Marathon Petroleum Stock Leads 3 Oil Exposure Picks As Inflation Fears Return

Marathon Petroleum Corporation MPC | 0.00 |

Rising Middle East tensions and fresh inflation worries are pulling oil back into the spotlight, and that ripple effect is running straight through parts of the stock market. With CPI running at 4.2% in May and oil costs feeding into everything from transport to consumer goods, some companies could see a lift from higher energy prices while others face tougher margin pressure. This article looks at three stocks exposed to the latest geopolitical and inflation headlines, highlighting one that may be positioned to benefit from the current setup and two where the risks from oil and pricing pressure appear more challenging.

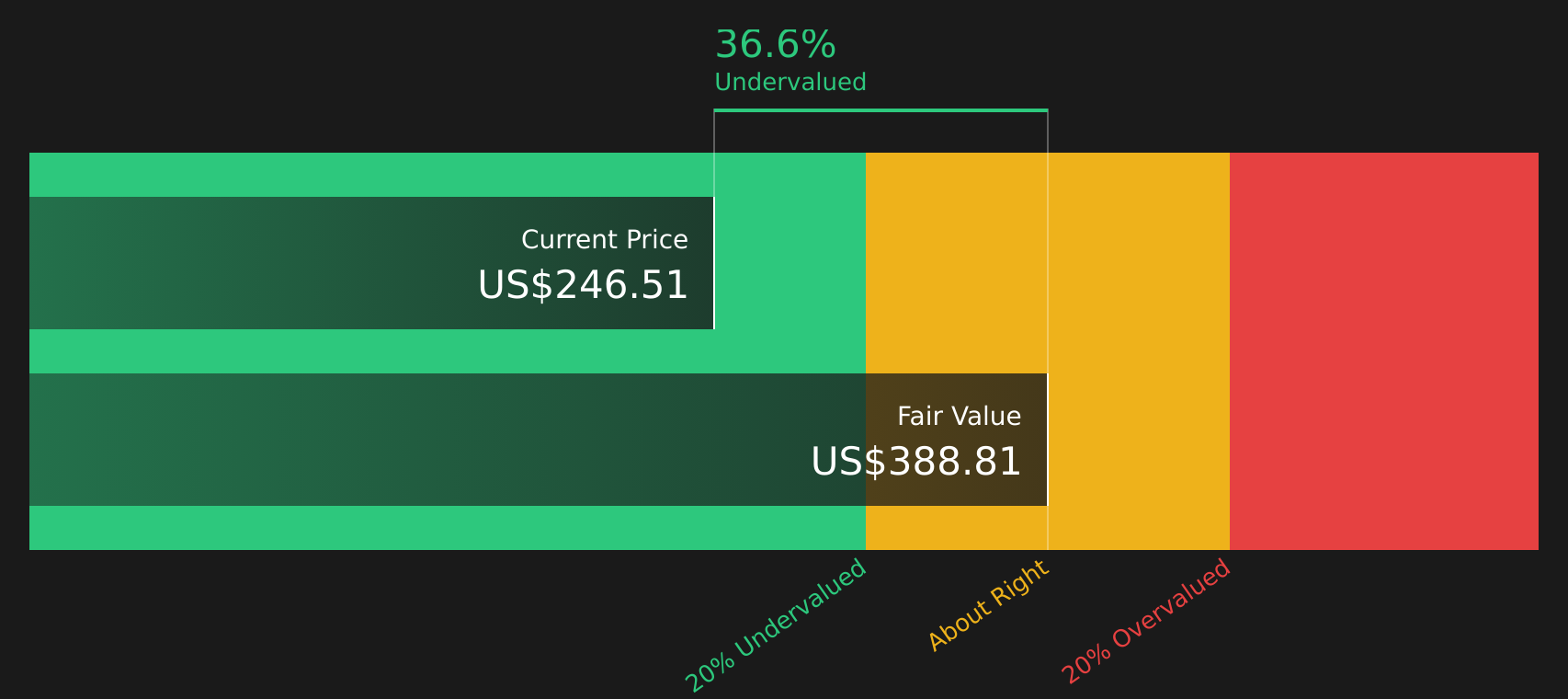

Marathon Petroleum (MPC)

Overview: Marathon Petroleum is a large US downstream energy company that refines crude oil into fuels and petrochemicals, moves those products through its midstream pipeline and logistics network, and produces renewable diesel sold through brands like Marathon and ARCO.

