Marathon Petroleum (MPC) Stock Looks Cheap Even With Mixed Valuation Signals

Marathon Petroleum Corporation MPC | 0.00 |

Marathon Petroleum has delivered a very large 5 year gain for shareholders, yet its current share price around US$280.68 still screens below an intrinsic value estimate from a Discounted Cash Flow (DCF) model, while the broader valuation checks point to a more mixed picture.

- Over the past 5 years, Marathon Petroleum has returned roughly 4.7x an initial investment. This puts extra focus on whether the current valuation leaves enough room for future upside.

- A softer crude price backdrop can support refining margins for Marathon Petroleum. However, any sustained pressure on global fuel demand remains a key risk for how much cash flow investors are willing to pay for.

- On Simply Wall St's checks, Marathon Petroleum screens as attractively priced on some measures but not others. 3 of 6 valuation checks currently point to value, which is a mixed picture rather than a clear bargain.

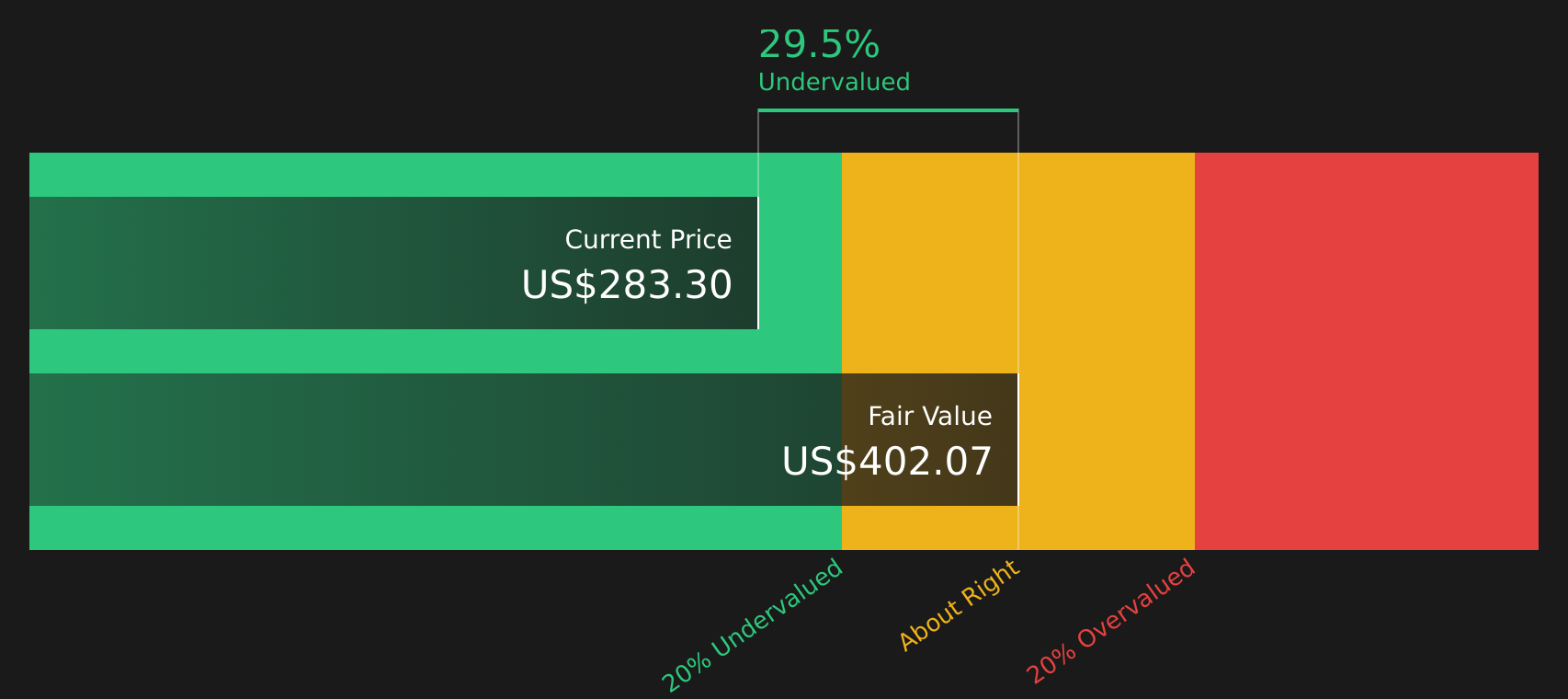

The issue now is whether Marathon Petroleum's current share price already reflects its cash flow potential or if the DCF implied discount of about 30.2% still offers a margin of safety.

Is Marathon Petroleum a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) method values Marathon Petroleum by projecting future cash the business could return to shareholders and discounting it back to today. On this model, Marathon Petroleum's latest twelve month free cash flow of about $6.7b feeds into a 2 Stage Free Cash Flow to Equity framework that assumes cash flows ease back from current levels over time.

Those projections produce an estimated intrinsic value of about $402 per share, compared with the current share price near $280.68, implying the stock screens roughly 30.2% undervalued on this cash flow view. Because recent commentary highlights refiners such as Marathon Petroleum as potential beneficiaries of softer crude prices, the current discount suggests the market is still cautious about how durable these cash flows will be.

On this DCF view, Marathon Petroleum stock currently appears undervalued relative to the cash flows investors are pricing in.

Our Discounted Cash Flow (DCF) analysis suggests Marathon Petroleum is undervalued by 30.2%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Does Marathon Petroleum Look Fairly Valued on Earnings?

P/E works well for Marathon Petroleum because earnings are a key driver for how investors usually compare refiners. Marathon Petroleum currently trades on a P/E of about 17.7x, which is slightly above the peer average of around 16.9x and higher than the wider Oil and Gas industry average of roughly 13.4x.

On Simply Wall St's model, a fair P/E for Marathon Petroleum is estimated at about 18.1x, which is close to where the stock currently sits. That indicates the market is pricing Marathon Petroleum broadly in line with what this framework implies for its earnings profile and risk, even though the sector as a whole trades on lower multiples.

Overall, Marathon Petroleum stock appears roughly fairly valued on its P/E multiple.

The Marathon Petroleum Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Marathon Petroleum pick up where the valuation checks leave off by spelling out which assumptions about Marathon Petroleum's growth, margins and earnings would need to hold for the stock to be worth materially more or less than its current price. Instead of a single point estimate, they set out the future conditions that figure relies on, so you can monitor whether those expectations continue to match what actually happens on Marathon Petroleum's Community page.

The community is split on Marathon Petroleum, with one camp focusing on potential upside from refinery and midstream projects while the other highlights long term demand and policy risks.

Bull case: 12% undervalued

"Refining investments at Galveston Bay, Garyville, Robinson and El Paso are aimed at converting lower value inputs into higher value products and improving reliability..."

Bear case: roughly fairly valued

"The company's large refining footprint, with ongoing investments into refining assets (e.g., in California and major multiyear projects), risks asset stranding or value impairment if environmental policies or carbon pricing become significantly stricter..."

Do you think there's more to the story for Marathon Petroleum? Head over to our Community to see what others are saying!

The Bottom Line

For Marathon Petroleum, the Discounted Cash Flow (DCF) intrinsic value estimate points to meaningful upside, while the P/E based view suggests the stock now trades roughly in line with what the market is prepared to pay for similar earnings profiles. That mixed message, alongside the existing valuation checks, makes the current setup less of a clear bargain and more of a judgment call on cash flow durability. The key swing factor from here is whether refining margins and long term fuel demand stay resilient enough to support the cash flows implied by the intrinsic value, rather than the market being correct that the discount reflects lasting risk.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.