Permian Basin Royalty Trust (PBT) Stock Looks Rich After Its New Cash Distribution

Permian Basin Royalty Trust PBT | 0.00 |

Permian Basin Royalty Trust (PBT) has declared a June 2026 cash distribution of $0.024673 per unit, payable on July 15 to unit holders of record as of June 30, drawing fresh attention from income-focused investors.

The new distribution lands while Permian Basin Royalty Trust’s 1 month share price return is down 18.54%, even though its year to date share price return is 43.60% and 1 year total shareholder return is 113.50%. This suggests strong longer term momentum despite recent volatility.

If this payout has you thinking about other income or commodity ideas, it could be worth scanning opportunities among 33 elite gold producer stocks.

With Permian Basin Royalty Trust’s unit price down 18.54% over the past month but up 113.50% over the past year, investors are left with a simple question: is this a fresh income opportunity or is future growth already priced in?

Price-to-Earnings of 79.9x: Is It Justified?

With Permian Basin Royalty Trust last closing at $25.26, its current P/E of 79.9x places it at a much richer level than many investors might expect for an oil and gas royalty trust.

The P/E ratio compares the price you pay for each unit with the earnings attributed to that unit, so a higher figure usually reflects the market paying more for each dollar of profit. For a business like Permian Basin Royalty Trust that holds royalty interests rather than operating wells itself, this can sometimes reflect how the market views the durability and predictability of its cash flows.

At 79.9x earnings, PBT trades at a far higher level than both the US Oil and Gas industry average P/E of 12.9x and its peer average of 12.7x. This indicates that the current price embeds expectations that are much stronger than those reflected in these comparison groups.

Result: Price-to-Earnings of 79.9x (OVERVALUED)

However, investors in Permian Basin Royalty Trust still face risks such as commodity price swings and potential changes in production volumes that could affect future distributions.

Another View: What Our DCF Model Suggests

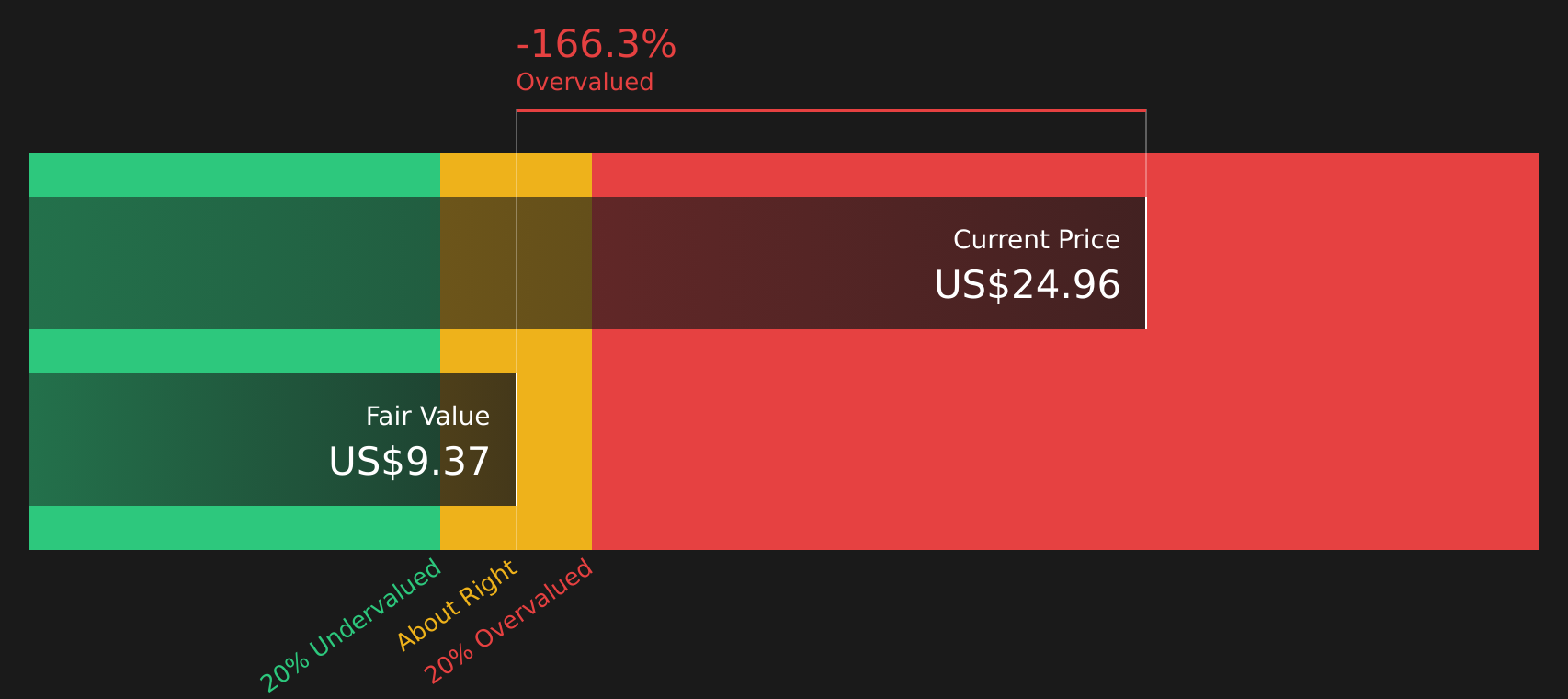

While the P/E ratio paints Permian Basin Royalty Trust as expensive, the SWS DCF model also points to a stretched valuation. At a unit price of $25.26 versus an estimated future cash flow value of $9.37, the units screen as overvalued using this second lens as well. If both methods flag a rich price, how comfortable are you paying a higher price for these royalties?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Permian Basin Royalty Trust for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Looking For More Investment Ideas Beyond Permian Basin Royalty Trust?

If Permian Basin Royalty Trust has sharpened your interest in income and value, do not stop here. The Simply Wall Street Screener can quickly surface other targeted opportunities.

- Target reliable payouts by focusing on companies identified as potential income standouts through the 7 dividend fortresses.

- Hunt for quality at a compelling price by scanning opportunities filtered by valuation and fundamentals using the 44 high quality undervalued stocks.

- Prioritize resilience by concentrating on companies with sturdier finances and lower assessed risk scores via the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.