Moelis (MC) Stock After 7.7% One-Year Gain Is The Price Still Reasonable

Moelis & Co. Class A MC | 0.00 |

- If you are wondering whether Moelis at around US$64.48 is priced fairly or not, the starting point is understanding what the current share price might already be factoring in.

- The stock is up 7.7% over the past year, even though it is down 3.7% over the last week, 4.2% over the last month, and 9.5% year to date. This suggests the market's view on risk and opportunity around Moelis has shifted over different time frames.

- Recent company updates and sector commentary have kept Moelis in focus, helping investors reassess how the stock fits into the broader capital markets space. These developments form an important backdrop when weighing whether the latest moves in the share price are justified by fundamentals or sentiment.

- On Simply Wall St’s valuation checks, Moelis currently has a valuation score of 3 out of 6. The rest of this article will walk through the key valuation approaches behind that score, before closing with a different way to think about what “fair value” can mean for this stock.

Approach 1: Moelis Excess Returns Analysis

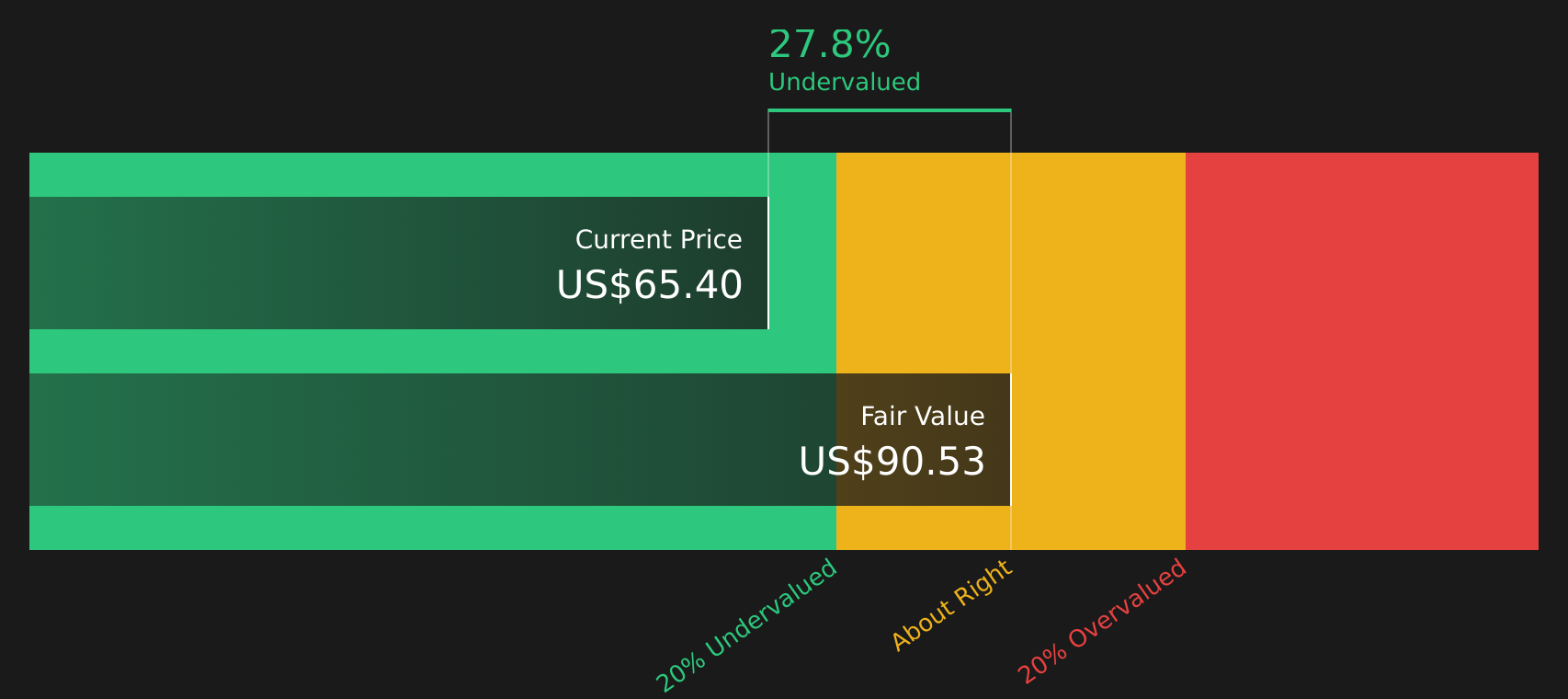

The Excess Returns model asks a simple question for Moelis: how much profit is the company expected to generate above the return that shareholders require, given the equity invested in the business.

