Murphy USA (MUSA) On A Fair Value Debate As Growth Expectations Stay In Focus

Murphy USA, Inc. MUSA | 0.00 |

Recent share performance and business snapshot

Murphy USA (MUSA) has drawn attention after recent share moves, with the stock up around 4% over the past month and about 6.6% over the past 3 months, prompting a closer look at its fundamentals.

At a latest share price of US$526.33, Murphy USA has seen short term share price momentum soften after a 7 day share price return decline of 4.5%. Its year to date share price return of 29.9% and 5 year total shareholder return of 300.4% reflect a strong longer term track record.

If this type of performance has you thinking about where else growth stories might emerge, it could be worth scanning 20 top founder-led companies

With Murphy USA shares already posting solid multi year returns and trading around US$526, the key question now is simple: are you looking at an undervalued retailer or a stock where the market is already banking on future growth?

Most Popular Narrative: 6% Undervalued

On the most followed narrative, Murphy USA’s fair value of $558 sits modestly above the latest close of $526.33, setting up a measured valuation debate.

The analysts have a consensus price target of $558.0 for Murphy USA based on their expectations of its future earnings growth, profit margins and other risk factors.

Given the current share price of $542.74, the analyst price target of $558.0 is 2.7% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

Curious what underpins that fair value call? The narrative leans on steady top line expansion, slimmer margins, and a richer future earnings multiple to balance the equation.

Result: Fair Value of $558 (UNDERVALUED)

However, the Murphy USA narrative can quickly look different if fuel demand keeps softening or new store openings fall short of expectations, which could pressure margins and cash returns.

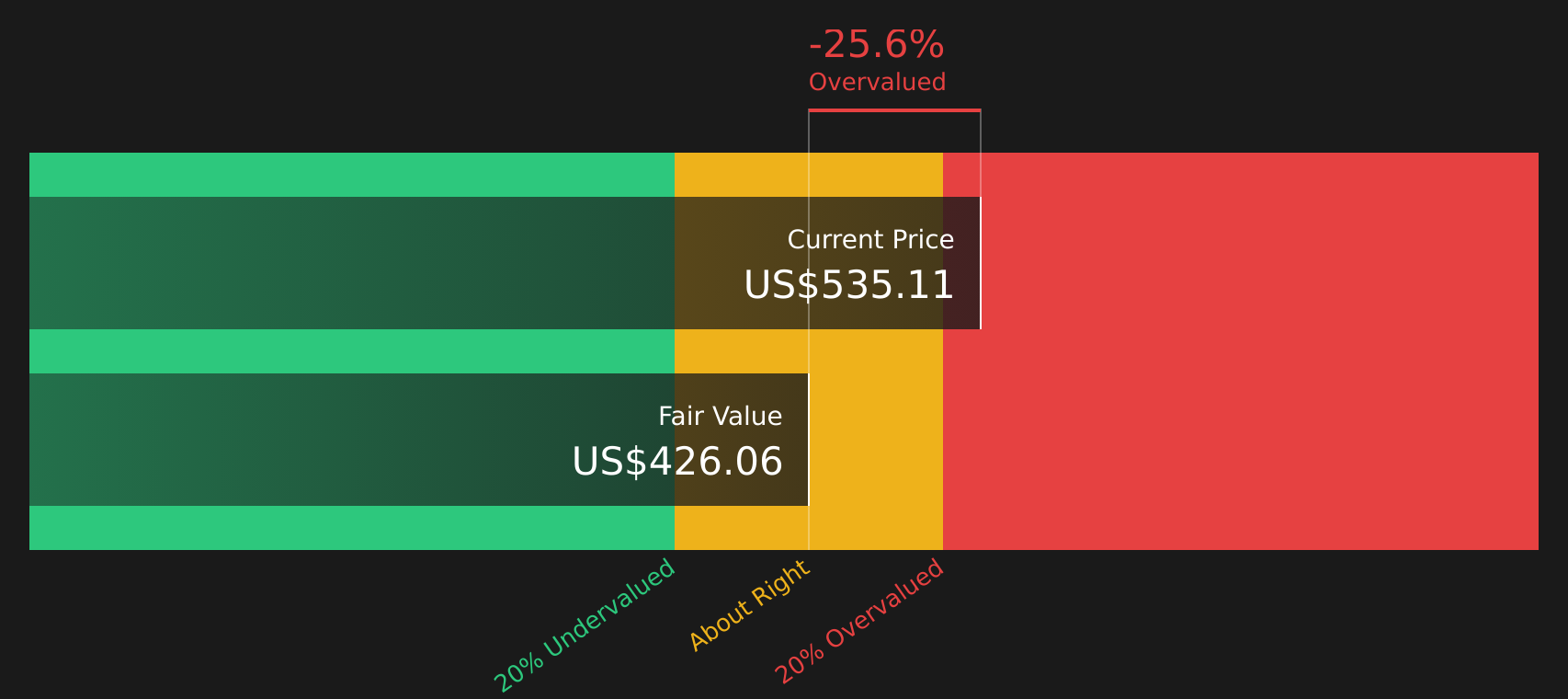

Another view on Murphy USA’s valuation

The analyst narrative frames Murphy USA as around 6% undervalued at a fair value of $558, but the SWS DCF model tells a different story. On that approach, the stock at $526.33 sits above an estimated future cash flow value of $426.05, which points to a potential overvaluation instead.

For investors, that gap between the analyst target and our DCF output raises a simple question: which set of assumptions around growth, margins and required returns feels closer to your own view of Murphy USA’s future cash generation?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Murphy USA for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment on Murphy USA split between opportunity and caution, it makes sense to move quickly, review the key data for yourself, and weigh both sides of the story by checking the 2 key rewards and 3 important warning signs

Looking for more investment ideas beyond Murphy USA?

If Murphy USA has sharpened your appetite for opportunities, do not stop here. The Simply Wall St Screener can surface other stocks that match your investing style.

- Target resilient cash generators by reviewing companies in the solid balance sheet and fundamentals stocks screener (48 results) that may better align with your risk comfort.

- Spot potential mispricings by scanning the 44 high quality undervalued stocks and see which stocks currently sit out of favor with the market.

- Explore potential income ideas by checking the 8 dividend fortresses before others move first.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.