One Credit Engine One Asset Sensitive Bank One Volatile Deal Maker

Atlantic Union Bankshares Corporation AUB | 0.00 |

Markets are wrestling with a new Fed Chair, stubborn 4.2% CPI inflation and Treasury yields at multi year highs. That mix can quickly reshuffle which stocks look resilient and which look vulnerable. For large U.S. financial companies, the debate over interest rates, balance sheet reduction and long term yields is not just theory; it can influence funding costs, lending activity and investor appetite for risk. This article highlights 3 stocks from a U.S. big bank and financial sector screener that are especially exposed to these Fed driven catalysts, and explains why some investors may see potential opportunity or reasons for caution.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

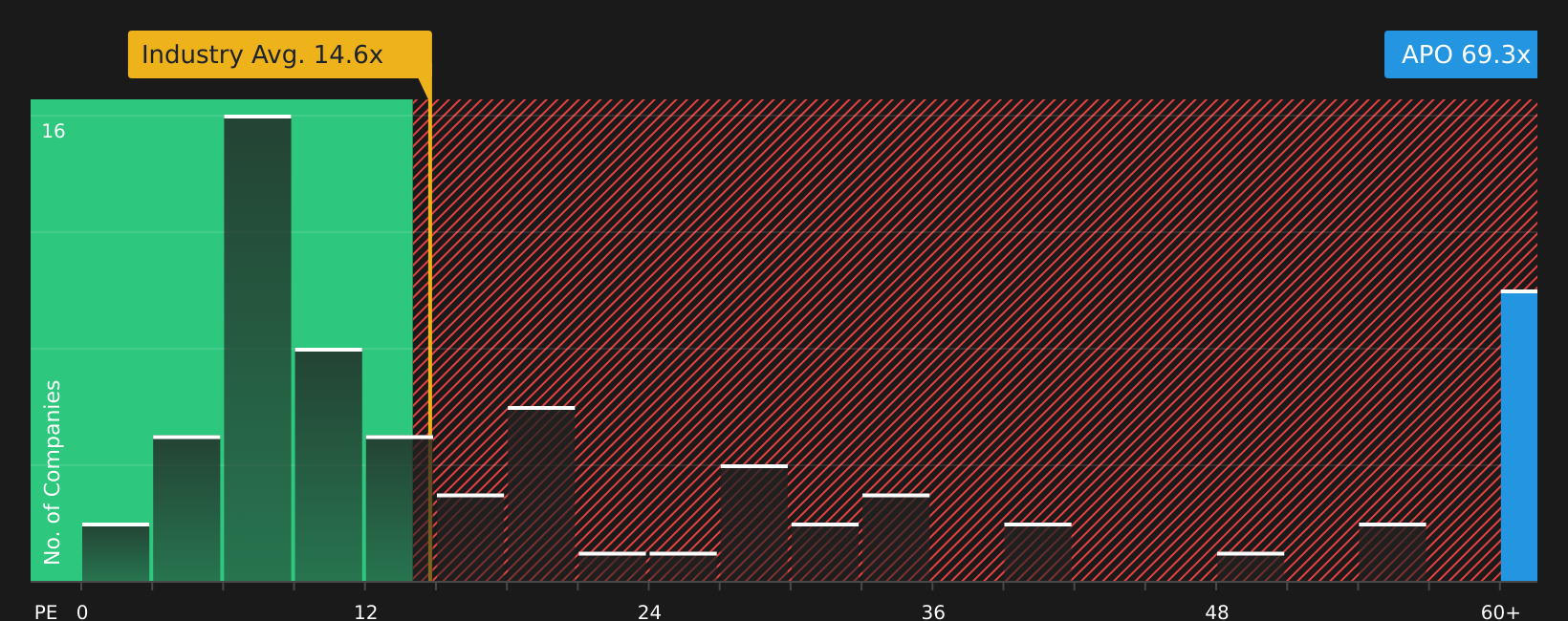

Apollo Global Management (APO)

Overview: Apollo Global Management is a large alternative asset manager that invests across credit, private equity, real estate, infrastructure and retirement services, using both public and private markets to provide capital and financial products to institutions and individuals worldwide.

Operations: Apollo generates most of its revenue from Retirement Services at about US$24.3b, with Asset Management contributing about US$5.8b and Principal Investing about US$1.5b.

