NovoCure (NVCR) Is Down 19.7% After TRIDENT Misses Survival Endpoint In Earlier TTFields Use

NovoCure Ltd. NVCR | 0.00 |

- In June 2026, Novocure reported topline Phase 3 TRIDENT data showing that starting Tumor Treating Fields (TTFields) at the onset of chemoradiation for newly diagnosed glioblastoma did not significantly improve overall survival versus starting during the maintenance phase.

- While the trial missed its primary endpoint, the broadly similar survival outcomes and clean safety profile raise important questions about how TTFields should be sequenced rather than whether they should be used at all in this setting.

- Next, we’ll examine how TRIDENT’s lack of added survival benefit for earlier TTFields initiation may influence Novocure’s broader investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

NovoCure Investment Narrative Recap

To own NovoCure, you need to believe TTFields can keep expanding across multiple cancers and geographies, turning today’s concentrated GBM business into a broader, reimbursed franchise. TRIDENT’s miss on earlier GBM use is a setback for one specific timing question, but it does not appear to alter the near term focus on new indications and reimbursement progress. The biggest current risk remains execution on adoption and payor coverage while the company is still loss making.

The TRIDENT update sits alongside a very different recent milestone: FDA approval of Optune Pax for locally advanced pancreatic cancer in February 2026. That approval, backed by PANOVA 3, highlights how NovoCure’s near term catalysts now lean more on expanding into new tumor types than on squeezing extra benefit from earlier GBM use. How well pancreatic and lung launches convert into prescriptions and reimbursement will likely matter more than the TRIDENT timing question.

Yet despite these growth angles, investors should be aware that the company’s continued losses and dependence on a single platform leave NovoCure exposed if...

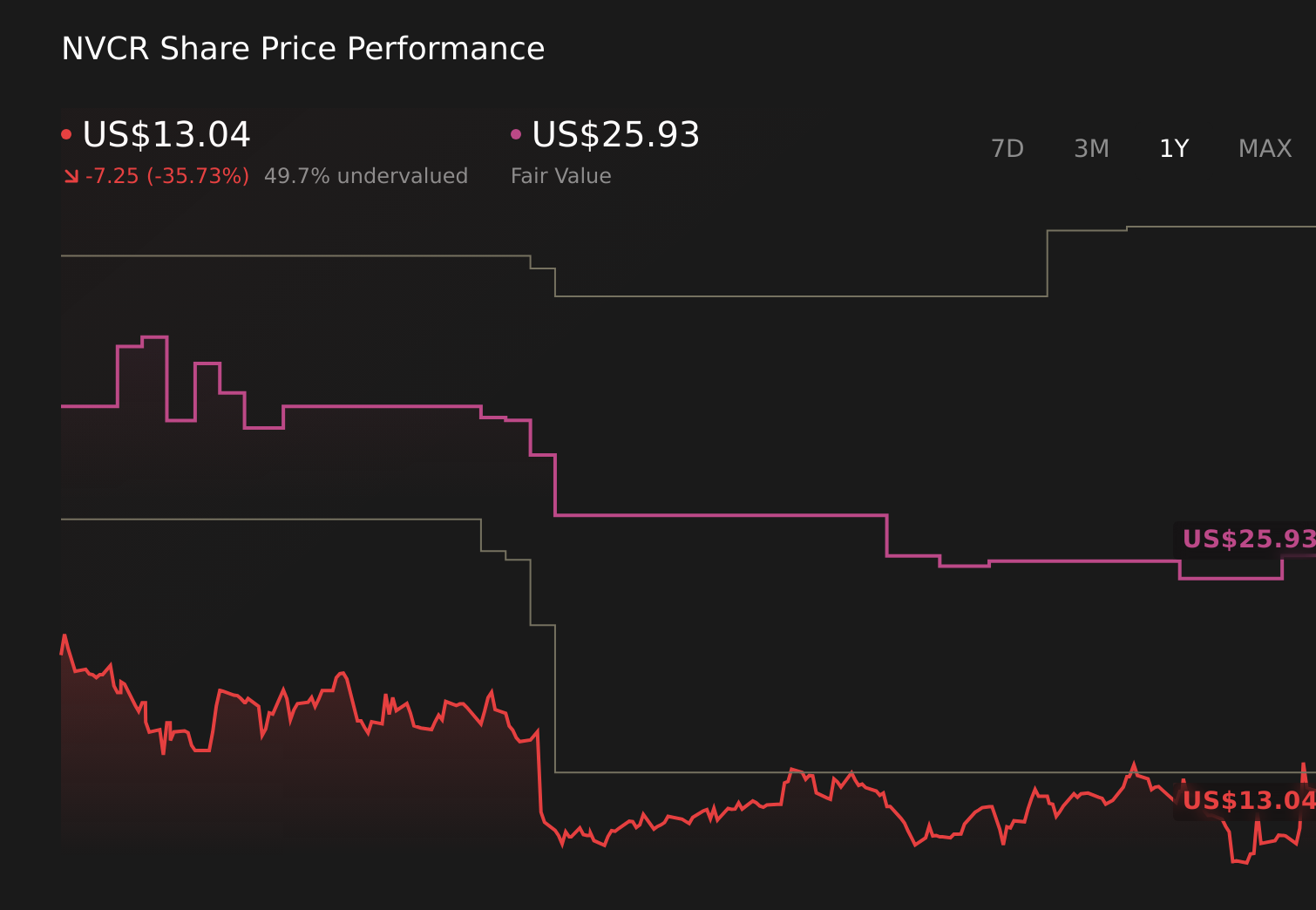

NovoCure's narrative projects $915.6 million revenue and $119.8 million earnings by 2029.

Uncover how NovoCure's forecasts yield a $26.07 fair value, a 83% upside to its current price.

Exploring Other Perspectives

Before TRIDENT, the most optimistic analysts were assuming revenue could reach about US$1.2 billion and positive earnings by 2029, but this new GBM data may force you to reassess how realistic those expectations are and whether TTFields can really outrun the competitive and reimbursement risks you just read about.

Explore 4 other fair value estimates on NovoCure - why the stock might be worth just $26.00!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your NovoCure research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free NovoCure research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NovoCure's overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- Find 45 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.