Nucor (NUE) Stock May Be 46% Undervalued On Cash Flow

Nucor Corporation NUE | 0.00 |

Nucor stock has delivered a strong 144.7% return over the past 5 years, yet current checks suggest the market price may still sit below an intrinsic value estimate based on a Discounted Cash Flow (DCF) approach and supporting multiples. That combination, alongside a mixed overall value score, puts the focus on whether the recent gains have already reflected the key fundamentals.

- Over 5 years, Nucor has returned 144.7%, which puts long term holders in a significantly stronger position than when they started.

- For valuation, the central support can come from the company’s ability to turn its operations into steady cash flows. Any pressure on margins or cash generation would be the main risk to that picture.

- Nucor screens as undervalued on both a Discounted Cash Flow (DCF) estimate and earnings multiples. However, the broader checks form a mixed picture, with the stock clearing 4 of 6 valuation tests on value score.

The stock's next move may depend on whether Nucor’s current share price continues to trade at a discount to its intrinsic value estimate or whether that gap has already largely closed.

Does Nucor Look Undervalued on Cash Flow?

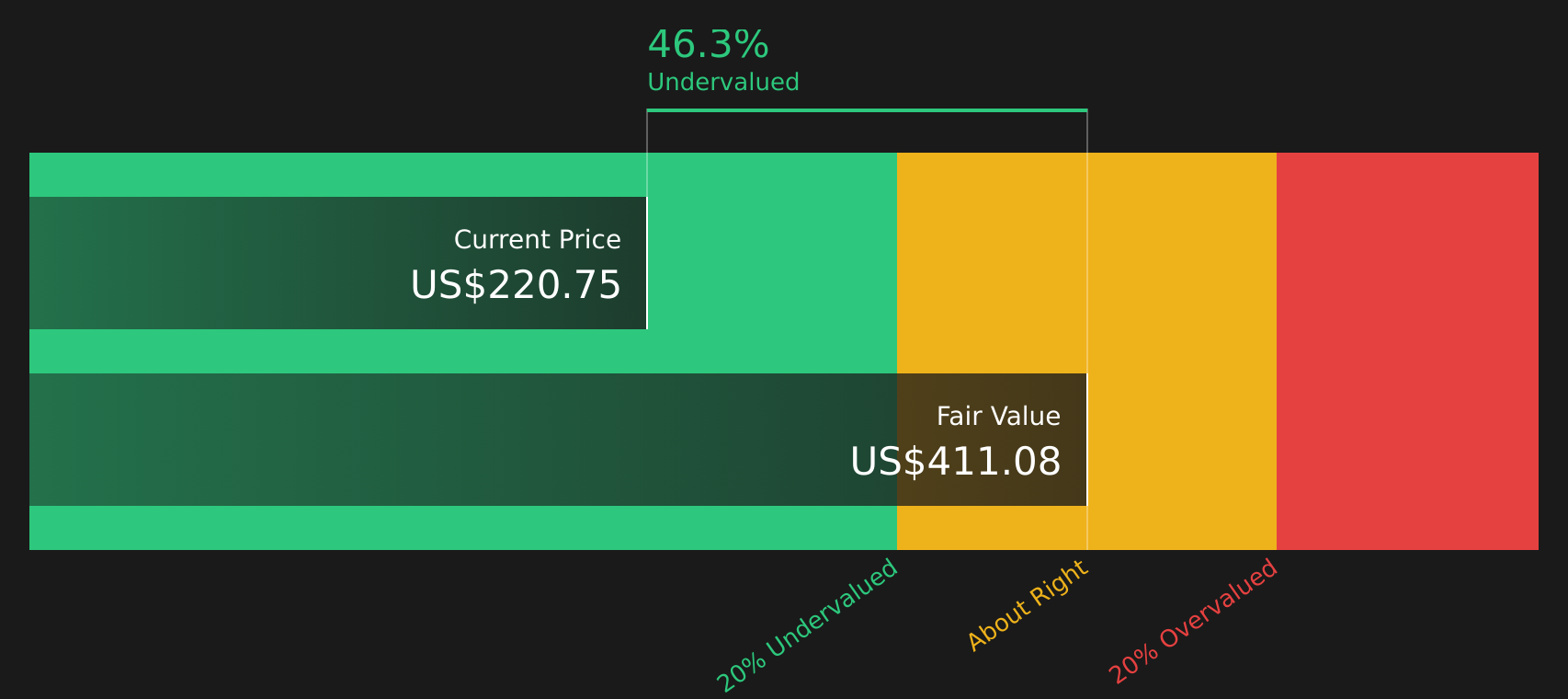

The Discounted Cash Flow (DCF) model here uses projected cash flow to estimate what Nucor stock could be worth based on its own cash generation. Nucor’s latest twelve month free cash flow sits at about $656.4 million, with the model assuming that cash flows grow from this base over time rather than shrink. Using those projections, the 2 Stage Free Cash Flow to Equity approach arrives at an estimated intrinsic value of about $411 per share.

Compared with the current market price, that intrinsic value implies the stock trades at roughly a 46.3% discount. For readers, the key point is that the model is not relying on extreme growth rates. Instead, it uses a path from today’s cash flow towards higher, but still finite, levels by 2030 and beyond.

On this DCF view, Nucor stock currently screens as undervalued relative to its projected cash flows.

