Otter Tail (OTTR) Stock Could Be 3.3% Undervalued As Utility Growth Plans Come Into Focus

Otter Tail Corporation OTTR | 0.00 |

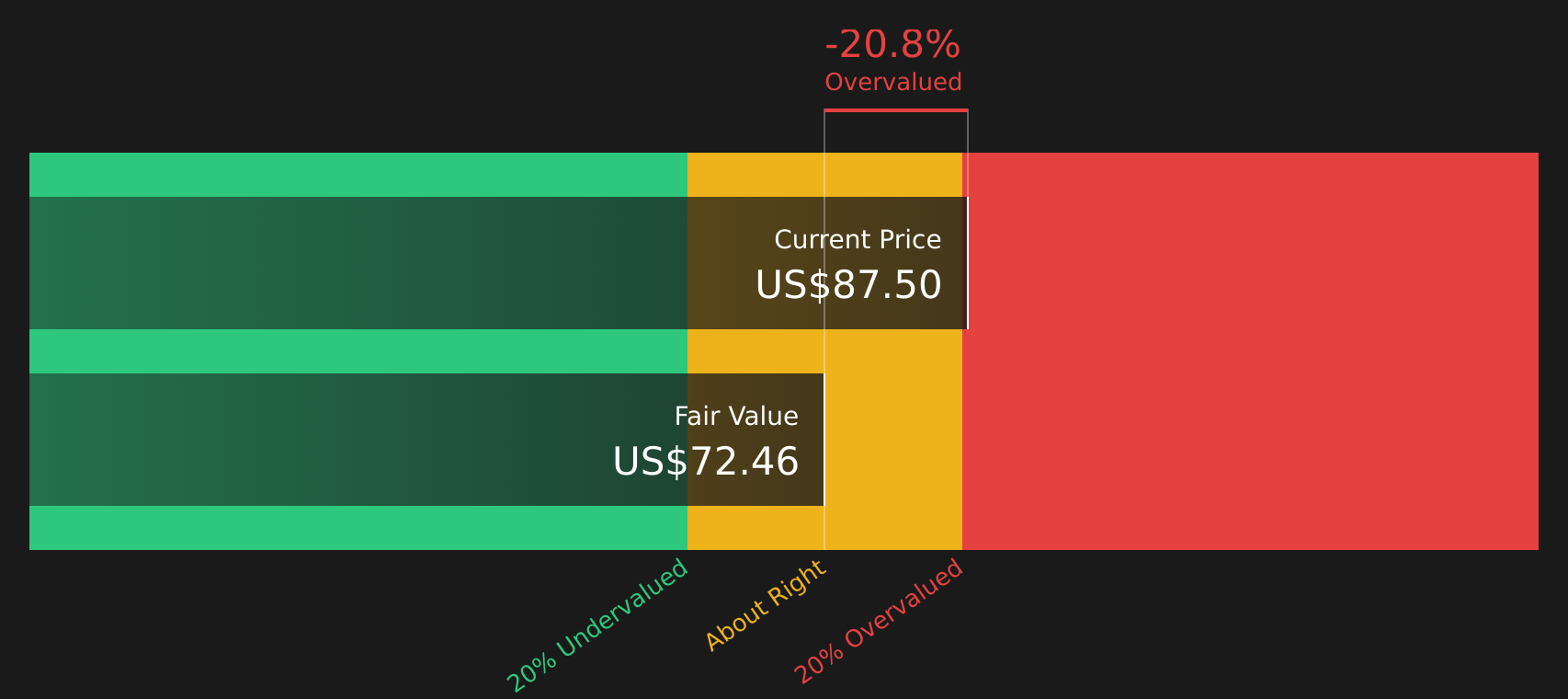

Otter Tail (OTTR) is back on investors’ radar after fresh trading data highlighted recent share performance, including a last close of $87.50 and a year to date total return of 7.4%.

Recent trading shows mixed short term momentum for Otter Tail, with a 1 day share price return of 0.89% and a 7 day share price return that declined 2.33%, while the 1 year total shareholder return of 17.29% and 5 year total shareholder return of 102.01% point to stronger longer term gains.

If Otter Tail has you looking at utilities and infrastructure, it can be useful to widen your watchlist to opportunities linked to the power grid and energy transition via 34 power grid technology and infrastructure stocks

With Otter Tail trading close to a US$90.50 analyst price target and an intrinsic value estimate that sits above the current US$87.50 share price, the key question is whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 3.3% Undervalued

With Otter Tail’s most followed narrative pointing to a fair value of $90.50 against a last close of $87.50, the current share price sits slightly below that narrative anchor and puts the spotlight on what is baked into those assumptions.

Otter Tail is projecting utility segment compounded annual earnings growth of 9% driven by $1.4 billion in capital investments focused on grid reliability, renewables, and transmission, supported by favorable rate recovery mechanisms and regulatory approvals, which could underpin strong, steady earnings and revenue expansion.

Read the complete narrative. Read the complete narrative.

Want to see what sits behind that projected earnings path for Otter Tail? The narrative leans on shifting revenue mix, changing margins and a higher future earnings multiple. Curious which assumption matters most to that $90.50 fair value call and how sensitive it is to even small changes in those inputs? The full breakdown reveals the numbers driving that conclusion.

Result: Fair Value of $90.50 (UNDERVALUED)

However, Otter Tail’s story could shift if PVC pipe litigation outcomes or changing environmental and regulatory requirements weigh more heavily on costs and future project economics.

Another View: Otter Tail Through A Cash Flow Lens

While the prevailing Otter Tail narrative leans on a fair value of $90.50, the Simply Wall St DCF model points in the opposite direction, with an estimate of $72.46. This suggests the stock is trading above its future cash flow value and leaves less room for execution hiccups.

The gap between a multiples based fair value and a cash flow based estimate raises a simple question for investors: which set of assumptions feels closer to how Otter Tail will actually perform over time?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Otter Tail for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Balancing Otter Tail’s mix of risks and rewards comes down to your own risk tolerance, so review the full picture quickly and weigh up the 2 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Otter Tail?

Otter Tail may be front of mind today, but your next strong opportunity could be sitting in plain sight, so do not miss the chance to widen your search.

- Target resilient income by scanning companies with robust payouts and defensive characteristics through 8 dividend fortresses.

- Hunt for quality at a reasonable price by filtering for companies that pair solid fundamentals with appealing valuations using the 45 high quality undervalued stocks.

- Prioritise capital protection by focusing on companies with steadier profiles and lower overall risk signals via the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.