NextEra Energy (NEE) Stock Looks Stretched After A 31% Five Year Return

NextEra Energy, Inc. NEE | 0.00 |

NextEra Energy stock sits at an interesting valuation crossroads, with a solid 5 year return against a low overall value score and two key pricing frameworks pulling in opposite directions as the Dividend Discount Model points to a premium to intrinsic value while market multiples suggest the shares look cheaper than peers. That split is now front and center for investors weighing how to price the company after a run of news including the planned Dominion Energy acquisition and heavy investment in clean power and grid assets.

- Over the past 5 years, NextEra Energy has returned 30.8%, which puts extra focus on whether today's valuation still leaves enough room for further upside.

- The planned all stock purchase of Dominion Energy can support higher long term earnings expectations. However, regulatory scrutiny around the deal and governance issues such as the recent political interference settlement may cap how much investors are willing to pay for that growth.

- NextEra Energy scores 2 of 6 on valuation checks, which leans expensive overall rather than a clear bargain despite the more supportive read from some multiples.

The issue now is whether the current share price already reflects the intrinsic value implied by NextEra Energy's dividend profile and growth plans, or if the market multiple view is closer to the mark.

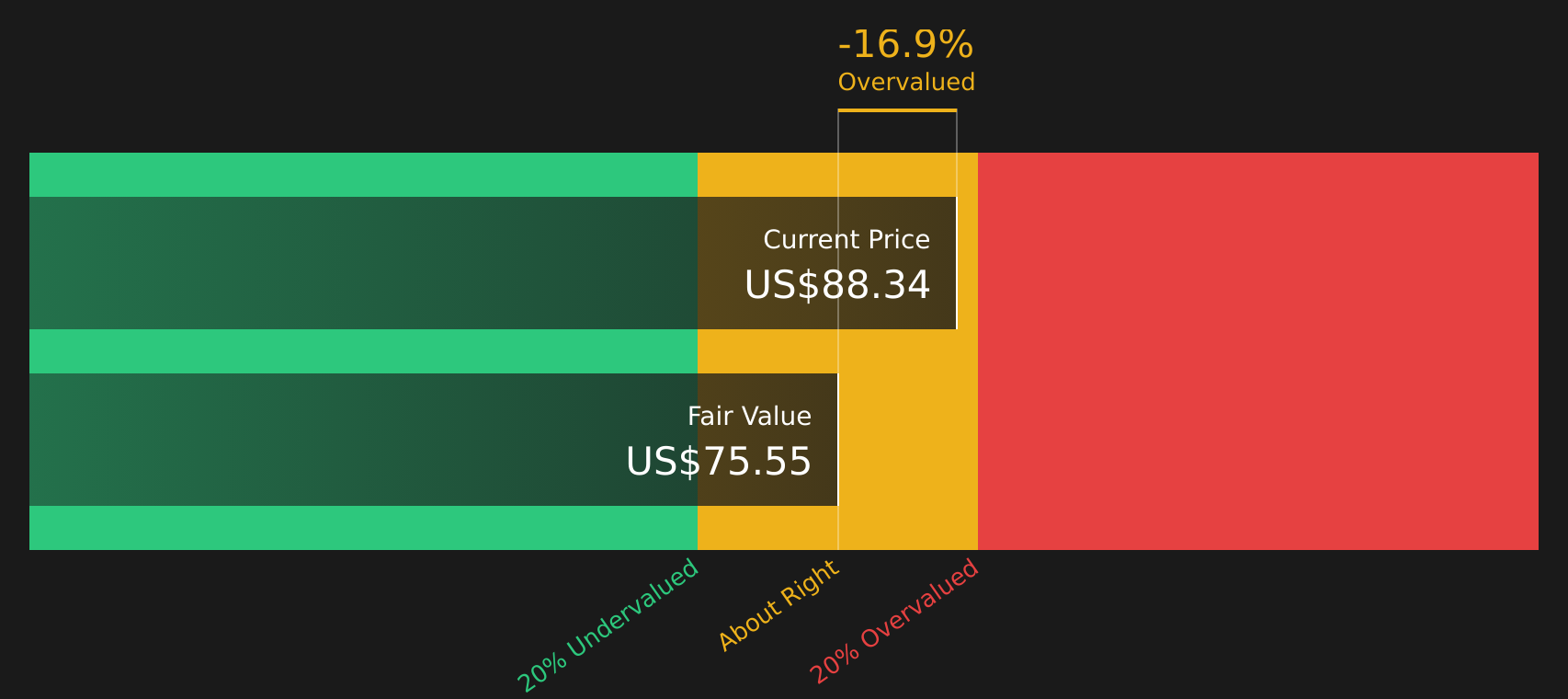

Does NextEra Energy Look Pricey on Dividends?

