Moody's (MCO) Stock Looks Fully Priced On Fair Value And Earnings

Moody's Corporation MCO | 0.00 |

Moody's stock has delivered a 43.8% gain over the past three years, yet the current valuation checks suggest the shares trade at a premium, with both the intrinsic value estimate from the Excess Returns model and market multiples pointing to the stock being overvalued.

- Over the last 3 years Moody's has returned 43.8%, which puts recent price strength against a more cautious read from the valuation models.

- The push to expand beyond traditional credit ratings into analytics and workflow tools can support longer term earnings quality, while any slowdown in private credit fundraising, especially in Asia Pacific, may limit how much investors are willing to pay for that growth story.

- With a value score of 1 out of 6, Moody's currently leans expensive on the broader set of valuation checks rather than screening as a clear bargain.

The issue now is whether Moody's current share price already reflects the long term benefits of its business shift, or if there is still room for the valuation to catch up with fundamentals.

Has Moody's Run Too Far on Excess Returns?

The Excess Returns model for Moody's looks at how much profit the company is projected to earn on its equity base above the required return that shareholders might expect. For Moody's, this framework points to a business generating returns on equity that are substantially higher than its estimated cost of equity.

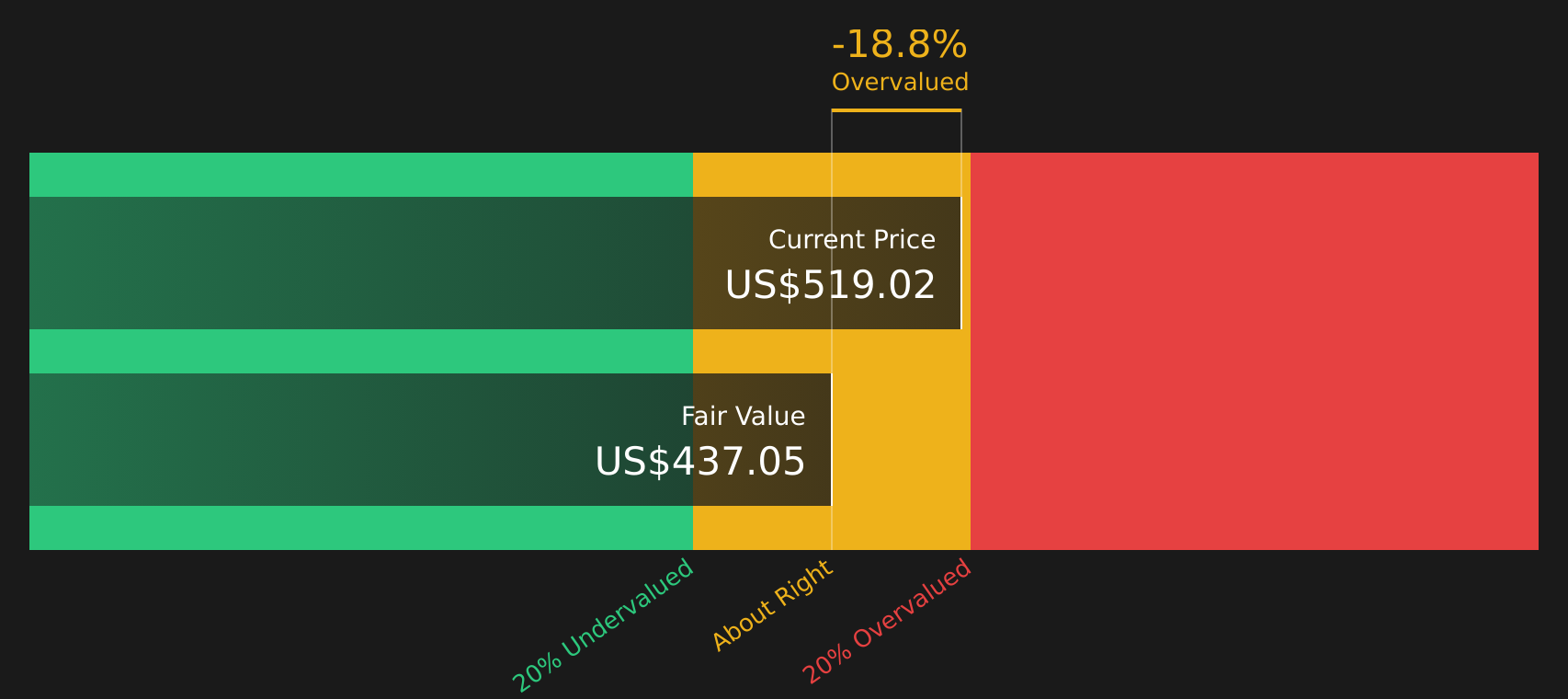

The inputs behind the model highlight why the stock scores as expensive. Book Value is $17.14 per share and Stable EPS is $20.22 per share, based on return on equity estimates from 7 analysts, against a Cost of Equity of $2.08 per share. That gap feeds into an Excess Return of $18.14 per share and an Average Return on Equity of 77.23%, supported by a Stable Book Value estimate of $26.18 per share from 5 analysts. These economics translate into an intrinsic value of $438.63 per share, which sits about 15.0% below the current share price, so the model points to Moody's stock as overvalued on this basis.

Because Moody's recently reported record growth as it expands beyond credit ratings into broader analytics and workflow tools, the market appears willing to pay a premium above what the Excess Returns math implies.

On the Excess Returns model, Moody's screens as overvalued, with the market price running ahead of the model's intrinsic value estimate.

