Northrop Grumman (NOC) Valuation Check After New MUX TACAIR Collaborative Combat Aircraft Win

Northrop Grumman Corp. NOC | 702.50 | +0.79% |

Northrop Grumman (NOC) is back in focus after being competitively awarded the U.S. Marine Corps MUX TACAIR Collaborative Combat Aircraft program, which pairs its uncrewed and autonomy technology with Kratos’ Valkyrie system.

The MUX TACAIR award lands at a time when momentum in Northrop Grumman’s shares has been picking up, with a 10.45% 1 month share price return and a 35.54% 1 year total shareholder return from a latest share price of US$629.32.

If this kind of defense contract is on your radar, it could be a good moment to see what else is moving across aerospace and defense stocks for another source of ideas.

With Northrop Grumman trading at US$629.32 after a strong 1 year run and sitting close to its average analyst price target, the key question is whether the MUX win still leaves upside on the table or if the market is already pricing in future growth.

Most Popular Narrative: 5.4% Undervalued

Against the last close of US$629.32, the most followed narrative pegs Northrop Grumman’s fair value closer to US$665, framing today’s price as modestly below that estimate.

The ramp-up of advanced autonomous and integrated systems such as Beacon and IBCS, combined with ongoing investments in solid rocket motor capacity (targeting a near doubling by 2029), positions the company to capitalize on high growth, higher margin market segments, thereby enhancing future operating margins and underlying cash flow.

Curious what earnings path and margin profile justify that higher fair value, and why the assumed future P/E climbs above today’s level and still trails peers? The full narrative lays out a tight link between revenue growth, profitability, and valuation that is not obvious from the current share price alone.

Result: Fair Value of $665.20 (UNDERVALUED)

However, that upside case can break if major U.S. programs like B 21 or Sentinel hit budget or timing setbacks, or if tighter buyback rules curb future capital returns.

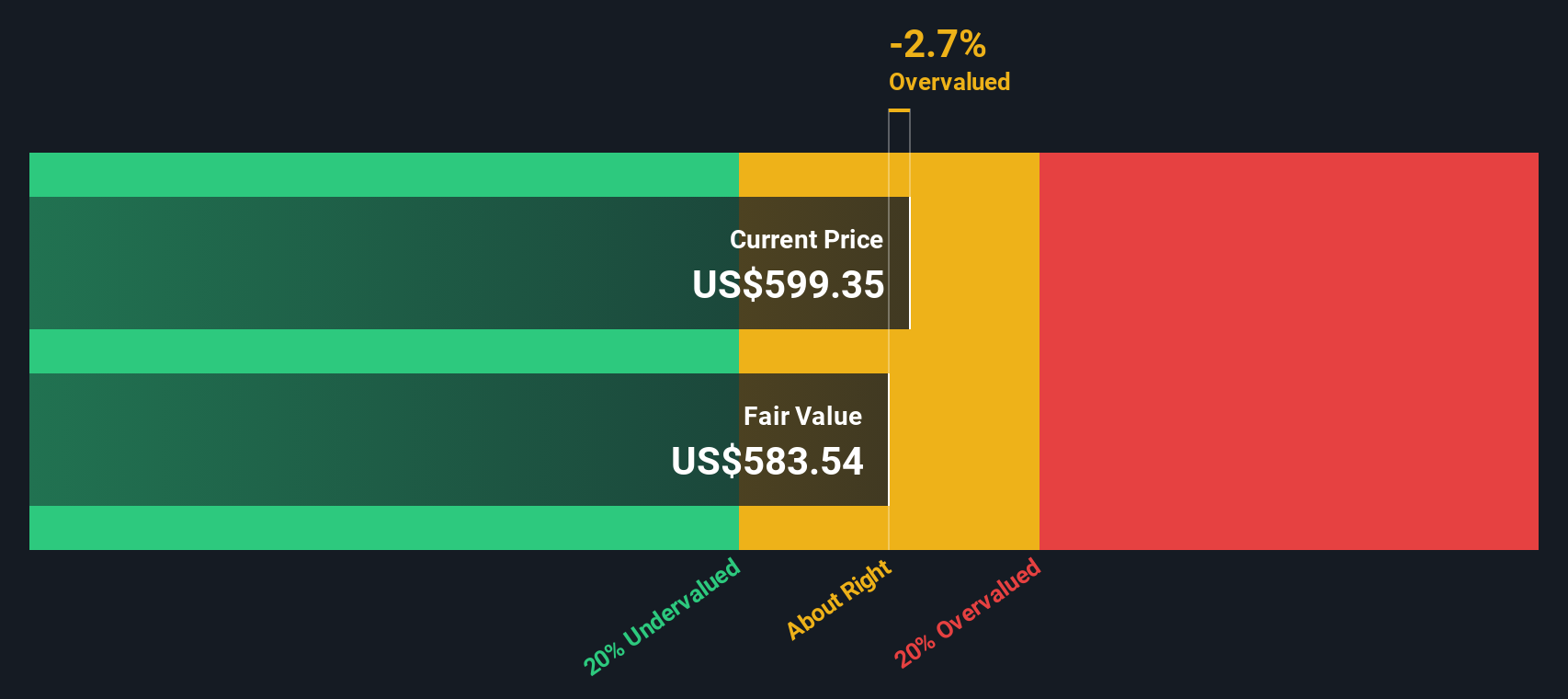

Another Angle: Our DCF Flags Overvaluation

The AI narrative leans on a fair value near US$665, yet our DCF model tells a different story. On that framework, Northrop Grumman’s fair value sits closer to US$510.71, which makes the current US$629.32 share price look rich rather than discounted. Which yardstick do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Northrop Grumman for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 881 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Northrop Grumman Narrative

If you look at the numbers and reach a different conclusion, or simply want to test your own assumptions, you can spin up a tailored view in minutes, Do it your way.

A great starting point for your Northrop Grumman research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Northrop Grumman has your attention, do not stop here, the right screener can quickly surface other opportunities that fit your style and keep you ahead of the crowd.

- Target potential turnaround stories with these 3536 penny stocks with strong financials that pair smaller price tags with solid financial underpinnings.

- Tap into machine learning and automation themes through these 26 AI penny stocks and see which names align with your view of where technology is headed.

- Zero in on companies trading below estimated cash flow value using these 881 undervalued stocks based on cash flows to spot ideas that might warrant a closer look.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.