Northern Trust (NTRS) Joins Russell Growth Indices, Is It Fully Valued?

Northern Trust Corporation NTRS | 0.00 |

Index additions put Northern Trust in focus

Northern Trust (NTRS) has just been added to several Russell growth indices, a shift that can influence how index tracking funds and benchmark aware investors look at the stock.

The recent index additions come after a strong run in Northern Trust’s share price, with a 27.63% 90 day share price return and 24.83% year to date share price return, while the 3 year total shareholder return of 156.65% points to momentum that has been building over time.

If you are looking beyond Northern Trust and want to spot other potential long term compounders, now could be an interesting moment to check out 20 top founder-led companies

With Northern Trust trading around US$173.87 and only a small intrinsic value gap of roughly 3%, the main question is whether recent growth and index additions leave meaningful upside, or if the market is already pricing in future progress.

Most Popular Narrative: 2% Overvalued

The most followed Northern Trust narrative sets a fair value of $171 against a last close of $173.87, so the story hinges on fairly tight valuation assumptions.

The company's recent organic growth and margin expansion are largely attributed to near-term operational efficiencies and balance sheet optimization (notably lower expense growth and improved operating leverage), yet investors may be overestimating the persistence of these improvements in light of ongoing industry fee pressure from the growing shift to passive investing and ETFs, which is likely to constrain long-term revenue growth and profit margins.

Want to see what sits behind that caution on margins? The narrative focuses on measured revenue growth, firmer profitability, and a future earnings multiple that would need to compress. The full breakdown brings all three together into one tight fair value range.

Result: Fair Value of $171 (OVERVALUED)

However, if Northern Trust’s AI rollout and cost cutting deliver stronger operating leverage, or if alternatives grow faster than modeled, today’s tight valuation case could shift quickly.

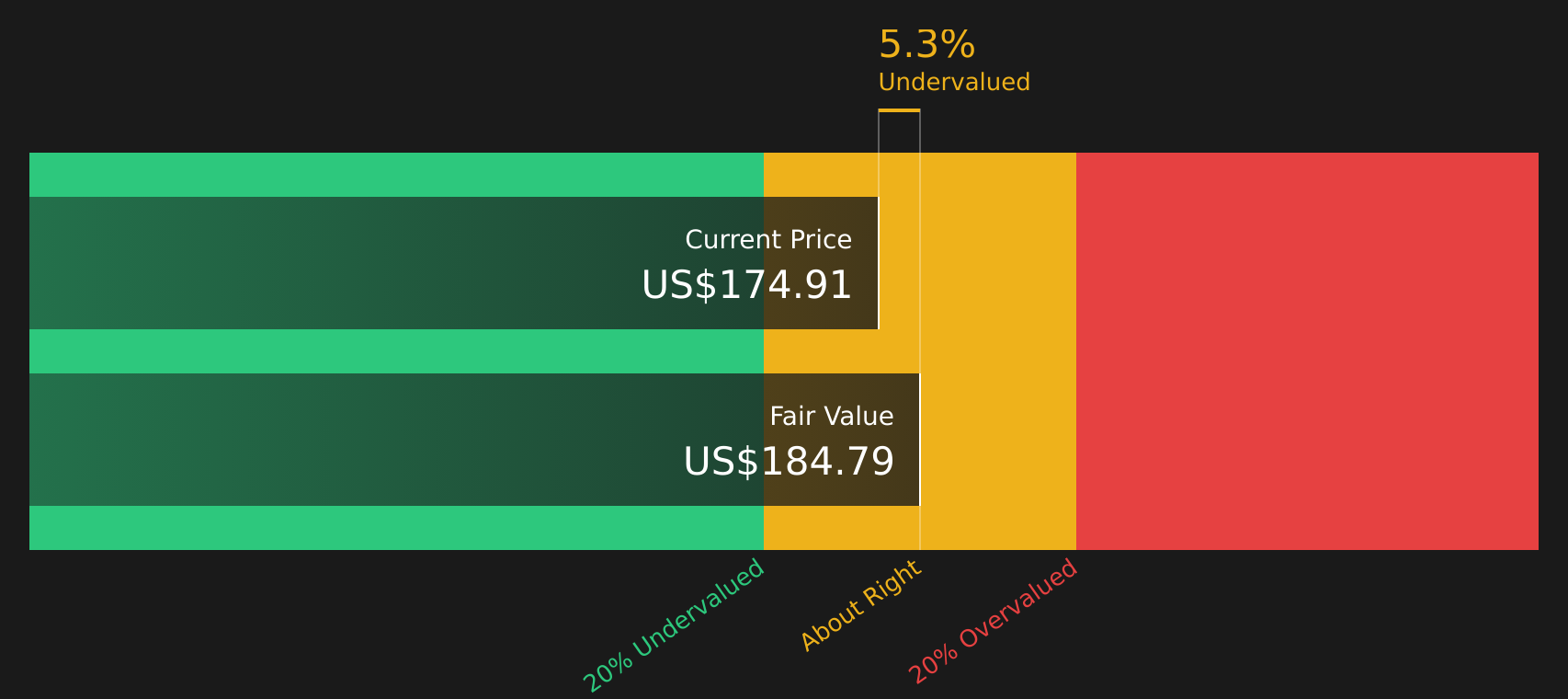

Another View on Northern Trust’s Valuation

While the prevailing Northern Trust narrative leans on tight earnings and price target assumptions, the SWS DCF model offers a different angle, with a fair value estimate of about US$178.76 against a share price of US$173.87, suggesting the stock screens as slightly undervalued rather than 2% overvalued. Which story do you find more convincing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Northern Trust for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Curious whether the mixed sentiment around Northern Trust fits your own view of the risk reward trade off? Take a closer look at the figures, weigh both sides of the story, and see how the balance stacks up with 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond Northern Trust?

If Northern Trust has sharpened your interest, now is the moment to scan a wider field of potential opportunities before the next wave of stories takes shape.

- Spot potential mispricings early by reviewing companies that currently look attractively valued using the 44 high quality undervalued stocks.

- Strengthen your focus on resilience by checking stocks that pass strict balance sheet and fundamentals filters through the solid balance sheet and fundamentals stocks screener (48 results).

- Get ahead of the crowd by searching for under followed opportunities with the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.