Our Excess Returns analysis suggests Moody's may be overvalued by 15.0%. Discover 47 high quality undervalued stocks or create your own screener to find better value opportunities.

Is Moody's Getting Expensive on Earnings?

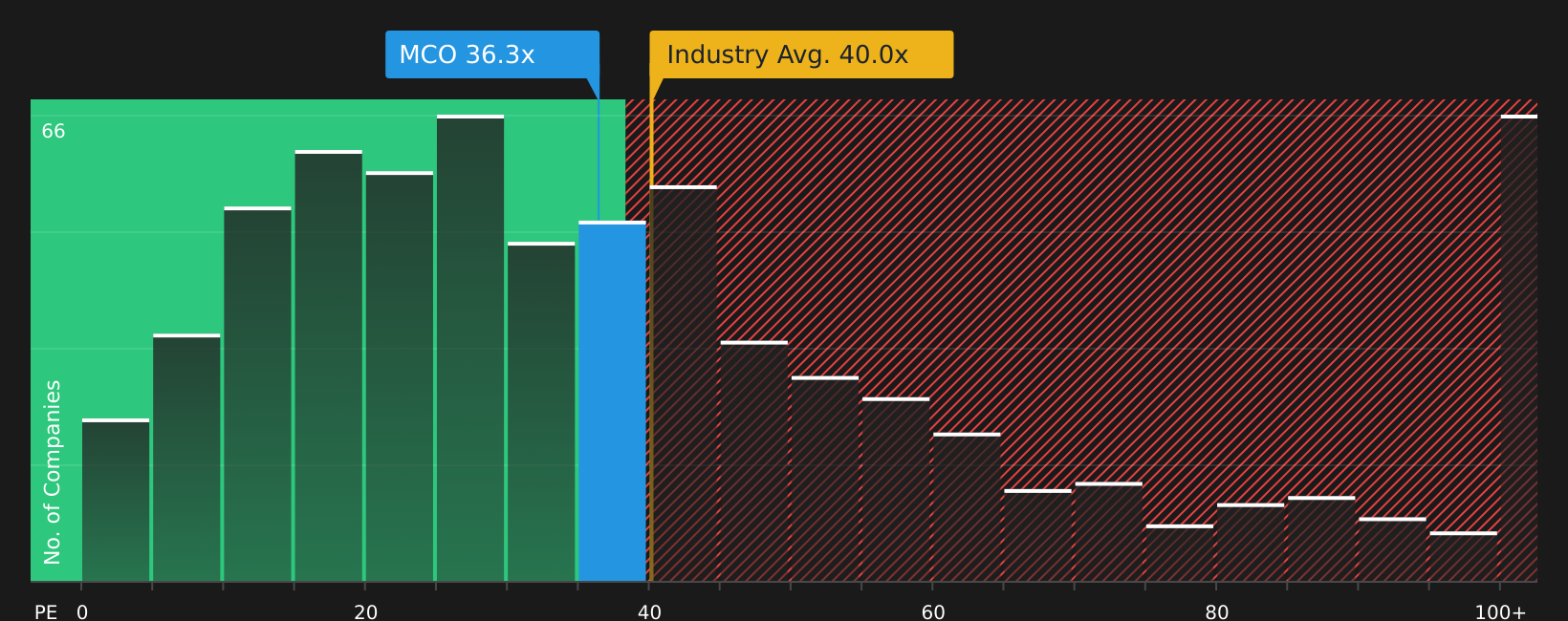

The P/E ratio suits Moody's because earnings are a key lens for a mature, high margin information services and credit ratings business. On this measure, Moody's trades on about 35.3x earnings, which is below the Capital Markets industry average of roughly 40.0x but above the peer group average of about 23.9x.

A tailored fair P/E ratio for Moody's, which reflects its size, margins and risk profile, sits closer to 18.1x. That is roughly half the current P/E, suggesting investors are paying a substantial premium versus what this framework implies for the stock. The current multiple already reflects a strong earnings profile and leaves less room for disappointment.

On the P/E multiple, Moody's stock currently appears overvalued, with the market price implying a much richer earnings premium than the fair ratio suggests.

The Moody's Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Moody's pick up where the valuation checks leave off by spelling out what kind of future for growth, margins and earnings would need to play out for the stock to be worth significantly more or less than it is today on the market. Each narrative anchors its number to a specific view on how Moody's growth, profitability and risk profile might evolve, giving you a reference point you can revisit as new information comes through.

Community views on Moody's sit far apart, with some investors seeing a wide moat at a reasonable price while others focus on premium pricing risks.

Bull case: 9% undervalued

"Moody's has established itself as one of the global standards in credit ratings, a status reflected in its wide economic moat and consequently stellar operating margins in the 45 to 50% range..."

Bear case: 7% overvalued

"At current valuations, Moody’s is not a bargain-bin stock, but high-quality compounding businesses rarely are..."

Do you think there's more to the story for Moody's? Head over to our Community to see what others are saying!

The Bottom Line

For Moody's, both the Excess Returns intrinsic value estimate and the earnings multiple view currently point to the stock as overvalued, suggesting expectations are already demanding. The broader valuation checks are also weak, so the burden of proof now sits with the business to keep justifying a premium price tag as it leans further into analytics and workflow tools. The crux for investors is whether Moody's can sustain the kind of earnings quality and growth narrative that keeps the current valuation intact, or whether a shift in sentiment or fundraising trends would pressure the multiple from here.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.