For Moelis, estimated book value is $6.55 per share and average return on equity is 53.22%. That translates into a stable earnings figure of about $4.21 per share, based on weighted future Return on Equity estimates from 4 analysts. The model assumes a cost of equity of $0.62 per share, which leaves an estimated excess return of $3.60 per share. Stable book value is projected at $7.92 per share, also based on weighted future Book Value estimates from 4 analysts.

Combining these inputs, the Excess Returns framework produces an estimated intrinsic value of $92.01 per share. Compared with the current Moelis share price of about $64.48, this suggests the stock is 29.9% undervalued under this approach.

Result: UNDERVALUED

Our Excess Returns analysis suggests Moelis is undervalued by 29.9%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Approach 2: Moelis Price vs Earnings

For a profitable company like Moelis, the P/E ratio is a useful shorthand for how much you are paying for each dollar of earnings. It allows you to compare what the market is currently willing to pay for Moelis earnings with other stocks in the Capital Markets industry.

What counts as a “normal” or “fair” P/E ratio usually reflects how the market views a company’s growth potential and risk. Higher expected growth or lower perceived risk can support a higher P/E, while lower growth or higher risk often align with a lower multiple.

Moelis currently trades on a P/E of 21.68x. This sits close to the peer group average of 21.28x and below the broader Capital Markets industry average of 39.58x. Simply Wall St also calculates a proprietary “Fair Ratio” for Moelis of 15.06x. This is the P/E level suggested by factors such as earnings growth profile, industry, profit margins, market cap and company specific risks.

This Fair Ratio can be more informative than a simple comparison with peers or industry averages because it adjusts for Moelis specific characteristics rather than assuming all companies deserve the same multiple. Comparing 21.68x with the 15.06x Fair Ratio points to Moelis trading above this benchmark.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Moelis Narrative

Earlier the article mentioned that there is an even better way to think about Moelis than static multiples. This is where Narratives come in, allowing you to attach a clear story about future revenue, earnings and margins to your own fair value and then compare that to the current share price.

A Narrative on Simply Wall St is your view of how Moelis' business might develop, turned into a structured forecast that links the story you believe, the financial estimates you think are reasonable and the fair value that falls out of those assumptions.

Because Narratives sit inside the Community page on Simply Wall St, they are designed to be accessible. You can see how a more optimistic view that lines up with a Fair Value of US$86.00 differs from a cautious view closer to US$58.00, and use that range to decide whether the current price feels high, low or roughly in line with your expectations.

As new information arrives, such as Moelis' conference commentary, updated buyback activity or revised analyst targets, these Narratives can be refreshed so your decision framework stays current rather than frozen at the time you first ran the numbers.

For Moelis however we'll make it really easy for you with previews of two leading Moelis Narratives:

Fair value in this bullish narrative is US$71.00 per share.

At the last close of US$64.48, this implies Moelis trades about 9.2% below that fair value estimate.

This narrative uses a forecast revenue growth rate of 15.39%.

- Expansion into private capital advisory and technology sectors is expected to broaden Moelis' deal flow and client base, supporting revenue and earnings.

- Hiring senior bankers and increasing recurring advisory work is aimed at improving fee visibility and margins, while still accepting the risk of higher compensation costs.

- Analysts in this camp see fair value around US$71.00, with underlying assumptions about higher revenues, slightly higher margins and a P/E of 19.0x by 2029 compared to today.

Fair value in this more cautious narrative is US$58.00 per share.

At the last close of US$64.48, this implies Moelis trades about 11.2% above that fair value estimate.

This narrative uses a forecast revenue growth rate of 15.03%.

- Growing use of AI, automation and direct capital access is expected to put pressure on Moelis' traditional advisory fees and add to revenue volatility over time.

- Dependence on transaction based revenues, rising regulatory complexity and competition are central to concerns around margins and earnings stability.

- Analysts behind this narrative anchor on a fair value of US$58.00, tied to assumptions of strong earnings by 2029 but a much lower P/E of 11.2x than today given perceived risks.

These contrasting Moelis Narratives give you a structured way to decide which assumptions about revenue growth, margins and valuation feel closer to your own view, and where the current share price sits relative to that range.

Do you think there's more to the story for Moelis? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.