Owens Corning (OC) Stock Looks Overvalued With Shares Above Fair Value

Owens Corning OC | 0.00 |

Owens Corning stock has delivered a 66.0% return over the past five years, yet the current checks send mixed valuation signals, with the Discounted Cash Flow (DCF) intrinsic value suggesting the shares trade at a premium while market multiples look more forgiving.

- A 66.0% gain over five years suggests Owens Corning has already rewarded patient shareholders, so fresh buyers need to think carefully about the risk and reward from here.

- Recent unsolicited acquisition interest and policy support for new housing construction may support investor expectations for future cash flows, while any cooling in deal speculation or construction demand could quickly bring the focus back to what investors are paying today for those cash flows.

- With a valuation score of 3 out of 6, Owens Corning presents a mixed picture rather than a clear bargain or clear overvaluation on the broader checks.

For investors, the debate is whether Owens Corning at around US$142 already reflects the acquisition interest and housing tailwinds, or if the current price still leaves enough room above intrinsic value estimates to justify taking or keeping a position.

Is Owens Corning Getting Expensive on Cash Flow?

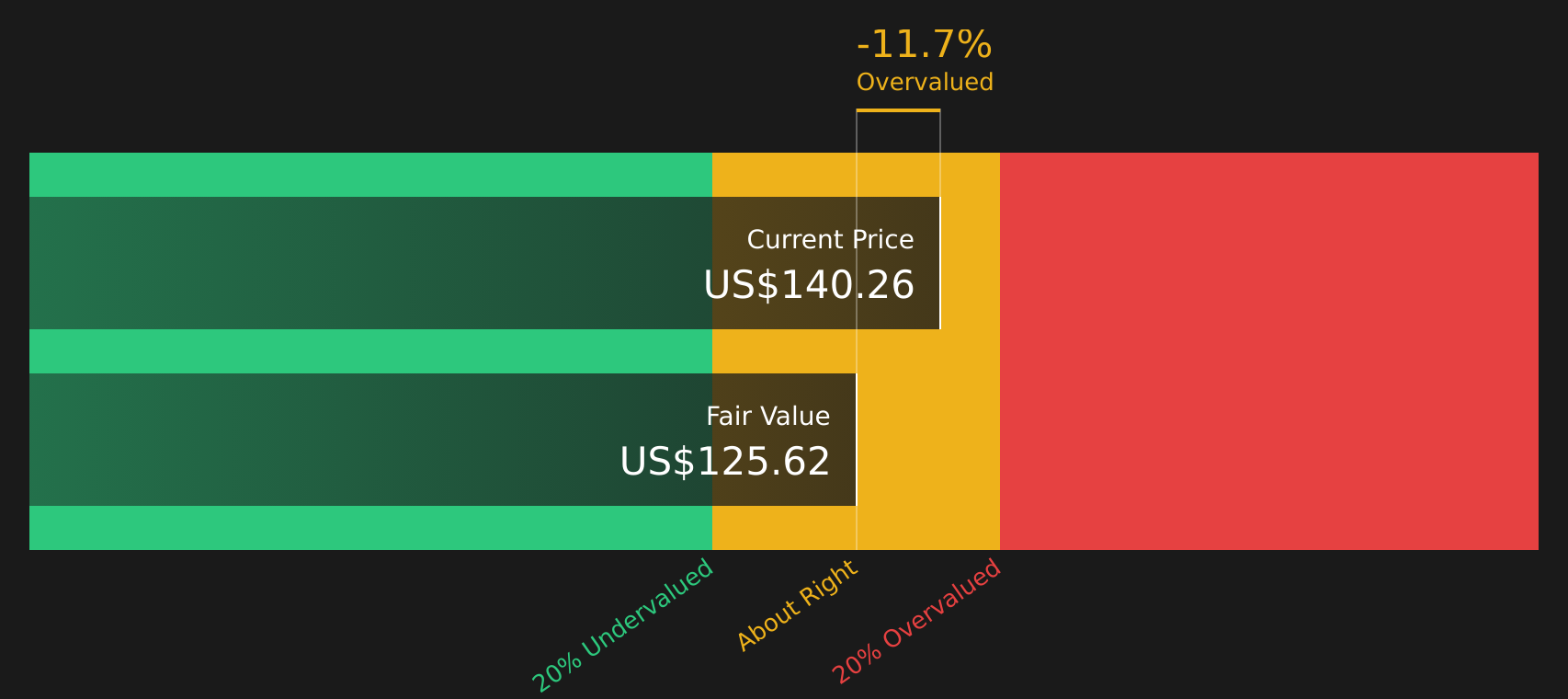

The Discounted Cash Flow (DCF) model values Owens Corning by projecting its future cash flows and discounting them back to today. On this method, the company’s latest twelve month free cash flow is about $991.5 million, with the model assuming a broadly declining path from current levels rather than rapid expansion.

Those cash flows translate to an estimated intrinsic value of about $127.61 per share, compared with the current share price around $142. This implies the stock screens roughly 11.5% overvalued on this framework. The surge in Owens Corning after unsolicited acquisition offers helps explain why the market price now sits above what the cash flow projections alone would support.

On these DCF assumptions, Owens Corning looks overvalued relative to its estimated intrinsic value.

Our Discounted Cash Flow (DCF) analysis suggests Owens Corning may be overvalued by 11.5%. Discover 45 high quality undervalued stocks or create your own screener to find better value opportunities.

