Owens Corning (OC) Stock After 73% Five-Year Gain Is There Still Upside?

Owens Corning OC | 0.00 |

- If you are wondering whether Owens Corning stock is priced attractively or already reflects most of its potential, the current valuation story is worth a closer look.

- At a recent close of US$156.05, Owens Corning has posted returns of 25.2% over the past 7 days, 24.0% over 30 days, 36.7% year to date, 16.3% over 1 year, 25.4% over 3 years, and 73.4% over 5 years.

- Recent coverage around Owens Corning has focused on its role in the building materials sector and on how market sentiment is responding to broader construction and housing activity. This context helps explain why investors are reassessing the stock and paying closer attention to valuation.

- Owens Corning currently has a valuation score of 3 out of 6. This reflects where it screens as undervalued across several checks. The rest of this article will compare different valuation approaches before finishing with a more holistic way to think about what the stock might be worth.

Approach 1: Owens Corning Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company might be worth by projecting its future cash flows and then discounting those back to today’s value. For Owens Corning, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flows available to shareholders.

Owens Corning most recently reported trailing free cash flow of about $991.5 million. Analysts provide explicit forecasts out to 2027, with free cash flow for that year estimated at $851.1 million. Beyond that, Simply Wall St extrapolates cash flows out to 2035, with the ten year projection in 2035 sitting at $790.4 million, using a series of gradual adjustments from the analyst baseline.

