Nelnet (NNI) Looks Fully Priced After Graduate Loan Expansion

Nelnet, Inc. Class A NNI | 0.00 |

Nelnet (NNI) is drawing fresh attention after Nelnet Bank expanded its graduate student loan offerings ahead of the planned phaseout of federal Grad PLUS loans for new borrowers starting July 1, 2026.

Recent headlines around graduate lending come as Nelnet’s 1 month share price return of 4.7% and year to date share price return of 4.9% sit alongside a 1 year total shareholder return of 11.6% and a 5 year total shareholder return just under 2x. Together, these figures point to steady but not explosive momentum around the story.

If you are weighing Nelnet’s position in your portfolio, it can also be helpful to scan for other financials and lenders using the Simply Wall St tool that highlights 20 top founder-led companies

With Nelnet trading close to analyst price expectations and a value score of 1, the headline numbers suggest limited mispricing. However, could the Grad PLUS shake-up mean there is still a buying opportunity, or is future growth already reflected in the price?

Price-to-Earnings of 11.7x: Is it justified?

On a P/E of 11.7x, Nelnet trades at a lower earnings multiple than the wider US market but at a premium to the US Consumer Finance industry, which raises questions about how its mix of businesses and earnings quality are being weighed by investors.

The P/E ratio compares the current share price to earnings per share and is a common way for investors to gauge how much they are paying for each dollar of profit. For Nelnet, a 11.7x multiple sits below the US market average P/E of 19.1x, but above the Consumer Finance industry average of 8.8x. This suggests the stock is being treated as better quality than the typical lender, without being priced as expensively as the broader market.

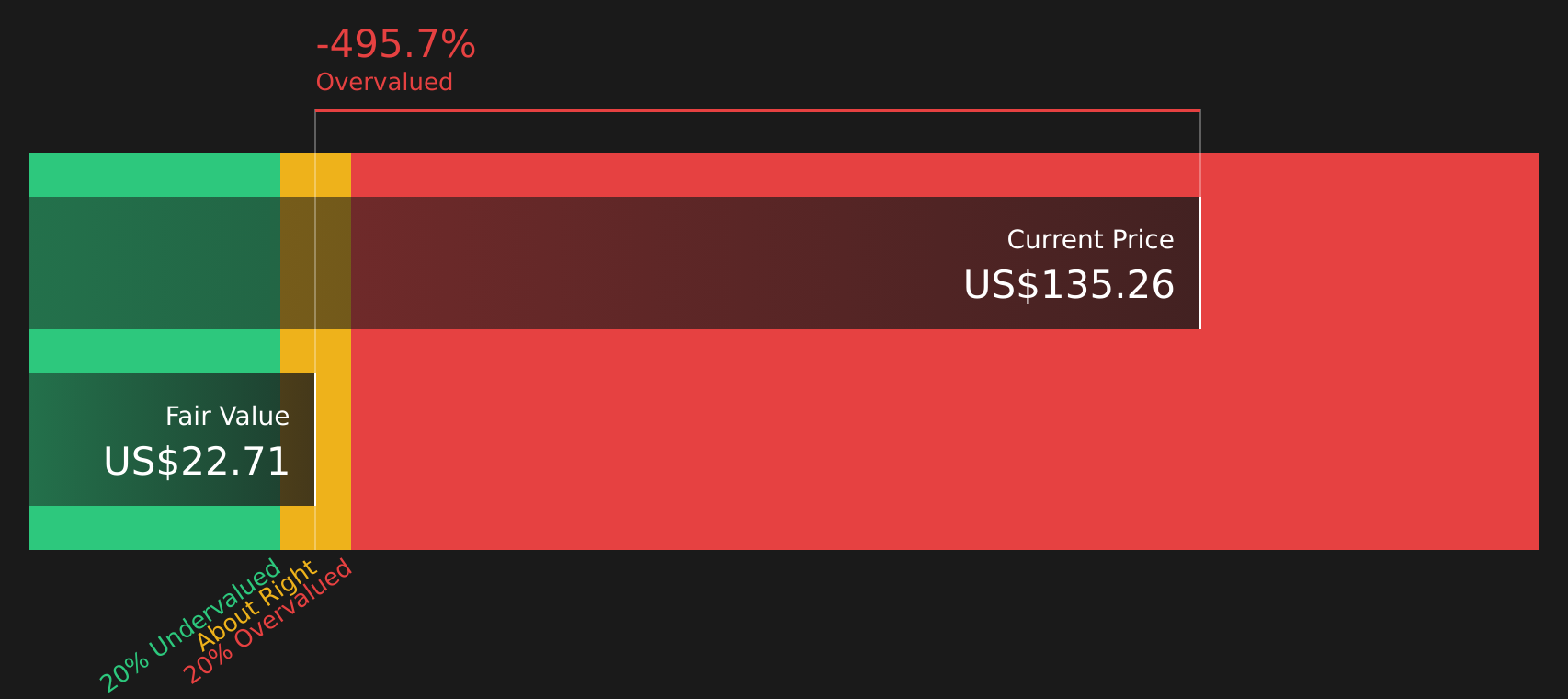

Part of that premium to industry could be tied to the company’s recent earnings rebound, with earnings reported as having grown very strongly over the past year after a multi year period in which they declined on average. At the same time, the SWS DCF model points to a very conservative view of future cash flows. It indicates that the current $135.26 share price is far above that specific fair value estimate of $22.44, so investors following that model may see limited room for error in the current valuation.

Against peers, the contrast is stark. Nelnet’s 11.7x P/E is higher than the 8.8x sector average, which means the stock is priced more richly than many Consumer Finance stocks, even though the same model flags that it is expensive compared to an intrinsic cash flow estimate. Without a fair ratio benchmark to indicate where the P/E could reasonably settle, the market’s stance appears to sit somewhere between treating Nelnet as a higher quality earner than most of its industry and potentially overpaying relative to its estimated future cash generation.

Result: Price-to-Earnings of 11.7x (OVERVALUED)

However, Nelnet’s premium to Consumer Finance peers and the large gap between its share price and one DCF estimate mean that sentiment could reverse quickly if earnings or Grad PLUS expectations disappoint.

Another View on Nelnet’s Value

The earlier discussion flagged Nelnet as expensive on a P/E of 11.7x compared with the Consumer Finance industry at 8.8x. Our DCF model tells a different story again, with the SWS DCF model suggesting a fair value of $22.44 versus today’s $135.26 share price, pointing to a very stretched valuation. So which signal should carry more weight when you think about risk?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Nelnet for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 42 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals around Nelnet’s valuation and future Grad PLUS exposure, it makes sense to review the underlying data yourself and act promptly. To weigh the upside potential against the concerns that investors have flagged, check out the 2 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Nelnet?

If Nelnet has you thinking harder about where to put fresh capital, do not stop here. Use focused stock lists to quickly spot other opportunities that fit your style.

- Target resilience by scanning stocks that pass strict balance sheet and fundamentals filters using the solid balance sheet and fundamentals stocks screener (46 results).

- Hunt for quality at a discount with the 42 high quality undervalued stocks that highlights companies combining sturdy finances with appealing valuations.

- Prioritise stability and income by checking out the 7 dividend fortresses that focuses on higher yielding companies with stronger profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.