Does Owens Corning Look Undervalued on Sales?

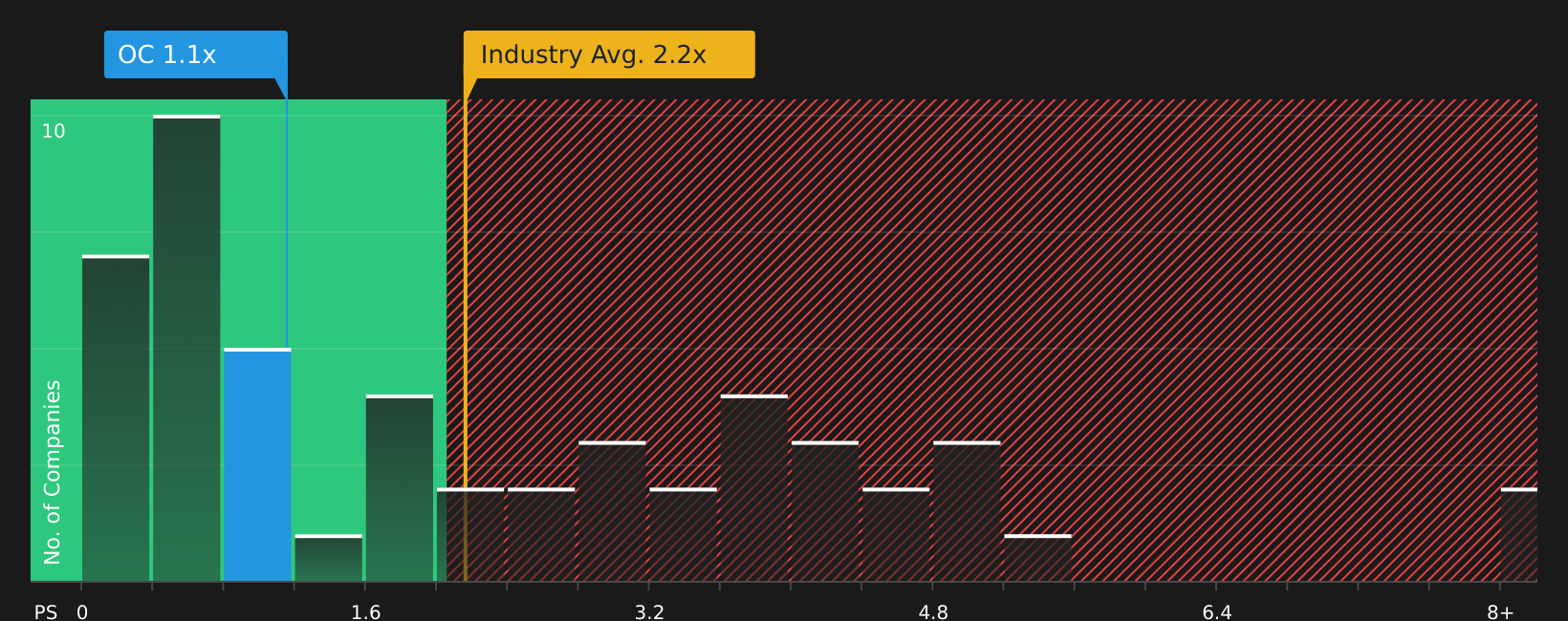

For a building materials company like Owens Corning, the P/S ratio gives a straightforward read on how the market is valuing each dollar of revenue.

Owens Corning currently trades on a P/S of about 1.2x, which is well below the Building industry average of roughly 2.2x and also below the peer group average around 3.3x. Based on Simply Wall St’s fair P/S estimate of about 1.9x, which reflects the company’s size, margins and risk profile, the current multiple sits at a clear discount to the level indicated by that model.

This difference suggests the recent interest in Owens Corning has not fully closed the valuation gap implied by revenue-based checks, even after the stock reaction to acquisition headlines and housing-related policy support.

On the P/S multiple, Owens Corning stock currently appears undervalued relative to both its industry and its modelled fair level.

The Owens Corning Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Owens Corning pick up where this valuation puzzle leaves off. They spell out which assumptions about Owens Corning's future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today’s price, and set out clear, testable theses about the business that you can watch over time rather than treating fair value as a one off snapshot, all hosted on Simply Wall St's Community page.

Owens Corning investors on the Simply Wall St Community are split between seeing the stock as roughly fairly priced and taking a more cautious view that it trades well above a bearish fair value scenario.

Bull case: roughly fairly valued

"Owens Corning's portfolio shift towards higher-margin, differentiated products and regions (divesting low-margin Asian businesses and glass reinforcements) is likely to improve consolidated operating margins and return on invested capital over time..."

Bear case: 29% overvalued

"However, ongoing cost inflation and required production curtailments could cap pricing power and compress EBITDA margins over the next several years..."

Do you think there's more to the story for Owens Corning? Head over to our Community to see what others are saying!

The Bottom Line

Owens Corning sits in a genuine valuation tug-of-war, with the Discounted Cash Flow (DCF) intrinsic value estimate pointing to the stock as overvalued while revenue-based multiples still frame it as undervalued against peers and a fair P/S marker. That split largely reflects different judgments about cash flow durability and capital needs on one side, and about how far growth expectations and sector sentiment can support a higher multiple on the other. For you, the real question is whether margins and cash generation can justify both the current price and any further re-rating in the face of inflation and potential production curtailments.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.