Our Discounted Cash Flow (DCF) analysis suggests Nucor is undervalued by 46.3%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Is Nucor a Bargain on Earnings?

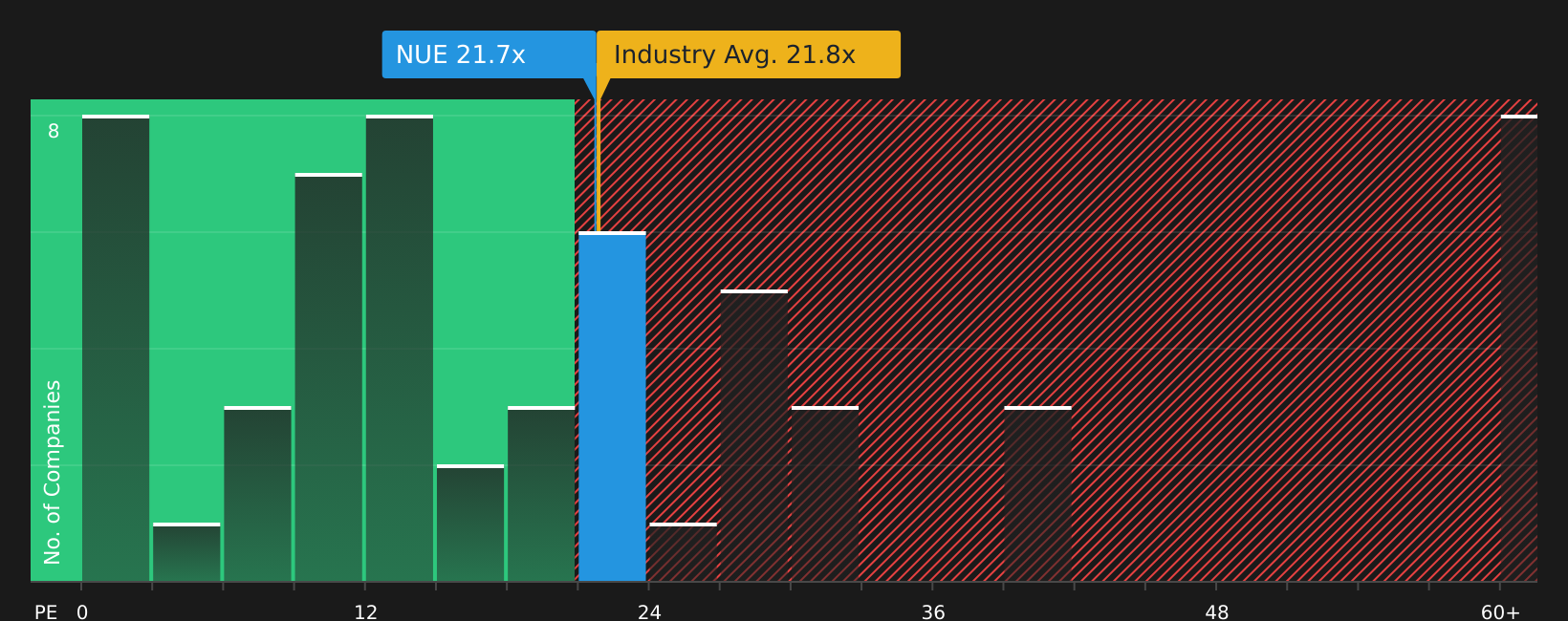

P/E is a useful lens for Nucor because earnings still sit at the center of how many investors assess mature, cash generating industrial stocks. On this basis, Nucor currently trades on a P/E of about 21.7x, which is very close to the wider Metals and Mining industry average of around 21.8x and above a peer group average near 18.1x.

The fair P/E ratio implied by the model for Nucor is about 25.7x, which is higher than where the stock trades today. That gap suggests the current earnings multiple does not fully reflect the company’s profile when earnings quality, scale and risk are considered together, even if the headline P/E looks roughly in line with the sector.

On this earnings metric, Nucor stock appears undervalued relative to the fair P/E that the model assigns it.

The Nucor Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Nucor take the valuation puzzle a step further by spelling out the specific futures for Nucor's growth, margins and earnings that would need to play out for the stock to be worth materially more or less than today’s price, and they sit on the company’s Community page. Where a single ratio or model offers one output, these narratives unpack the assumptions behind it so you can watch how closely reality lines up over time.

Community views on Nucor sit far apart, with one side leaning into tariff support and new mills, and the other worried about capacity and earnings risk.

Bull case: 15% undervalued

"Nucor's significant capital reinvestment of $860 million, with two-thirds directed towards projects commencing operations within two years, is expected to diversify and strengthen future earnings..."

Bear case: 17% overvalued

"As the West Virginia sheet mill moves through commissioning and into an early 2027 shipment ramp, a pessimistic outcome is that new capacity arrives into a flat domestic sheet market..."

Do you think there's more to the story for Nucor? Head over to our Community to see what others are saying!

The Bottom Line

For Nucor, both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings multiple view point in the same direction, suggesting the stock still screens as undervalued rather than stretched. At the same time, the broader set of checks is only mixed, which keeps the focus squarely on whether the current discount is compensation for real risks around margins, cash generation and capacity additions. From here, the key question is whether Nucor can sustain cash flows and earnings at levels that justify the intrinsic value estimate, or whether the market is already correctly pricing in potential pressure on future profitability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.