Mastercard (MA) Valuation Check After Q1 Beat And Yellow Card Stablecoin Partnership

Mastercard Incorporated Class A MA | 0.00 |

Mastercard (MA) just paired a better than expected Q1, with revenue of US$8,398 million and net income of US$3,882 million, with a Yellow Card partnership focused on stablecoin-based payments across emerging markets.

Despite the strong Q1 and the Yellow Card partnership, momentum in the stock has cooled. The 90 day share price return shows an 8.71% decline and the year to date share price return shows an 11.04% decline. In contrast, the 3 year total shareholder return of 32.98% and 5 year total shareholder return of 43.25% point to much stronger longer term results.

If you are interested in how digital payments, crypto and infrastructure trends are reshaping opportunities, it could be worth scanning 20 cryptocurrency and blockchain stocks

So with Mastercard stock down double digits year to date despite Q1 beats, a near 54% intrinsic discount flag and analysts seeing upside from around US$501, is this a genuine buying opportunity or is the market already pricing in future growth?

Most Popular Narrative: 3.7% Undervalued

According to the most followed narrative, Mastercard's fair value sits at $520, only a touch above the last close at $500.94, which suggests the recent pullback is not the whole story.

Mastercard is more than just a card network. It is a technology platform powering the global digital economy: secure, scalable, profitable, and increasingly diversified beyond swipe fees. With revenue growth, expanding VAS, cross-border strength, fintech-ready infrastructure (stablecoins, AI/analytics), and disciplined shareholder returns, Mastercard is described as well-positioned to compound dividends and earnings over the long term.

The key to this fair value is not just payment volume. It leans heavily on high margin services, sticky data products, and recurring cash flows that sit on top of the core network. Investors may be curious which growth and profitability assumptions matter most here, and how they connect back to that modest undervaluation gap.

Result: Fair Value of $520 (UNDERVALUED)

However, the Mastercard story can change quickly if regulation tightens around fees or data use, or if fintech and stablecoin rivals chip away at payment economics.

Another View: Multiples Signal a Richer Price Tag

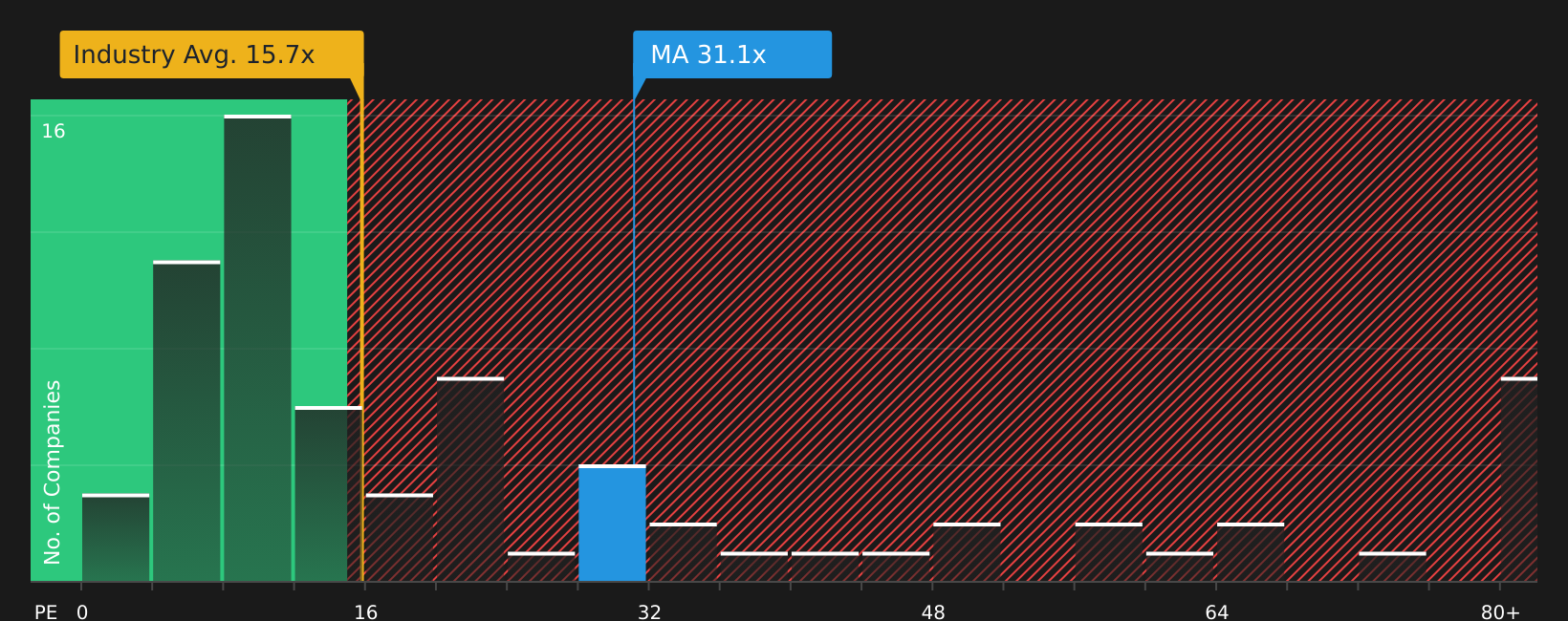

That 3.7% undervaluation narrative sits awkwardly beside Mastercard's current P/E of 28.4x, which is well above both the US Diversified Financial industry at 17.1x and the peer average at 19.2x, and even above a fair ratio of 20.2x that the market could move towards over time.

Those gaps suggest investors are already paying a premium for quality and growth, which can limit upside if expectations cool. The real question is whether you see that premium as justified or as valuation risk that could unwind.

Next Steps

With sentiment clearly split between valuation upside and downside risk, this is the moment to move quickly, review the numbers yourself, and weigh the 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Mastercard is on your radar, do not stop there. Use the tools available to spot other opportunities that fit your goals before the crowd gets there.

- Spot potential upside in quality companies trading below their estimated worth by scanning 51 high quality undervalued stocks.

- Strengthen your income stream by checking out stocks in 12 dividend fortresses.

- Prioritise resilience and capital protection by reviewing companies inside 71 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.