Monster Beverage Stock And Two Low Debt Quiet Compounders

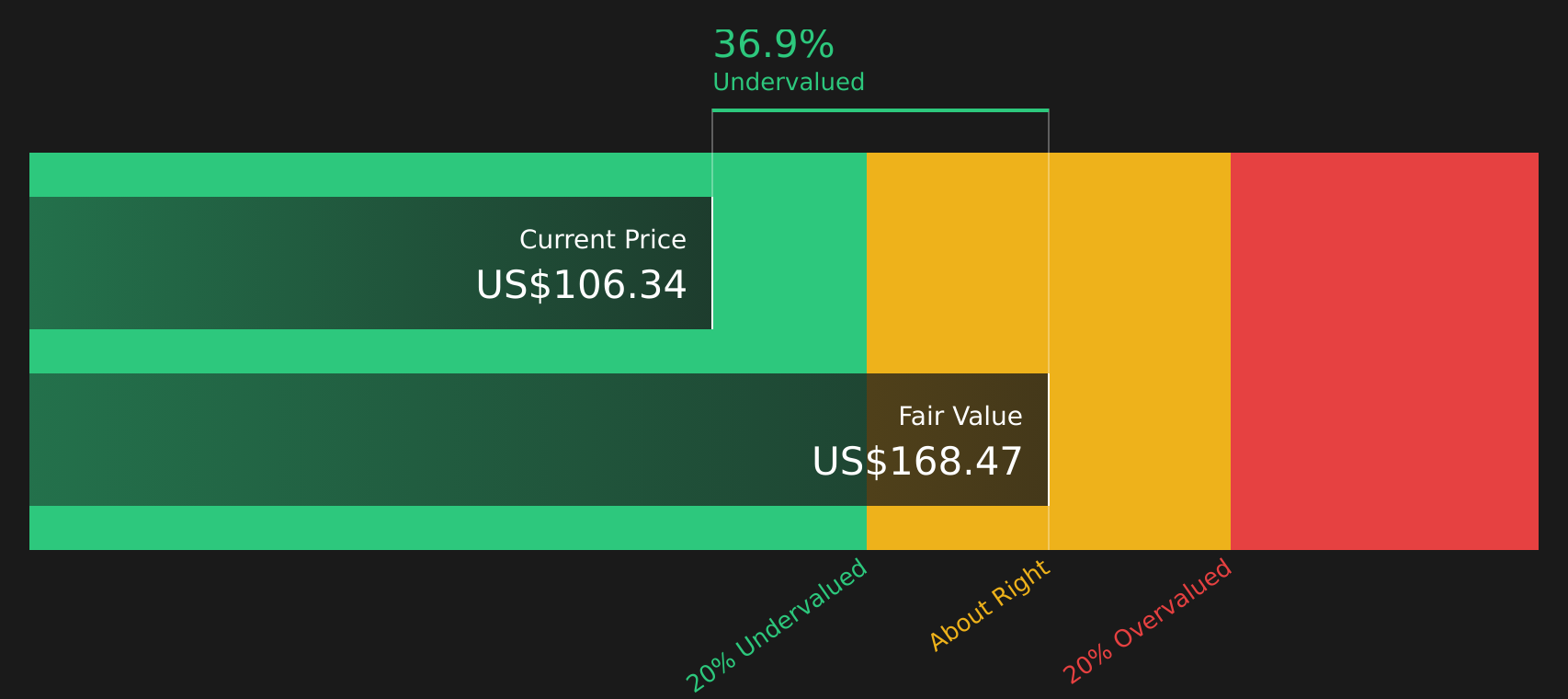

T. Rowe Price Group, Inc. TROW | 0.00 |

With the Federal Reserve signaling an interest rate hike and borrowing costs set to rise, many investors are rethinking which stocks might hold up best if financing becomes more expensive and market swings increase. This article focuses on low debt companies that appear well prepared for this kind of backdrop, thanks to limited reliance on borrowing and stronger balance sheet metrics. From this screener, three stocks will be highlighted that look particularly interesting based on their financial profiles and their exposure to the current interest rate story. This may help you decide which opportunities might deserve a closer look and which to treat with more caution.

Monster Beverage (MNST)

Overview: Monster Beverage is a global drinks company that develops, markets, and sells a wide range of energy drinks and other ready to drink beverages under brands like Monster Energy, Reign, Bang, Java Monster, and several alcohol and craft beer labels, distributing through major retailers, bottlers, and e commerce channels.

