Mastercard (MA) Faces Slower Card Growth As Fair Value Debate Builds

Mastercard MA | 0.00 |

Recent updates around Mastercard (MA) have shifted focus to the health of its core card business and rising European regulatory pressure, including progress toward a digital euro that aims to reduce reliance on non European networks.

Despite a steady stream of product launches, partnerships and regulatory headlines, Mastercard’s recent share price return has been weak, with the stock down 13.33% year to date and the 1-year total shareholder return declining 11.94%. The 3-year and 5-year total shareholder returns of 30.11% and 36.54% point to a stronger longer-term record.

If you want to broaden your search beyond Mastercard and tap into the next wave of payment and automation trends, take a look at 49 AI infrastructure stocks.

With Mastercard stock down this year despite ongoing product launches, AI driven payment initiatives and solid dividend continuity, the key question is whether recent weakness reflects an undervalued franchise or a market that is already pricing in future growth.

Most Popular Narrative: 34.9% Undervalued

According to the current narrative on Mastercard, a fair value of $750 per share sits well above the last close of $488.07, which puts a spotlight on why some investors see a wide gap between price and quality.

What it offers instead: a business that compounds safely, a payout growing at double-digit rates from a tiny base, and a price that does not currently reflect either of those things. Setups like that do not come around often, and the current pullback looks more like an entry point than a warning sign.

Curious how Mastercard gets to that higher fair value? The narrative leans heavily on earnings power, resilient margins and a future profit multiple usually reserved for fast growing platforms. Want to see which specific growth and margin assumptions support that $750 figure.

Result: Fair Value of $750 (UNDERVALUED)

However, Mastercard’s story can change quickly if European regulation tightens network fees faster than expected, or if new payment rails start to meaningfully chip away at card volumes.

Another View: Multiples Paint a Richer Picture for Mastercard

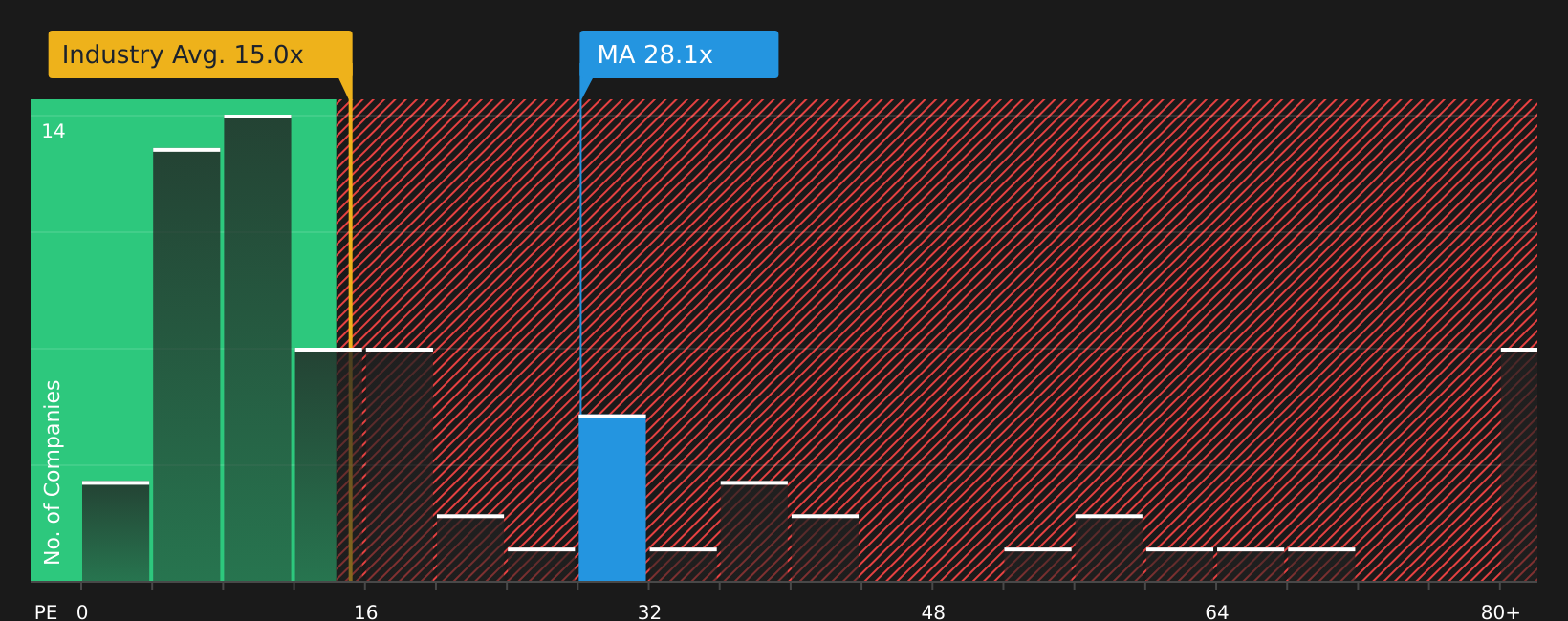

While the user narrative leans on a fair value of $750 per Mastercard share, the current P/E of 27.7x tells a different story. That multiple sits well above the estimated fair ratio of 20.7x, the US Diversified Financial industry average of 14.6x, and the peer average of 24.3x.

In practical terms, you are paying a clear premium for Mastercard relative to both its sector and closer peers, with the fair ratio hinting at where the market could eventually settle. The question is whether that premium feels like justified quality or valuation risk to you.

Next Steps

With Mastercard, the mix of optimism and concern is clear, so now is the time to look through the numbers yourself and decide where you stand. To weigh up both sides in one place and see how that balance of risk and reward looks to you, start with 4 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Mastercard?

If Mastercard has sharpened your thinking about quality and valuation, do not stop there. Broaden your watchlist with a few focused idea lists built from hard numbers.

- Target reliable income and long term stability by reviewing 7 dividend fortresses built around companies that keep cash flows and payouts front and center.

- Hunt for mispriced quality by checking out screener containing 19 high quality undiscovered gems that might not yet be crowded but still show strong underlying fundamentals.

- Dial down potential volatility by scanning 67 resilient stocks with low risk scores focused on businesses that score well on resilience instead of hype.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.