Merit Medical Systems (MMSI) On Employee Share Plan News And A Fair Value Debate

Merit Medical Systems, Inc. MMSI | 0.00 |

Merit Medical Systems (MMSI) has filed a US$35.865 million shelf registration for 500,000 common shares tied to an employee stock ownership plan, which gives investors fresh context for the stock’s recent price performance and valuation.

Against this employee stock ownership plan backdrop, Merit Medical Systems’ share price has rebounded with an 11.93% 1 month share price return. However, the stock remains down year to date with a 19.66% share price decline and a 25.73% drop in 1 year total shareholder return, pointing to improving short term momentum after a weaker stretch.

If you are comparing Merit Medical Systems with other healthcare related opportunities, it could be helpful to look at companies benefiting from medical and diagnostic AI, starting with 39 healthcare AI stocks

So with Merit Medical Systems trading below analyst price targets but rebounding in the short term, is the current share price still undershooting the company’s fundamentals, or is the market already pricing in any future growth potential?

Most Popular Narrative: 22.4% Undervalued

At a last close of $69.45 versus a narrative fair value of $89.55, Merit Medical Systems is framed as materially discounted, with that gap tied to specific growth and margin expectations rather than sentiment alone.

The expanding global prevalence of chronic diseases and an aging population are increasing the need for interventional, diagnostic, and therapeutic medical procedures. Merit's strong growth in cardiovascular and endoscopy segments, robust new product development, and recent acquisitions (such as Biolife and EndoGastric) position the company to capture a larger share of this growing market and drive sustained long-term revenue growth.

Want to see what revenue trajectory, margin lift, and future earnings multiple are baked into that $89.55 fair value? The narrative leans on steady expansion, richer profitability, and a premium valuation tag usually reserved for faster growing peers.

Result: Fair Value of $89.55 (UNDERVALUED)

However, the Merit Medical Systems narrative could be challenged if WRAPSODY CIE reimbursement delays persist or if tariffs and China pricing pressure weigh more heavily on margins and growth assumptions.

Another View: Merit Medical Systems Looks Rich On Earnings

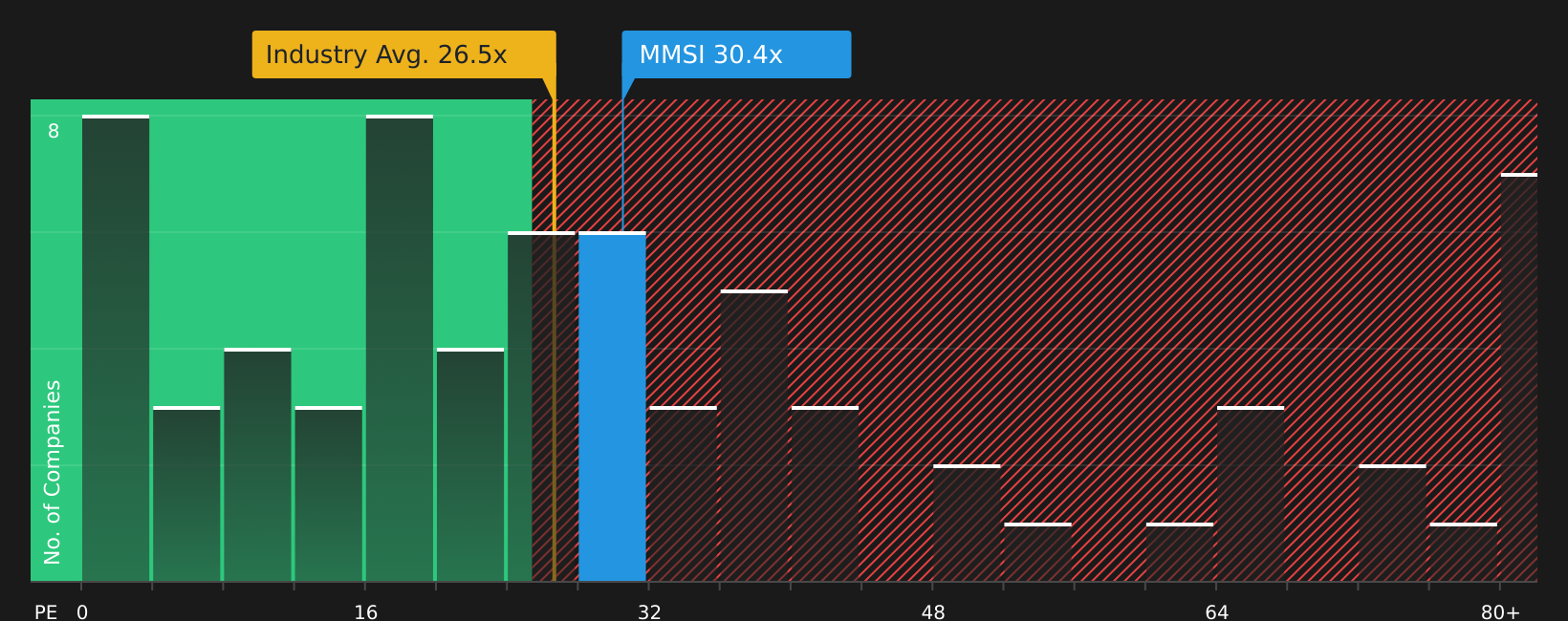

The first narrative frames Merit Medical Systems as around 22.4% undervalued against an $89.55 fair value, but the current P/E of 29.7x tells a tighter story. That multiple is higher than the US Medical Equipment industry at 25.6x and above a fair ratio of 23.1x.

Compared with peers averaging 42.8x, the stock does not look stretched across its group. However, the gap between 29.7x and the 23.1x fair ratio suggests limited room for disappointment if growth or margins come in below expectations, so which signal do you trust more?

Next Steps

If the mixed sentiment around Merit Medical Systems leaves you undecided, take a closer look at the underlying data and form your own view quickly by reviewing the 4 key rewards

Looking for more investment ideas beyond Merit Medical Systems?

If Merit Medical Systems has your attention, do not stop there. Use these focused stock lists to spot clear opportunities before they move out of reach.

- Target potential upside in quality stocks that look attractively priced by starting with 41 high quality undervalued stocks.

- Strengthen your portfolio with companies that pair financial resilience and healthy fundamentals by reviewing the solid balance sheet and fundamentals stocks screener (48 results).

- Unearth lesser known stocks with strong underlying metrics before they gain wider attention by checking the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.