NCR Atleos (NATL) Could Be 11% Undervalued As Shell UK Deal And Index Entry Draw Focus

NCR Atleos Corporation NATL | 0.00 |

NCR Atleos (NATL) is in focus after expanding its long-running ATM partnership with Shell UK and securing inclusion in multiple Russell 2000 indices. These developments may influence how investors view the stock.

Recent client wins and index inclusions appear to be reflected in NCR Atleos’ share price momentum, with a year to date share price return of 19.72% and a 1 year total shareholder return of 51.03% from a last close of US$44.57. Overall, this suggests interest in the stock has been building rather than fading.

If you are looking for other opportunities in financial technology and infrastructure, it could be worth checking a curated screener of 20 top founder-led companies

With NCR Atleos now in key Russell indices, fresh client collaborations and annual revenue growth of 3.92% alongside net income growth of 36.26%, the question is whether the recent share price strength leaves a buying opportunity or reflects markets already pricing in future growth.

Most Popular Narrative: 11.3% Undervalued

With NCR Atleos trading at $44.57 against a narrative fair value of $50.27, the most followed storyline in the market sees upside still on the table and ties that view directly to how its ATM as a Service model scales.

The rapid growth and backlog in NCR Atleos' ATM-as-a-Service business (32% revenue growth in Q2, 105% YoY backlog increase) signals accelerating demand for outsourced, integrated cash management as banks digitize and automate cash operations, setting up recurring, high-margin revenue growth into 2026 and beyond.

Want to see what is baked into that fair value for NCR Atleos? Earnings power, margins and the multiple all shift meaningfully in this narrative. The full story joins those moving parts into one valuation roadmap.

Result: Fair Value of $50.27 (UNDERVALUED)

However, the bullish NCR Atleos narrative could be challenged if consumers move faster toward fully digital banking or if fintech competition squeezes ATM service margins and contract wins.

Another Take On NCR Atleos Valuation

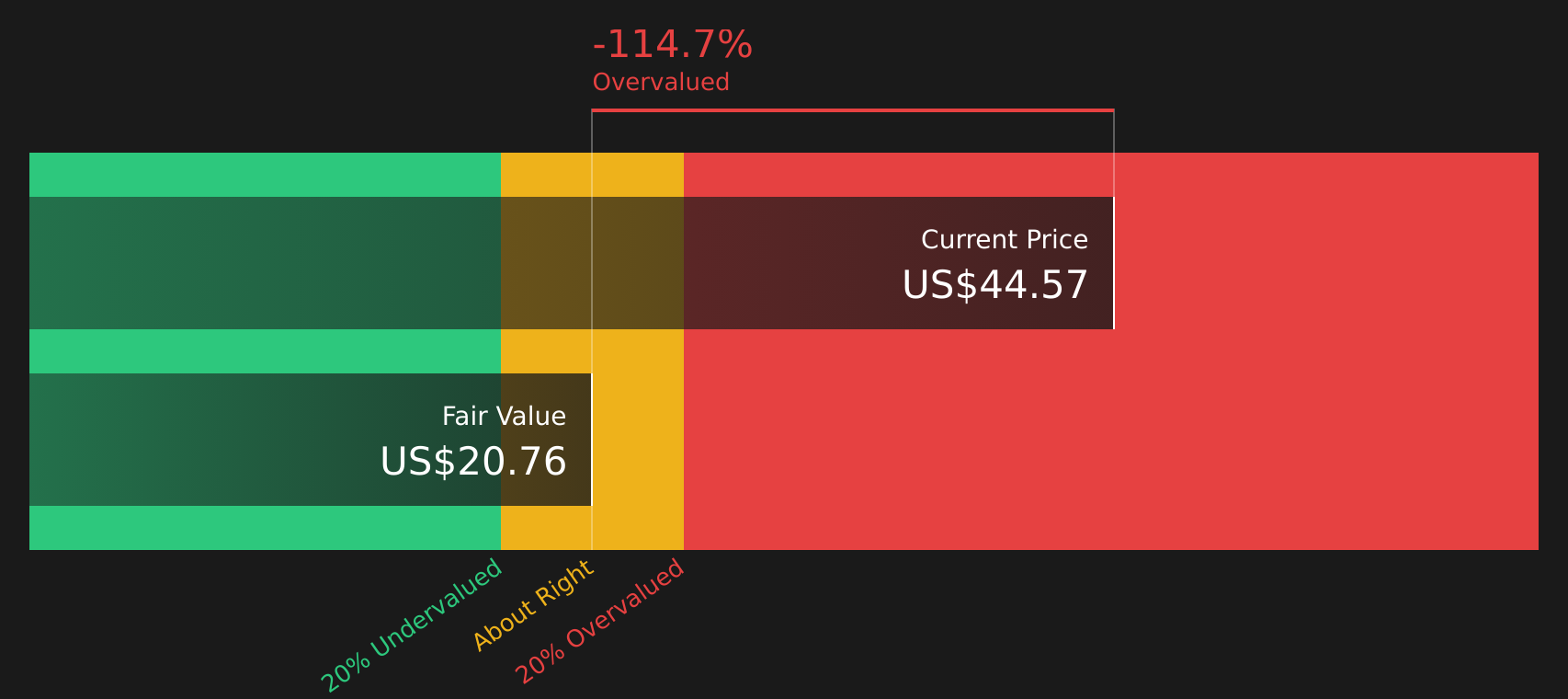

The first fair value view relies on analyst earnings forecasts and a P/E of 8.7x in 2029. Our DCF model presents a different perspective, with an estimated future cash flow value of $20.76 compared with the current $44.57 share price, which screens as overvalued on that basis. Which lens do you trust more?

For a closer look at how this cash flow view is built, including the key assumptions the model uses, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NCR Atleos for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around NCR Atleos have you on the fence, now is a good time to review the data yourself and decide where you stand. You can start with 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond NCR Atleos?

If NCR Atleos has sharpened your interest, do not stop here. Use the Simply Wall Street Screener to quickly spot other stocks that might fit your style.

- Zero in on potential mispriced opportunities by scanning 44 high quality undervalued stocks that combine solid fundamentals with attractive valuations.

- Build a steadier portfolio base by checking 74 resilient stocks with low risk scores that score well on resilience and financial strength.

- Get ahead of the crowd by reviewing the screener containing 18 high quality undiscovered gems that meet strict quality filters before they gain wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.