Methanex And 2 Oil Import Stocks With Margin And Funding Risk

LyondellBasell Industries NV LYB | 0.00 |

The U.S. decision to grant a temporary license for Iranian oil exports adds a fresh twist to the energy story, with extra supply potential and questions around the Strait of Hormuz all feeding into cost expectations for heavy oil users. For companies in transportation, chemicals, and logistics, even small shifts in fuel prices can influence margins, pricing power, and investor sentiment. This article looks at 3 stocks from the Oil-Importing Industries screener that may warrant closer review in light of the current news backdrop, helping you decide whether they deserve a closer look or a spot on your watchlist.

Methanex (TSX:MX)

Overview: Methanex is a Vancouver based chemicals producer that focuses on making methanol and some ammonia, supplying large industrial customers across Asia Pacific, North America, Europe, and South America and supporting them with owned and leased storage and terminal infrastructure.

Operations: Methanex generates about US$3.7b in revenue primarily from the production and sale of methanol.

Market Cap: CA$5.8b

Investors looking at oil importing industries may find Methanex interesting because it turns natural gas and other hydrocarbons into methanol. Lower oil and energy prices can ease input costs at the same time that analysts are expecting earnings to improve. The company is working on production efficiency and capacity, while also planning to pay down debt, which together could support better cash generation if methanol demand holds up. That said, Methanex still reports losses, carries funding risk from its borrowings, and relies on contracted gas supplies, so any disruption or weaker pricing could pressure margins. How these moving pieces interact with shifting Iranian energy flows and methanol trade is where the real opportunity and risk balance sits.

Methanex’s push for efficiency and debt reduction could be a bigger swing factor than investors are pricing in, especially with energy costs in flux. As a result, it is worth lining this up against the 3 key rewards and 2 important warning signs (1 is major!)

LyondellBasell Industries (LYB)

Overview: LyondellBasell Industries is a global chemicals company that turns oil based feedstocks into plastics, chemicals, and fuels used in everyday products, from food packaging and home furnishings to car parts and paints. It also licenses production technology and catalysts to other petrochemical producers.

Operations: LyondellBasell generates most of its revenue from olefins and polyolefins in the Americas and in Europe, Asia and International at about US$9.8b and US$10.1b respectively, with additional contributions from Intermediates & Derivatives at US$8.8b and Advanced Polymer Solutions at US$3.4b.

Market Cap: US$19.4b

LyondellBasell Industries gives you exposure to a global chemicals producer that can benefit when oil prices ease, because cheaper feedstock can support margins across its large polyethylene, polypropylene and intermediates businesses. At the same time, the company is reshaping its portfolio toward recycling and lower cost regions. Analysts also note the context of a period of weak earnings, dividend reset pressure, and heavy use of external funding. Alongside its technology licensing and recycling projects, the trade off between potential cost relief from additional oil supply, longer term sustainability investments, and balance sheet risk is an important consideration for investors.

LyondellBasell Industries is reshaping its business around cheaper feedstocks, recycling and technology licensing, yet the real story sits in how its balance sheet and cash returns hold up in different oil scenarios. Get the full context in the 4 key rewards and 2 important warning signs (2 are major!)

DuPont de Nemours (DD)

Overview: DuPont de Nemours is a diversified materials and solutions company that supplies specialty products for healthcare, water treatment, construction, protective garments, transportation, aerospace, and packaging, often selling into critical applications like medical devices, water filtration systems, and protective Tyvek suits.

Operations: DuPont de Nemours generates about US$3.6b from Diversified Industrials and US$3.3b from Healthcare & Water Technologies, with the United States and EMEA among its key regions.