Operations: Marathon Petroleum generates most of its US$141.4b revenue from Refining & Marketing (US$127.2b), with additional contributions from Midstream (US$11.4b) and Renewable Diesel (US$2.8b), almost entirely in the United States (about US$136.2b).

Market Cap: US$72.19b

Marathon Petroleum sits at the intersection of rising oil prices and inflation worries, and that combination is a key reason it is attracting attention. Its large refining system and midstream arm can benefit when oil volatility widens refining margins, particularly with investments at sites like Garyville aimed at improving reliability and product mix. At the same time, earnings have been strong in the past year and the stock is trading below some fair value estimates, while management emphasizes buybacks and a 1.61% dividend. On the other hand, the company carries meaningful debt, faces regulatory and legal risks including a proposed pricing class action in California, and remains sensitive to refined fuel demand. How these positives and pressures balance out will be important for Marathon Petroleum.

Refining margins, buybacks and a 1.61% dividend make Marathon Petroleum look like a straightforward oil beneficiary, but the real story may sit in how its valuation stacks up against those strengths and emerging risks in the DCF valuation analysis for Marathon Petroleum

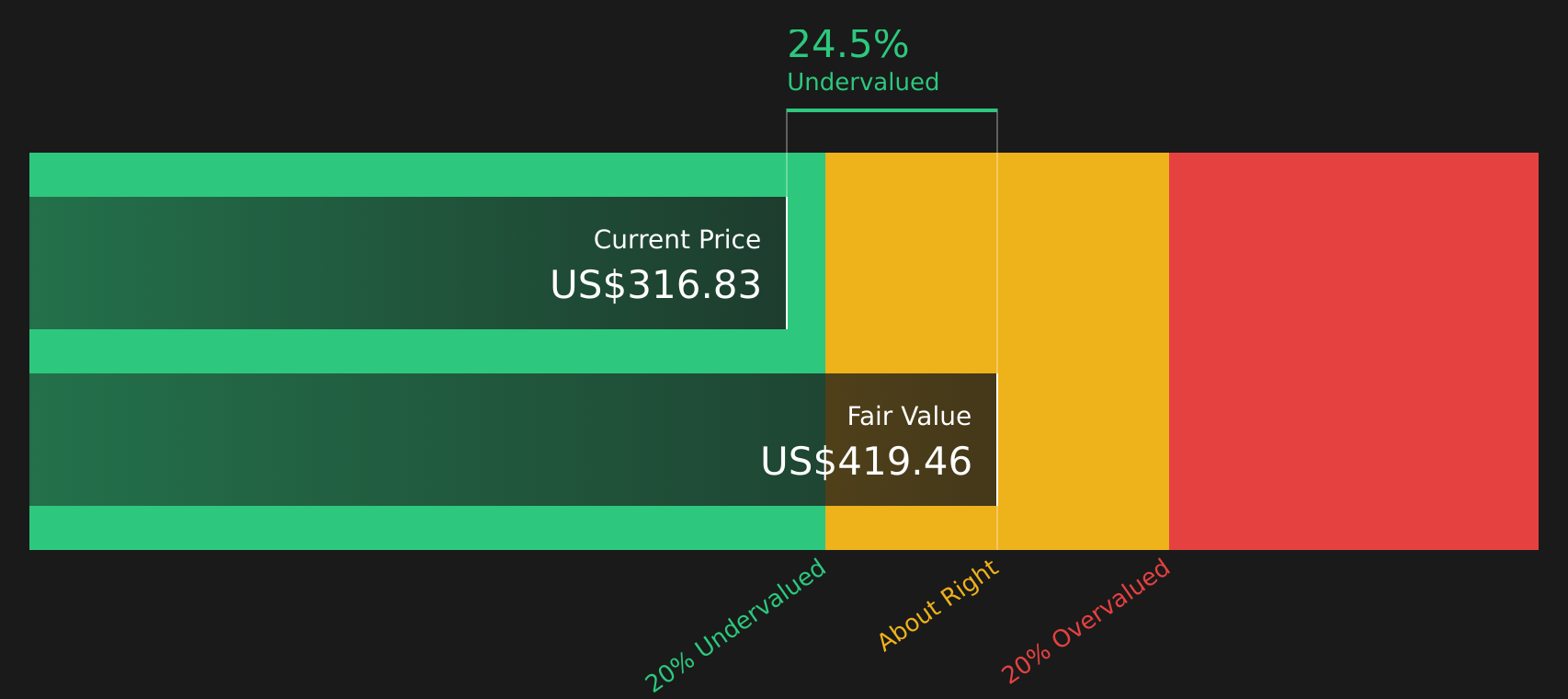

FedEx (FDX)

Overview: FedEx is a global logistics and delivery company that moves parcels and freight for consumers and businesses, while also offering e-commerce solutions, printing, document services, and supply chain management from its Memphis headquarters to customers around the world.

Operations: FedEx generates most of its US$86.3b revenue from Federal Express at US$79.7b, with FedEx Freight contributing US$8.7b and Corporate, Other, and Eliminations at US$3.6b, across the U.S. (US$66.1b) and international markets (US$25.9b).

Market Cap: US$78.45b

FedEx sits in a difficult spot when oil prices jump, because higher fuel costs can quickly eat into margins just as the company is trying to prove that its cost cutting, Network 2.0 overhaul and recent FedEx Freight spin off can support more efficient earnings. The stock currently appears inexpensive on several valuation measures, and recent results highlight record margins and solid parcel demand. However, freight separation, elevated debt, modest forecast revenue growth and higher wage and transport costs leave little room for error if inflation remains elevated. For investors, the tension between the current valuation and the execution and macro risks around FedEx makes it important to understand the company’s position in detail over the coming years.

