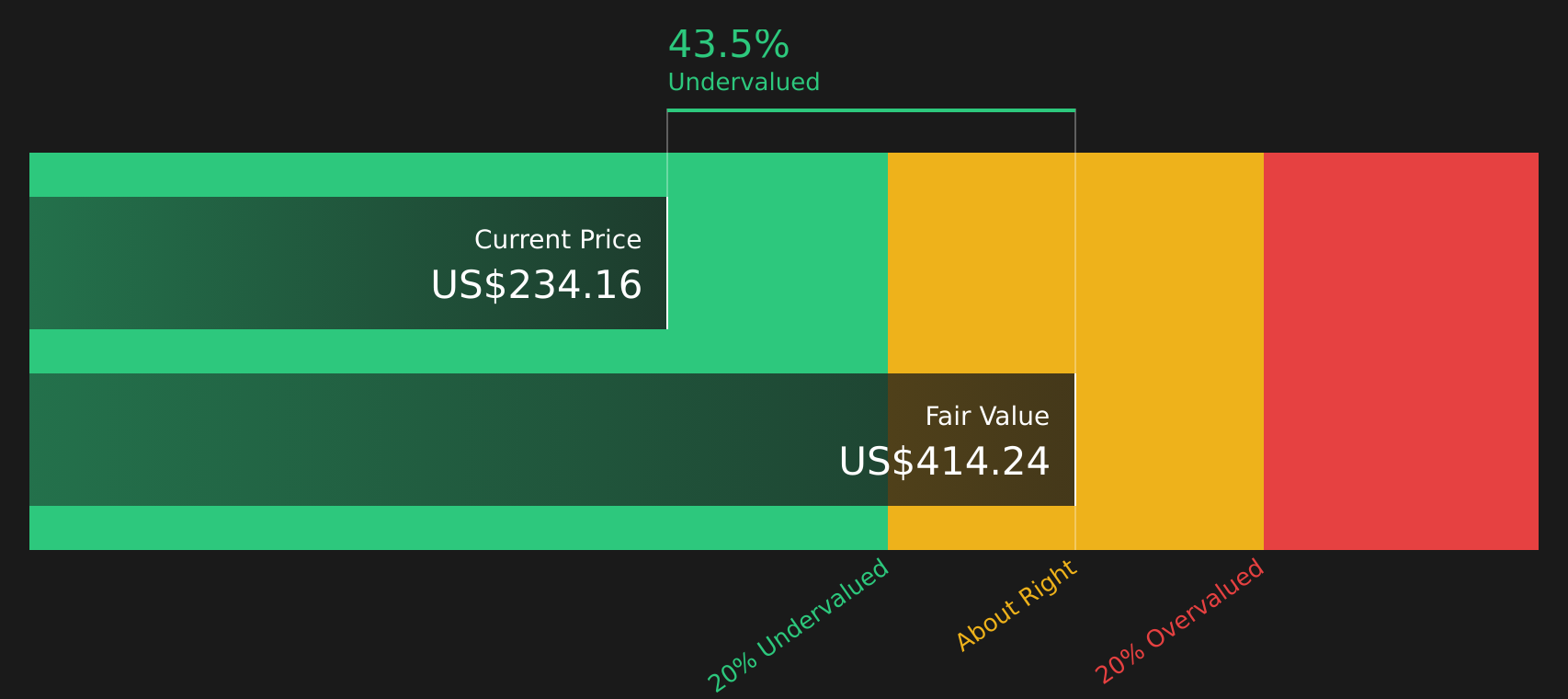

Nucor (NUE) Stock May Be 44% Undervalued On Fair Value Grounds

Nucor Corporation NUE | 0.00 |

Nucor’s share price has delivered a strong 178.7% total return over the past 5 years, while its current valuation signals indicate that the stock still screens as undervalued on both intrinsic value estimates and market multiples.

- A 178.7% return over 5 years suggests Nucor has already rewarded patient shareholders. Any further potential upside now matters more for new investors weighing entry price against risk.

- Expectations for Nucor’s future cash generation can support the current valuation. However, any setback in cash flow or returns on new investment may quickly narrow the implied discount.

- On Simply Wall St’s broader checks, Nucor appears mixed rather than a clear bargain, as it is assessed as undervalued in 3 of 6 tests here.

The key question is whether the current discount to intrinsic value provides Nucor with enough margin of safety after such a strong multi-year run.

Is Nucor a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) model here is based on projected cash flows available to shareholders over the long term. For Nucor, the latest twelve month free cash flow is about $656.4 million, and the projections assume recovering cash generation over time rather than sharp contraction. On those inputs, the model arrives at an estimated intrinsic value of about $413 per share.

That DCF outcome sits well above the current share price, which implies a 43.6% discount to the modelled intrinsic value. For readers, the key takeaway is that the cash flow profile used in this 2 Stage Free Cash Flow to Equity model suggests the market is pricing Nucor below what its projected free cash flows and terminal value would support, even after its strong multi year return.

On this DCF view, Nucor stock currently screens as undervalued relative to its estimated intrinsic value.

Our Discounted Cash Flow (DCF) analysis suggests Nucor is undervalued by 43.6%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

Is Nucor a Bargain on Earnings?