Market Cap: US$19.3b

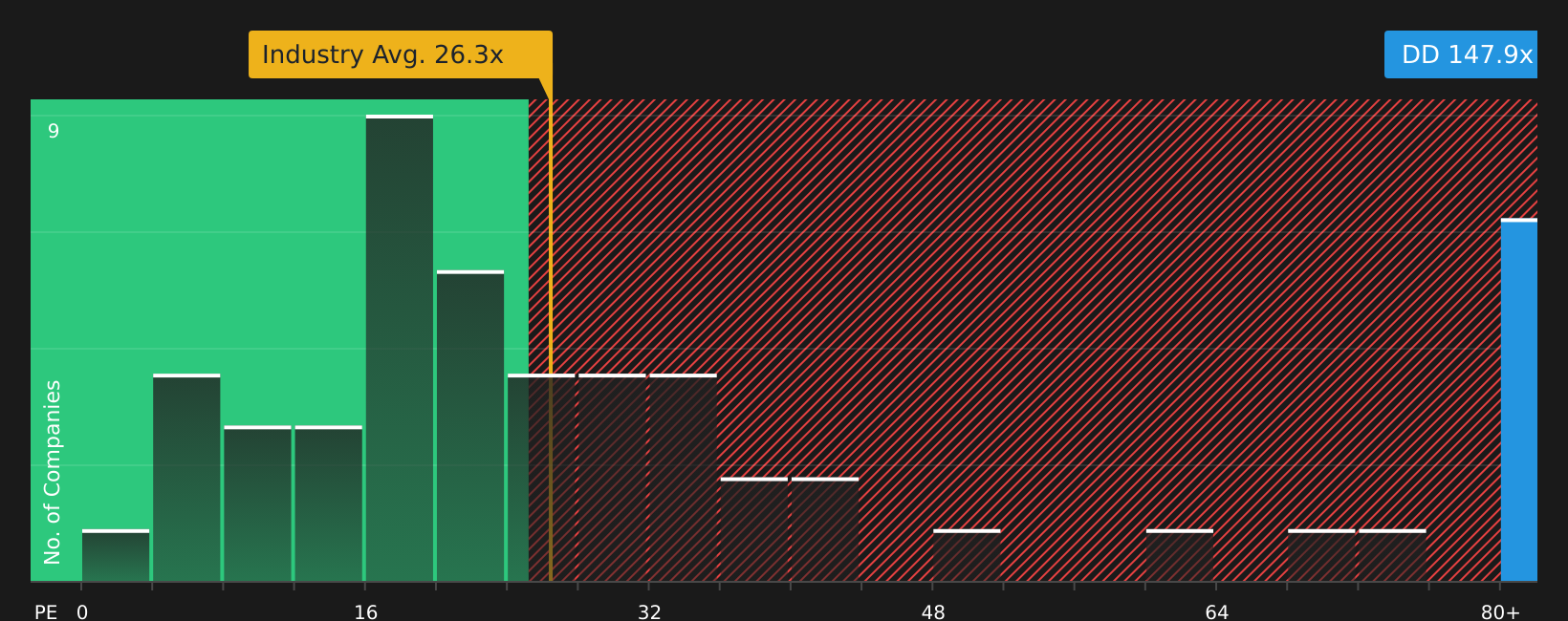

DuPont de Nemours is interesting in the Oil Importing Industries context because it combines energy intensive manufacturing with a focus on higher margin healthcare and water technologies. Lower oil prices can relieve cost pressure, and contracts such as the MemCor wastewater upgrade and new healthcare and Tyvek offerings support demand. The company has turned earnings positive and raised 2026 sales guidance, yet carries trade offs including a very high P/E, ongoing legal exposures, and relatively low forecast ROE, which leave little room for disappointment if input costs or Middle East logistics issues flare up again. For investors, the appeal lies in how this mix of cleaner cost tailwinds, water and healthcare growth, and residual legal and funding risks ultimately lines up against expectations for DuPont de Nemours over the next few years.

DuPont de Nemours is being priced for perfection, yet its very high P/E, legal exposures, and funding trade offs raise sharp questions about what the market is really baking in. Get the full narrative for DuPont de Nemours

The 3 stocks covered are only a starting sample. The full Oil Importing Industries screen has uncovered 42 more companies with equally compelling stories that you can review through the Oil-Importing Industries screener. Simply Wall St then lets you analyze and filter those results by the specific catalysts and narratives that matter most to you, so you can identify the highest conviction ideas for your own watchlist.

Take Control of Your Investment Journey

If DuPont de Nemours or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Oil?

Some of the strongest future breakouts start flying before headlines catch them. New ideas get stale fast, so scan these under the radar opportunities while it matters and consider acting while the window is open.

- Spot resilient cash generators before momentum headlines catch up by running the list of solid balance sheet and fundamentals (11 results) and focus on businesses with room to absorb shocks without rushing to raise capital.

- Explore potential beneficiaries of AI infrastructure demand by checking the 49 AI infrastructure stocks and concentrate on companies supplying the picks and shovels behind growing compute and data needs.

- Review high quality miners before gold sentiment changes by scanning the 33 elite gold producer stocks and filter for producers with meaningful scale and cleaner looking balance sheets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.