strength, and a lower future earnings multiple. The full breakdown shows how those moving pieces fit together.

Result: Fair Value of $271.59 (OVERVALUED)

However, the narrative around Marathon Petroleum can quickly shift if refining margins compress or if environmental policy tightens and pressures long term demand for its core fuels.

Another View: Cash Flow Signals for Marathon Petroleum

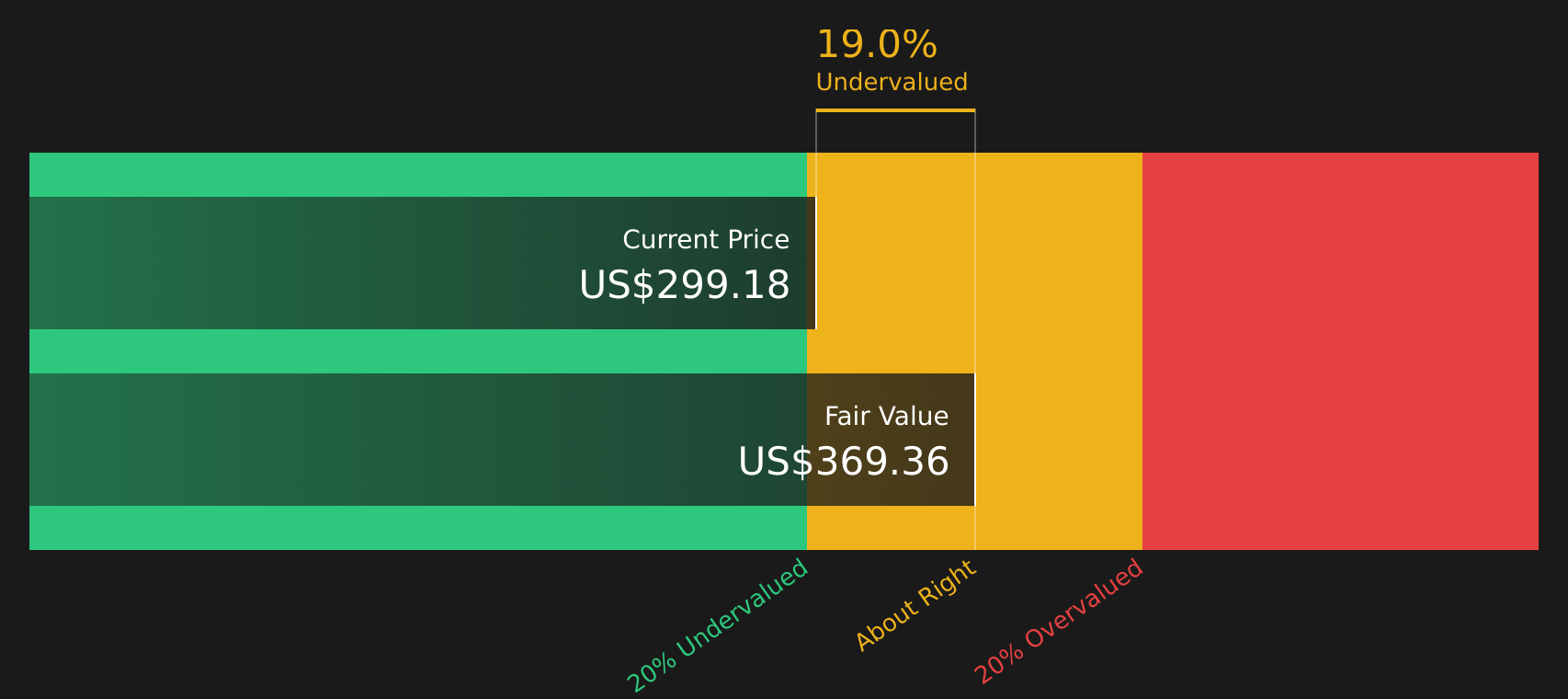

The analyst narrative puts Marathon Petroleum’s fair value at $271.59, about 11.7% below the current $303.40 share price. Our DCF model tells a different story, with an estimate of $369.36 that sits roughly 17.9% above today’s price and presents the stock as undervalued based on cash flow assumptions.

If that gap between analyst targets and the SWS DCF model has you wondering which lens to trust more, it can help to see exactly how the cash flows are treated and what would need to change for the two views to align. Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Marathon Petroleum for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals around Marathon Petroleum’s valuation and outlook, the real question is how the balance of risks and rewards looks to you right now. It is worth scanning both sides of the ledger, starting with 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Marathon Petroleum?

Do not stop with Marathon Petroleum. Use the Simply Wall Street Screener to check other stocks where quality, income, and resilience could better match your portfolio goals.

- Target reliable income and potential stability by scanning companies that show up in the 8 dividend fortresses.

- Spot opportunities where fundamentals and price look aligned by running through the 44 high quality undervalued stocks.

- Prioritise resilience and capital protection by reviewing stocks highlighted in the 79 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.