The Dividend Discount Model values NextEra Energy by projecting future dividends and the rate at which those payouts may grow over time. It is most useful when a company has an established dividend track record and a reasonably consistent policy.

For NextEra Energy, the DDM uses an annual dividend per share of about $2.70, a return on equity of roughly 9.9% and a payout ratio near 59%, with long term dividend growth capped at 3.54%. Based on these inputs, the model arrives at an intrinsic value of about $75.55 per share. This figure is below the current share price and indicates the stock screens as about 14.3% overvalued on a dividend basis.

The acquisition agreement to buy Dominion Energy, along with the large clean energy and grid investment pipeline, helps explain why investors may be comfortable paying more than the DDM output for NextEra Energy today. The model only captures dividend growth rather than the full range of potential cash flow from these projects.

Taken together, the Dividend Discount Model suggests NextEra Energy currently appears overvalued relative to its projected dividend stream.

Our Dividend Discount Model (DDM) analysis suggests NextEra Energy may be overvalued by 14.3%. Discover 41 high quality undervalued stocks or create your own screener to find better value opportunities.

Is NextEra Energy a Bargain on Earnings?

The P/E ratio is a useful yardstick for NextEra Energy because earnings remain a core driver of how investors value regulated utilities and large clean energy platforms. NextEra Energy currently trades on about 22.0x earnings, which sits close to both its peer average of 21.6x and the broader Electric Utilities industry average of 22.4x.

Where things get interesting is the comparison with the tailored fair P/E of 26.0x. This reflects what investors might typically pay given NextEra Energy's size, profitability and risk profile. Against that yardstick, the current multiple is lower. This suggests the stock trades at a discount relative to what these fundamentals would imply rather than at a premium to its sector.

On this P/E framework, NextEra Energy stock appears undervalued compared with the fair multiple implied by its earnings profile.

The NextEra Energy Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where this valuation split for NextEra Energy leaves off by spelling out which paths for growth, margins and earnings would need to play out for the stock to be worth materially more or less than its current price. They sit on the company's Community page. Each Narrative links a fair value estimate to a specific scenario for NextEra Energy's potential catalysts and risks, so you can track which version of events is taking shape over time.

Community views on NextEra Energy sit far apart, with one side leaning into long term demand and the other fixated on policy, cost and merger risk.

Bull case: 12% undervalued

"Accelerating and sustained demand growth for electricity, driven by AI, data center expansion, and electrification of sectors like transportation and heating, positions NextEra to grow volumes and capture higher average revenue per MWh as utilities compete to provide essential infrastructure for hyperscalers and traditional customers…"

Bear case: 18% overvalued

"The phase-out of wind and solar tax credits under the One Big Beautiful Bill Act will significantly reduce the financial incentives underpinning much of NextEra's renewables pipeline after 2029, leading to lower project returns and putting long-term earnings growth at risk as tax equity structures become less attractive and margins compress…"

Do you think there's more to the story for NextEra Energy? Head over to our Community to see what others are saying!

The Bottom Line

NextEra Energy sits between an intrinsic value view that screens as overvalued on the Dividend Discount Model (DDM) and a market multiple view that points to an undervalued P/E versus its tailored fair ratio. That gap reflects how heavily the DDM leans on near term funding needs and dividend capacity, while the multiple view leans on what investors expect from long run earnings and sentiment around peers. With broader valuation checks still weak, the key question is whether the current discount on earnings reflects a genuine opportunity or a market judgment on policy, regulatory and execution risk around its growth plans and the Dominion Energy deal.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.