Operations: Monster Beverage generates most of its revenue from Monster Energy Drinks at about US$8.1b, with smaller contributions from Strategic Brands of roughly US$0.5b, Alcohol Brands of about US$0.1b, and Other at around US$24m. Geographically, the U.S. and Canada contribute about US$5.3b of sales, with the rest spread across Latin America, EMEA, and Asia Pacific.

Market Cap: US$90.9b

Monster Beverage gives you a low debt balance sheet with strong cash, direct exposure to the energy drinks category, and a track record of high profitability, including a 23.3% ROE and net profit margins of 23.1%. Analysts point to opportunities in zero sugar and international products. Recent Q1 2026 results showed net sales of US$2.35b and ongoing margin focus, while management is also returning capital through buybacks. The trade off is that Monster Beverage stock trades on a rich 44.1x P/E, and recent insider selling raises questions about how much optimism is already priced in, especially with earnings growth forecasts below broader US market expectations and cost pressures such as aluminum tariffs on the radar.

Monster Beverage’s rich 44.1x P/E and high profitability suggest investors may be missing how finely balanced the risk and reward story really is, and the 2 key rewards and 1 important warning sign could reveal what is quietly tipping the scales

Copart (CPRT)

Overview: Copart runs a global online auction platform that helps insurance companies, car dealers, and the public sell and buy damaged, salvaged, and used vehicles, combining digital bidding with its own storage yards and title processing services to turn totaled cars into cash.

Operations: Copart generates about US$4.64b of revenue from vehicle related services to gasoline and auto dealers, with roughly US$3.80b from the United States and US$0.84b from international markets.

Market Cap: US$28.5b

Copart stands out in a higher rate world because it runs an asset light, fee based marketplace with minimal leverage and strong cash generation, so rising borrowing costs are less of a headwind than for many capital heavy businesses. The company has been growing through international markets and non insurance sellers, which has helped offset softer U.S. insurance volumes, and its 33.5% net margins point to a powerful business model. At the same time, earnings and revenue forecasts are modest and higher auto insurance costs have already pressured collision coverage and damaged vehicle supply, so future growth is not risk free. The real interest is how this balance of resilience, valuation signals, and supply risks fits the low debt theme and what that might mean for long term investors.

Copart’s fee based model and high 33.5% net margins look powerful, but the real question is how that story stacks up once you see the full valuation, growth, and supply picture in the analysis report for Copart.

T. Rowe Price Group (TROW)

Overview: T. Rowe Price Group is a global investment manager that runs mutual funds, ETFs, and other vehicles for individuals, retirement plans, and institutions, using in house and external research to pick stocks and bonds across markets, including strategies that factor in environmental, social, and governance issues.

Operations: T. Rowe Price Group generates about US$7.4b in revenue from Investment Management Services.

Market Cap: US$23.3b

T. Rowe Price Group stands out in a higher rate world because it carries no debt, yet still supports a 4.81% dividend and 27.6% profit margins, while trading at an earnings multiple that is below many peers and some fair value estimates. The interest rate backdrop and recent volatility matter because T. Rowe Price lives off assets under management and investor confidence. It is leaning into retirement products, ETFs, private credit, and partnerships such as ICE Compass and IncomeSelect that could broaden its client base and fee mix. At the same time, pressure from low fee passive products, fee compression, and past earnings declines mean this is not a simple yield story. The key consideration is how that mix of value, income, and competitive risk compares for long term investors.

T. Rowe Price Group’s mix of no debt, 4.81% dividend income, and 27.6% margins hints at a story many investors may be only half seeing, and the analyst forecasts for T. Rowe Price Group could show what might be quietly building beneath the surface

The three low debt stocks in this article are just a starting point, and the full screener uncovered 379 more companies in the Low Debt Companies screener that share similarly conservative balance sheets and potentially compelling narratives. Use Simply Wall St to identify, analyze, and filter for the specific catalysts and stories that matter most so you can focus on the highest conviction opportunities in minutes instead of hours.

Take Control of Your Investment Journey

If Monster Beverage or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Others?

Some of the most interesting stories can move from quiet to front page quickly. By the time headlines hit, the ideal entry can be gone, so consider acting promptly.

- Focus on income opportunities that aim for staying power with a curated set of potential high yield payers in the 8 dividend fortresses.

- Track real economy momentum by scanning producers in the 8 top copper producer stocks before demand stories are fully priced in and sentiment shifts.

- Identify potential future automation leaders early by reviewing companies in the 31 robotics and automation stocks while many remain under the radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.