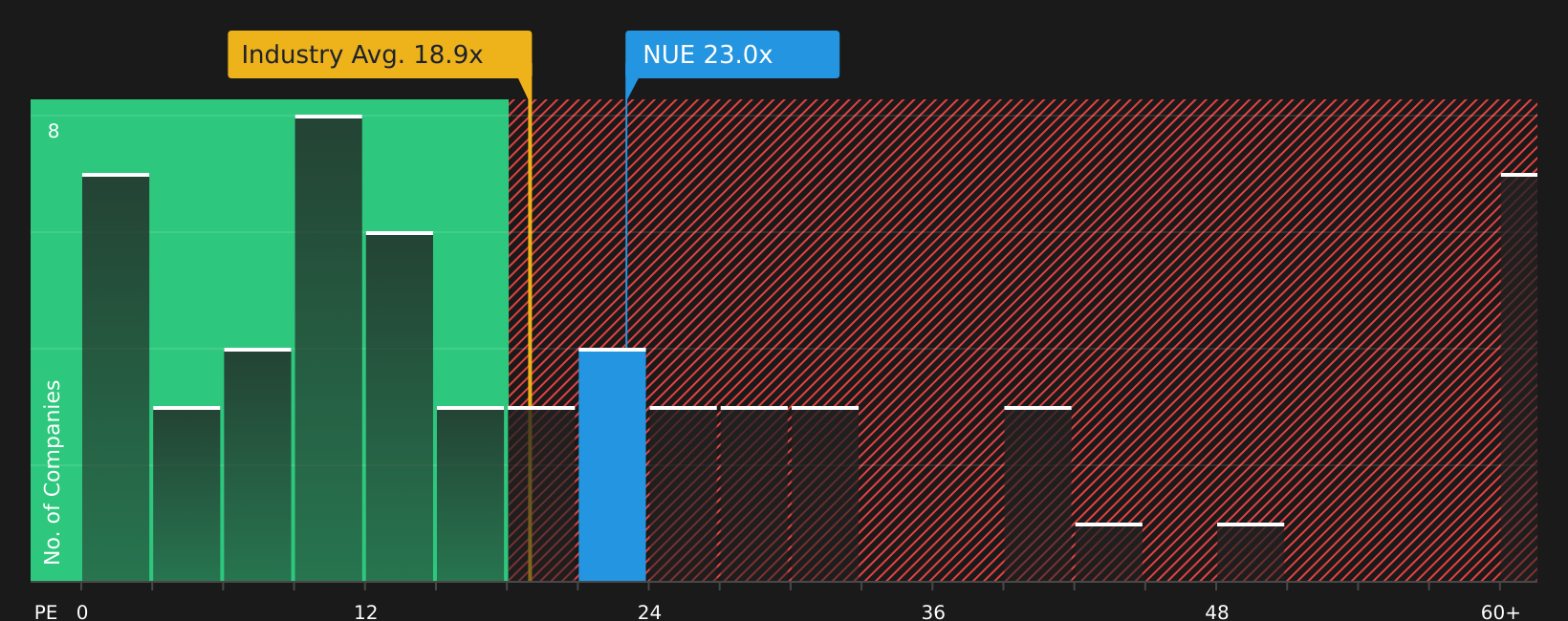

The P/E multiple suits Nucor because earnings remain a key yardstick for mature, cash generating industrial businesses. Nucor currently trades on a P/E of about 22.9x, compared with roughly 19.1x for peers and 18.4x for the wider Metals and Mining industry. On simple comparisons, the stock changes hands at a premium to both its direct peer set and the broader sector.

A more tailored benchmark, which factors in Nucor’s earnings profile, size and risk characteristics, points to a fair P/E of about 25.5x. That sits above the present 22.9x multiple and indicates the market is assigning a lower earnings multiple than this framework suggests would be reasonable, even after the strong longer term share price performance already logged.

On the P/E multiple, Nucor stock appears undervalued relative to this fair value benchmark.

The Nucor Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where Nucor’s valuation puzzle leaves off by spelling out which paths for revenue, margins and earnings would need to play out for the stock to be worth significantly more or less than today’s price, and they sit on the company’s Community page. Each one treats Nucor’s fair value as a thesis about how the business might develop over time, so you can see how that view holds up as new information arrives.

Community views on Nucor sit far apart, with one side focusing on tariff support and new mills, and the other on capacity and cyclical risk.

Bull case: 10% undervalued

"Nucor's significant capital reinvestment of $860 million, with two-thirds directed towards projects commencing operations within two years, is expected to diversify and strengthen future earnings..."

Bear case: 23% overvalued

"As the West Virginia sheet mill moves through commissioning and into an early 2027 shipment ramp, a pessimistic outcome is that new capacity arrives into a flat domestic sheet market..."

Do you think there's more to the story for Nucor? Head over to our Community to see what others are saying!

The Bottom Line

For Nucor, both the Discounted Cash Flow (DCF) view and the earnings multiple workup point in the same direction, with the intrinsic value estimate suggesting a sizeable 43.6% discount and the P/E check also flagging the stock as undervalued. At the same time, the broader set of valuation checks is mixed, so the signals are not unequivocal. From here, a key question is whether Nucor can translate its investment program and cash generation plans into sustained returns, or whether the market has correctly priced in cyclical and capacity risks that keep the stock cheap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.