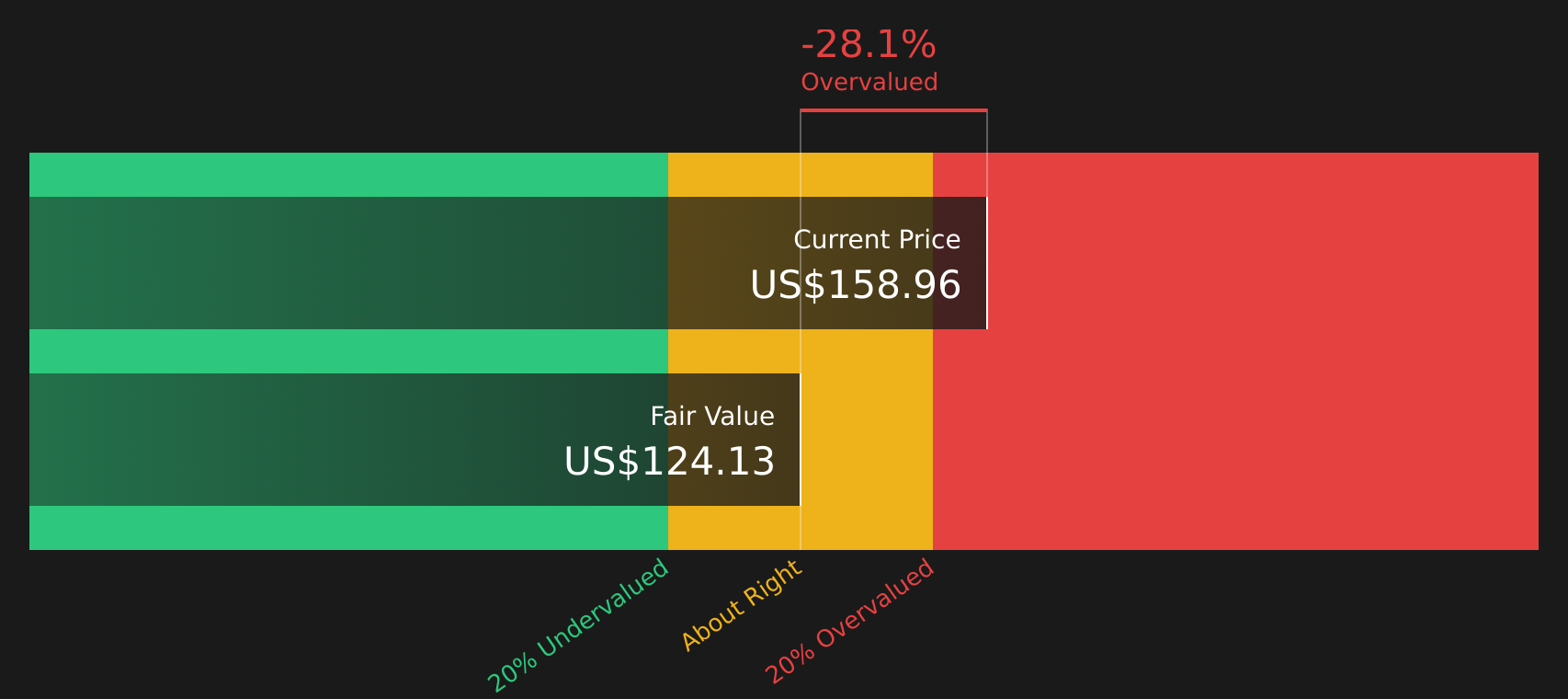

Discounting these projected cash flows back to today produces an estimated intrinsic value of $120.62 per share. Compared with the recent share price of $156.05, the DCF implies that Owens Corning stock trades at a premium, with the model indicating the stock is about 29.4% above this cash flow based estimate.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Owens Corning may be overvalued by 29.4%. Discover 42 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Owens Corning Price vs Sales

