Oceaneering International (OII) Could Be 14% Overvalued Following Its $500 Million Debt Reset

Oceaneering International, Inc. OII | 0.00 |

Oceaneering International (OII) has drawn fresh attention after launching a cash tender offer for its $500 million 6.000% Senior Notes due 2028, alongside issuing $500 million of new 6.875% Senior Notes maturing in 2034.

Recent debt moves appear to have coincided with improving sentiment, with Oceaneering International’s 1-day share price return of 1.68% contributing to a 7-day share price return of 11.01% and a year-to-date share price return of 61.09%. Its 1-year total shareholder return of 91.99% points to stronger momentum over a longer horizon.

If you are looking beyond Oceaneering International and want to see what else is moving in related areas, this could be a useful moment to review 29 robotics and automation stocks.

With Oceaneering International stock up 61.09% year to date, trading around $40.03 and sitting above a consensus price target of $36.50, the key question is whether there is still an opportunity for investors to consider or if the market is already pricing in future expectations.

Most Popular Narrative: 14% Overvalued

At $40.03, Oceaneering International is trading above the most followed fair value estimate of $35.25, which is built using a 7.6% discount rate and detailed long term forecasts.

The ongoing global energy transition and intensifying decarbonization efforts continue to limit new offshore oil & gas developments, which threatens Oceaneering's long-term project backlog and could ultimately reduce future revenue growth as the addressable market gradually contracts. There is increasing investor and regulatory pressure to reallocate capital away from traditional oilfield service providers; this trend is likely to hinder capital flows to Oceaneering's core business lines, potentially compressing growth prospects, restraining order activity, and constraining revenue and profit expansion.

Want to see what has to happen for Oceaneering International to justify this valuation? The narrative leans on modest revenue growth, sharply lower margins, and a much richer future earnings multiple.

Result: Fair Value of $35.25 (OVERVALUED)

However, the growth of Oceaneering International’s Aerospace and Defense Technologies business and its recurring offshore service work could soften energy transition pressures and challenge the 14% overvalued narrative.

Another View: What Oceaneering International’s Earnings Multiple Is Saying

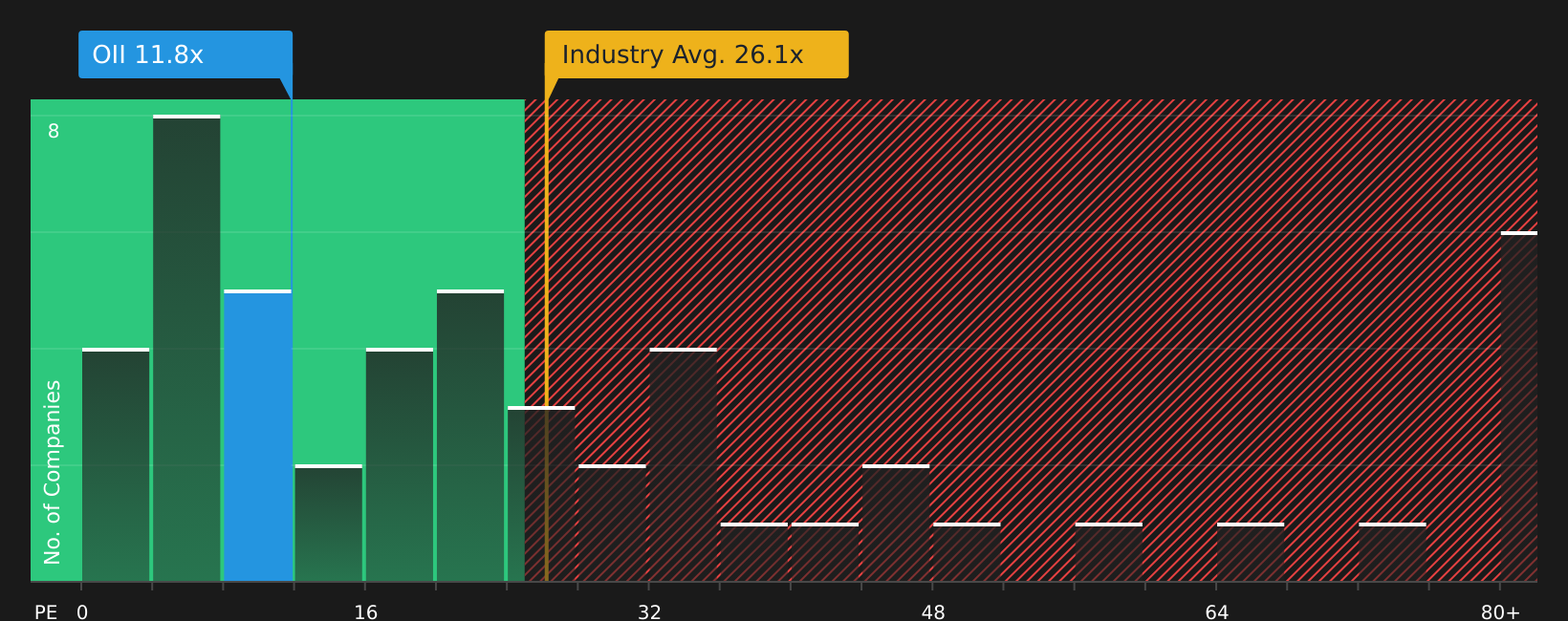

There is a twist to the 14% overvalued narrative. At around $40.03, Oceaneering International trades on a P/E of 11.8x, which is much lower than the US Energy Services industry at 26.1x and the peer average at 33.8x, yet higher than its fair ratio of 6.1x.

That gap suggests the stock may still carry valuation risk if the market drifts back toward the fair ratio, even though it looks cheaper than industry and peers. The key question is which reference point you treat as more important.

Next Steps

With sentiment on Oceaneering International looking mixed, take a moment to review the full picture for yourself, including the 2 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Oceaneering International?

If you are serious about building a stronger portfolio, do not stop at Oceaneering International, use the Simply Wall Street Screener to uncover fresh opportunities.

- Target potential mispricing by reviewing companies on the 44 high quality undervalued stocks that may offer a margin of safety and quality fundamentals.

- Strengthen portfolio resilience by focusing on businesses featured in the solid balance sheet and fundamentals stocks screener (48 results) that pair financial stability with consistent performance metrics.

- Spot underfollowed opportunities early by scanning the screener containing 19 high quality undiscovered gems before broader market attention catches up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.