MillerKnoll (MLKN) Stock Could Be 50.9% Undervalued After Design Days Refresh

MillerKnoll, Inc. MLKN | 0.00 |

MillerKnoll (MLKN) is back in the spotlight after using Fulton Market Design Days 2026 to showcase an extensive lineup of new and refreshed products, along with fresh creative leadership at Herman Miller.

For investors watching MillerKnoll, the recent design launches and leadership appointments come after a period where the share price return has been mixed, with a 30 day gain of 8.64% and a 90 day decline of 12.48%, while the 3 year total shareholder return of 22.11% contrasts with a 5 year total shareholder return that is down 60.32%. This combination suggests improving momentum in the near term alongside a still challenging longer term record.

If the design refresh at MillerKnoll has you thinking about where else change could reshape returns, it may be worth scanning 20 top founder-led companies

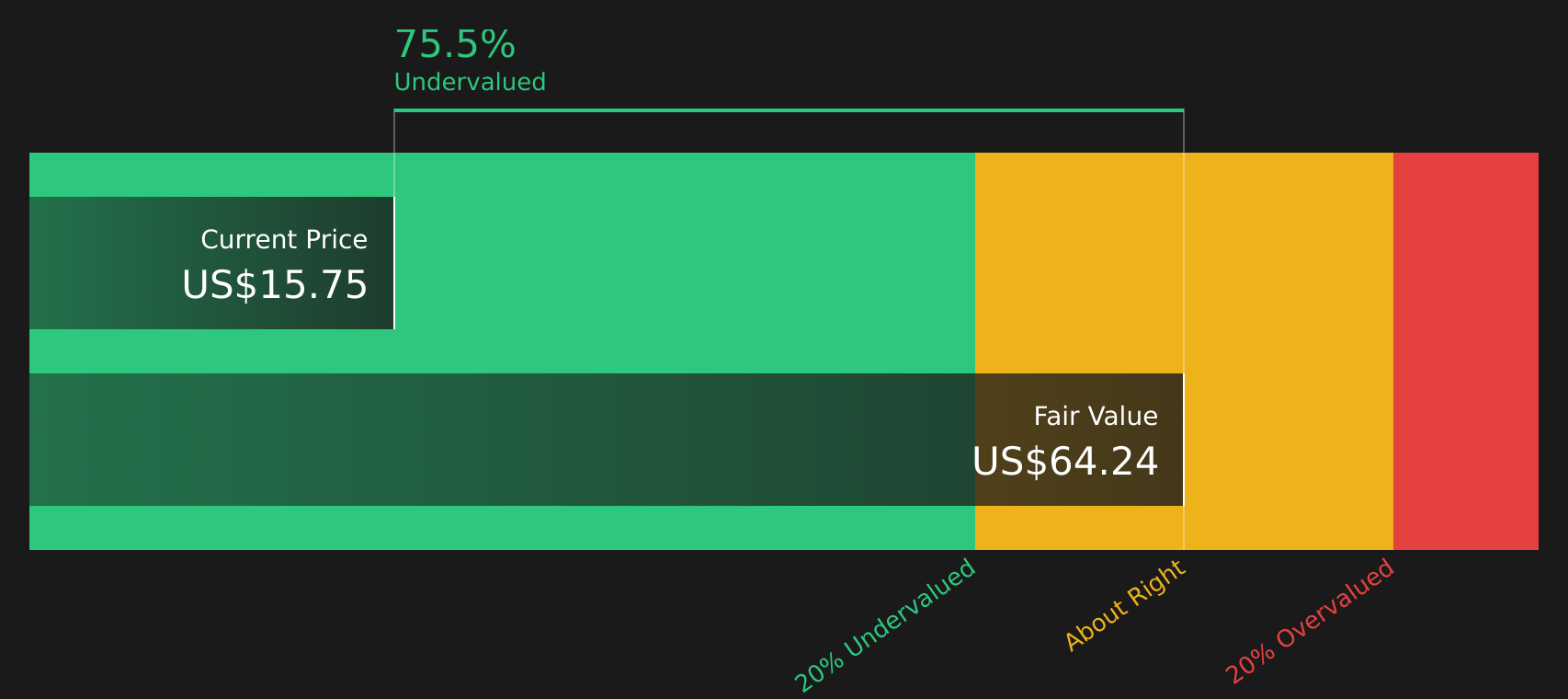

With MillerKnoll stock trading at $15.71 alongside an intrinsic value estimate that implies a sizeable gap, the key question is whether investors are looking at a genuine discount or if the market is already pricing in future growth.

Most Popular Narrative: 50.9% Undervalued

At a last close of $15.71 versus a widely followed fair value estimate of $32, the current MillerKnoll share price sits well below that narrative benchmark, putting extra focus on the earnings and margin assumptions that sit underneath.

The analysts have a consensus price target of $32.0 for MillerKnoll based on their expectations of its future earnings growth, profit margins and other risk factors.

In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $4.3 billion, earnings will come to $212.4 million, and it would be trading on a PE ratio of 13.9x, assuming you use a discount rate of 9.5%.

Want to see how a relatively modest revenue trajectory combines with much higher profit margins and a reset earnings multiple to reach that $32 fair value? The most followed narrative lays out a detailed earnings path, specific margin targets, and a valuation anchor that looks very different from today’s headline P/E.

Result: Fair Value of $32 (UNDERVALUED)

However, the MillerKnoll narrative still hinges on tariff and trade policy risks, along with weaker North America Contract orders that could pressure revenue and margins.

Another View on MillerKnoll Stock

The analyst narrative and SWS DCF model both point to MillerKnoll as undervalued, with the stock at $15.71 compared with an internal future cash flow value estimate of $64.13. That is a very wide gap, so the real question is how comfortable you are with the long term cash flow assumptions behind it.

Next Steps

With mixed signals around MillerKnoll's value and outlook, now is a good time to review the underlying data yourself and decide how comfortable you are with both the risks and potential rewards that investors are currently weighing. You can start with the 2 key rewards and 4 important warning signs.

Looking for more investment ideas beyond MillerKnoll?

If MillerKnoll has sharpened your focus on value and quality, this is the moment to widen your watchlist before the next wave of opportunities passes you by.

- Target resilient opportunities with lower volatility by reviewing 68 resilient stocks with low risk scores to help steady your portfolio when sentiment turns.

- Spot potential bargains early by scanning screener containing 20 high quality undiscovered gems before they attract wider market attention and pricing shifts.

- Strengthen your core holdings by using the solid balance sheet and fundamentals stocks screener (48 results) to focus on companies with sturdier financial foundations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.