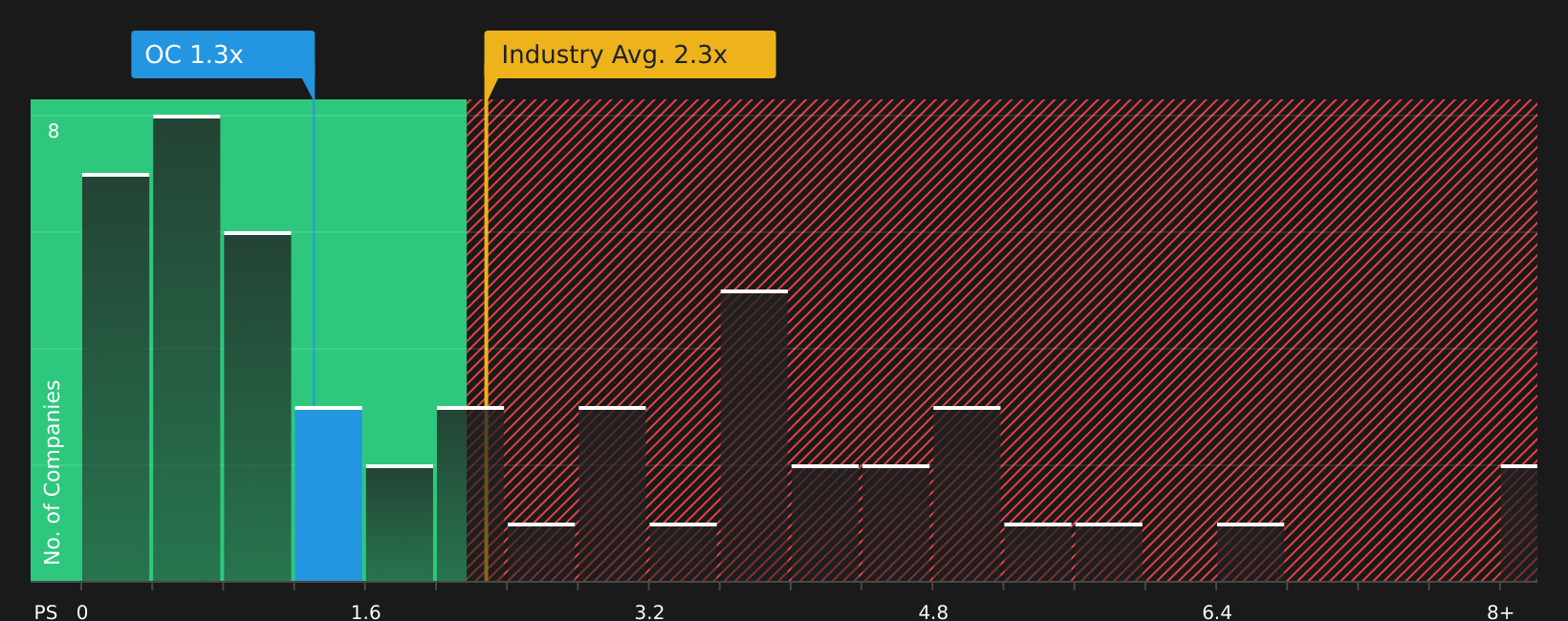

For a profitable company like Owens Corning, the P/S ratio can be a useful cross check on valuation because it links what you pay for the stock to the revenue the business generates, regardless of short term swings in earnings.

In general, higher growth expectations and lower perceived risk tend to support a higher “normal” or “fair” P/S ratio, while slower expected growth or higher risk usually line up with a lower multiple. That is why context is important when you compare any stock’s current multiple with simple averages.

Owens Corning currently trades on a P/S ratio of 1.28x. This sits below the Building industry average of 2.23x and also below the peer average of 4.19x that groups similar companies together. Simply Wall St’s “Fair Ratio” for Owens Corning is 1.80x. This proprietary metric estimates the P/S level that could be reasonable given factors such as earnings growth, profit margins, industry, market cap and key risks.

Because the Fair Ratio incorporates these company specific drivers, it is often more informative than relying only on broad peer or industry comparisons. With the actual P/S of 1.28x sitting below the Fair Ratio of 1.80x, Owens Corning screens as undervalued on this metric.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Owens Corning Narrative

Earlier the article mentioned that there is an even better way to understand what Owens Corning might be worth. Narratives take center stage here as a simple story that you attach to your numbers, where your view on the company is linked directly to assumptions like future revenue, earnings, margins and a Fair Value that you can compare with the current price.

On Simply Wall St’s Community page, Narratives are an accessible tool that help you tie Owens Corning’s business story to a forward looking forecast and then to a Fair Value estimate. This way you can see at a glance whether your story implies the stock should trade closer to the more bullish US$166.00 view or the more cautious US$110.00 view.

Because Narratives on the platform are refreshed as new information comes in, such as updated analyst targets between US$174.00 at the high end and US$125.00 at the low end, news on dividend policy, or changes to discount rates and margin assumptions, your Owens Corning view does not stay static. You can keep checking whether your Fair Value still lines up with the live share price when you are deciding whether to buy, hold or sell.

For Owens Corning however we will make it really easy for you with previews of two leading Owens Corning Narratives:

Fair value in this bullish narrative: US$166.00

Implied pricing gap vs last close: Owens Corning trades about 27.7% above this narrative fair value.

Revenue growth assumption: 3.31% annual decline

- Analysts in this camp anchor on a higher US$166.00 fair value that sits toward the top of the current target range and ties directly to their earnings and margin assumptions.

- The story leans on new roofing and insulation capacity, efficiency projects, and a broader contractor network to support EBITDA margins and earnings resilience across cycles.

- Key risks focus on weaker residential and nonresidential demand, Doors segment pressure, and the possibility that heavy capital investment delivers lower returns if construction activity stays subdued.

Fair value in this more cautious narrative: US$146.21

Implied pricing gap vs last close: Owens Corning trades about 6.7% above this narrative fair value.

Revenue growth assumption: 2.92% annual growth

- This view uses the analyst consensus fair value of about US$146.21, which sits between the US$174.00 high target and US$125.00 low target and frames Owens Corning as closer to fairly priced.

- The narrative highlights capacity and technology investment, a tilt toward higher margin products, and cost efficiencies, but pairs this with expectations for only moderate upside from current levels.

- Risks emphasize exposure to North American and European cycles, potential oversupply in roofing and insulation, tariff and input cost pressure, and the need to retain contractor loyalty in a competitive market.

Once you are clear on which Owens Corning narrative feels closer to your own assumptions on revenue, margins and risk, you can use the Community tools to adapt those inputs and track how your personal fair value compares with the live share price over time. See what the community is saying about Owens Corning

Do you think there's more to the story for Owens Corning? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.