Market Cap: US$77.2b

For investors watching how a higher for longer rate backdrop and Fed balance sheet decisions affect financial stocks, Apollo stands out as a credit focused asset manager that often prefers a higher rate environment and rising risk premiums. Its scale in retirement services and private credit gives it exposure to demand for income focused products. However, the stock carries a high P/E multiple, a forecast revenue decline and a funding model that depends on external borrowing rather than deposits. In addition, there has been insider selling and recent deal activity from AI infrastructure financing to large health care buyouts, creating a complex story that rewards closer analysis of what is driving earnings versus valuation.

Apollo’s credit engine and retirement platform are pulling in one direction, while a high P/E, forecast revenue decline and funding mix pull in another. Get the context in the analysis report for Apollo Global Management

Atlantic Union Bankshares (AUB)

Overview: Atlantic Union Bankshares is a regional U.S. bank that offers a full range of consumer and business banking services, from deposits and loans to wealth management, insurance, and treasury services, across its branch network and digital channels in the Mid-Atlantic and Southeast.

Operations: The bank generates most of its revenue from Wholesale Banking at about US$666.6m, followed by Consumer Banking at about US$494.5m and Corporate Other at about US$240.2m, all from customers in the United States.

Market Cap: US$5.8b

Atlantic Union Bankshares sits in the sweet spot of this higher rate conversation, with management describing the bank as “fairly asset sensitive,” meaning rising short term rates and wider net interest margins can support earnings. This is reflected in recent guidance for fully taxable equivalent net interest income of around US$1.34b to US$1.35b for 2026. At the same time, investors are dealing with a regional franchise that has concentrated exposure to a few fast growing states, a large recent one off loss of US$161.4m in the trailing year, and an earnings profile that has been flat over five years. In addition, there are governance reforms, a US$250m buyback authorization and a premium P/E. The key question is whether the current setup fairly reflects both the potential benefits from a higher for longer Fed and the risks around credit quality, deposit costs and further one off hits.

Atlantic Union’s “fairly asset sensitive” setup, premium P/E and US$250m buyback authorization could be masking a sharper earnings swing than the five year flat trend suggests; the real inflection point may sit inside the 4 key rewards and 1 important warning sign

Moelis (MC)

Overview: Moelis & Company is a global investment bank that advises corporations, financial sponsors, governments and sovereign wealth funds on mergers and acquisitions, restructurings, capital raising and broader corporate finance decisions across major regions including the Americas, Europe, the Middle East, Asia and Australia.

Operations: Moelis generates all of its revenue, about US$1.53b, from its investment banking advisory business, with around US$1.29b coming from the United States and the rest split between Europe and other international markets.

Market Cap: US$5.5b

Moelis operates in areas where a more volatile, higher rate environment can translate into client action, with rising financial stress and choppy equity and credit markets often lifting demand for its M&A and restructuring advice. The firm is pushing deeper into private capital advisory and tech sectors while continuing to hire senior bankers. This can support fee momentum but also keeps compensation and expansion costs high if deal activity slows. Earnings have been lumpy and the latest quarter showed softer profit even as revenue met expectations. High return on equity and ongoing buybacks and dividends indicate management is still committing capital to shareholders. The key consideration is how this mix of volatility, expansion and Fed driven catalysts affects earnings quality and valuation for Moelis in the years ahead.

Moelis’ expanding advisory reach and high return on equity could be masking where the real earnings power sits. Check the analyst forecasts for Moelis to see what Wall Street might be missing next.

The three stocks covered here are just a starting point, and the full U.S. Big Bank and Financial Sector Stocks screener surfaces 21 more large U.S. financial companies with equally compelling interest rate and balance sheet stories waiting to be unpacked. Use Simply Wall St to identify, filter and analyze the specific catalysts and narratives that matter to you so you can focus on the highest conviction opportunities across the sector.

Take Control of Your Investment Journey

If Moelis or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Big Banks?

Fresh ideas do not stay under the radar for long. Spot stocks with potential momentum or quiet pullbacks before the crowd catches up and the best entry points are gone, and consider acting promptly.

- Scan income plays in the 8 dividend fortresses that focus on higher payouts supported by solid balance sheets and robust cash generation.

- Review the curated 33 robotics and automation stocks that may benefit from broader adoption of robotics across factories, warehouses and everyday products.

- Explore the hand picked 48 AI infrastructure stocks that provide the chips, hardware and networks used in large scale machine learning.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.