Personalis (PSNL) Stock Looks Rich Even After A Very Large Run

Personalis PSNL | 0.00 |

Personalis stock has delivered a very large 3 year gain, yet the valuation checks still lean expensive, which puts the recent share price strength in tension with what the broader numbers suggest about value.

- Over the past 3 years, Personalis has returned roughly 5x, which is a very large move that raises the bar for what the current share price needs to justify.

- Future revenue growth and the path to stronger, more consistent cash flows can support today’s valuation. However, execution risks around profitability and funding needs may weigh on how much investors are willing to pay for that growth.

- Personalis passes 0 of 6 valuation checks, which means it does not screen as a clear bargain on Simply Wall St’s broader assessment of price versus fundamentals.

The issue now is whether the current price for Personalis leaves enough margin for error after such a strong multi year run.

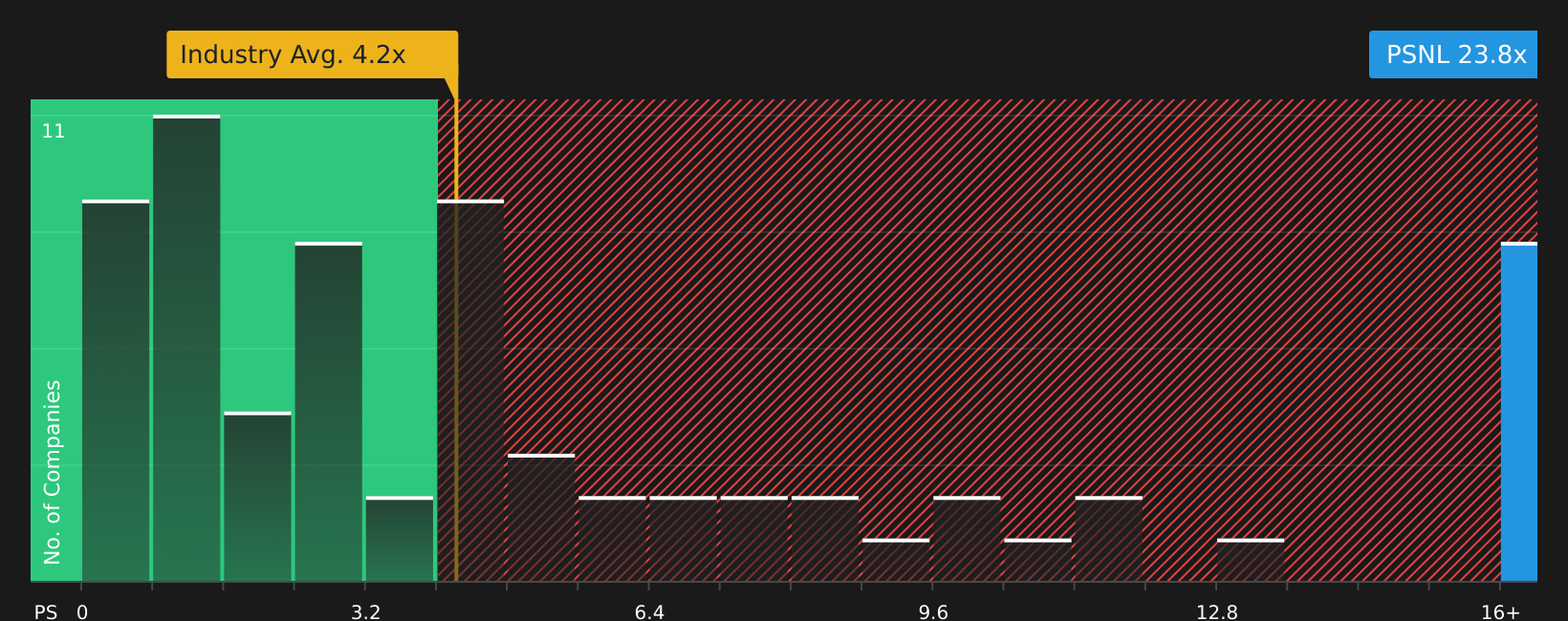

Does Personalis Look Pricey on Sales?

P/S is a useful lens for Personalis because the stock is still loss making, so revenue is the cleaner anchor than earnings. Personalis currently trades at a P/S of 22.9x, which is far above the Life Sciences industry average of 3.9x and also well above the peer group average of 8.9x. That alone suggests the market is placing a rich value on each dollar of Personalis revenue compared with many other stocks in the sector.

The Simply Wall St model indicates a fair P/S ratio of 4.2x for Personalis, and the gap to the current 22.9x is very wide. The framework is heavily penalising the company’s losses and risk profile, so this fair ratio is better read as a warning flag that the stock screens as very expensive on this measure, rather than a precise target. For anyone considering Personalis, the current P/S multiple implies a high bar for future execution to keep this valuation intact.

On the P/S multiple, Personalis stock currently screens as overvalued relative to both its sector and the modelled fair ratio.

The Personalis Narrative: What Would Justify Today's Price?

Simply Wall St Narratives take the valuation puzzle around Personalis and turn it into explicit scenarios that spell out what would need to happen to revenue, margins and earnings for the stock to be worth materially more or less than it is today, and they sit on the company’s Community page.

Instead of relying on a single multiple or model point estimate, each narrative lays out the assumptions behind its idea of fair value so you can compare those expectations with the actual results Personalis reports over time.

One of the top community narratives on Personalis: 57% overvalued

"Intensifying competition, regulatory pressures, and persistent operating losses risk constraining profitability and may force cost cuts or future shareholder dilution..."

Do you think there's more to the story for Personalis? Head over to our Community to see what others are saying!

The Bottom Line

For Personalis, the market multiple view points clearly to an overvalued stock, with a very wide gap between the current P/S and both its sector peers and the modelled fair ratio. That spread reflects how much optimism is already priced in around future revenue and margin progress, while the broader valuation checks remain weak. From here, the key question is whether Personalis can turn its high revenue multiple into a sustainable path toward stronger profitability, and whether it can do so quickly enough to keep investor confidence where it is today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.