FedEx’s low valuation, higher fuel costs and rising wage burden appear to be moving in different directions, and the gap between the story and the numbers is widening. Before assuming the current price compensates for that execution risk, read the analysis report for FedEx

Procter & Gamble (PG)

Overview: Procter & Gamble is a global consumer goods company that sells everyday products such as detergents, shampoos, diapers, grooming tools and health care items through brands like Tide, Pampers, Gillette, Olay and Crest across major retail and online channels.

Operations: Procter & Gamble generates most of its revenue from Fabric & Home Care at US$30.27b, followed by Baby, Feminine & Family Care at US$20.45b, Beauty at US$15.78b, Health Care at US$12.42b, Grooming at US$6.90b and Corporate at US$0.90b.

Market Cap: US$343.89b

Procter & Gamble is often viewed as a classic defensive stock, with a wide moat, high ROE around 30.5% and a long dividend record. However, rising oil driven inflation highlights a weak spot in its heavy reliance on commodities, packaging and global logistics, at a time when consumers are becoming more price sensitive. Management has flagged hundreds of millions of dollars in extra costs tied to Middle East related supply and logistics disruptions, and analysts already expect only low single digit revenue and EPS growth. At the same time, the stock is supported by strong cash generation and a long history of dividend growth that can keep income focused investors interested. A key consideration is how much inflation and cost pressure Procter & Gamble can absorb before that quality premium starts to look stretched.

Procter & Gamble’s quality halo and long dividend record can mask how exposed it is to commodities, packaging and logistics costs. Before assuming that premium is safe, read the 4 key rewards and 1 important warning sign

Take Control of Your Investment Journey

If Procter & Gamble or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Markets can change quickly and the next breakout ideas may not stay quiet for long. Review fresh stock lists while momentum is still building and the data is most relevant, then consider opportunities at an early stage.

- Look for potential income opportunities by reviewing 7 dividend fortresses that aim to support cash flows even when prices are changing.

- Track under the radar growth by scanning 19 high quality undiscovered gems that combine solid fundamentals with stories many investors may not have focused on yet.

- Evaluate your risk management approach by checking 67 resilient stocks with low risk scores that emphasize resilience when volatility and inflation concerns increase.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.