Photronics (PLAB) Is Up 12.0% After Earnings Beat And Expansion Update - What's Changed

Photronics, Inc. PLAB | 40.49 39.80 | -0.88% -1.70% Pre |

- Recently, Photronics reported a strong quarter with revenue increasing 6.1% year on year, surpassing analyst estimates for both sales and earnings per share.

- Management also emphasized that facility expansion and efforts to broaden the company’s geographic revenue mix are progressing, reflecting how it is adapting its photomask business to a more regionally segmented semiconductor industry.

- With this earnings beat and reaffirmed progress on facility expansion, we’ll now examine how the update influences Photronics’ investment narrative.

Find 48 companies with promising cash flow potential yet trading below their fair value.

Photronics Investment Narrative Recap

To own Photronics, you need to believe that its global photomask footprint and technology upgrades can convert semiconductor and display complexity into durable earnings, despite cyclical swings. The latest earnings beat modestly supports the near term catalyst of capacity expansion, but does not remove key risks around geopolitics, customer concentration in Asia, and volatile quarterly demand.

The update on facility expansion timing is particularly relevant here, as it ties directly into Photronics’ push to extend advanced-node capabilities in the U.S. and Asia. Progress on these projects matters because they underpin the company’s ability to serve next generation IC and display customers, which could help offset regional demand uncertainty and justify the heavy capital spending already committed.

However, investors should also be aware that rising capital expenditures and regional trade tensions could still weigh on returns if...

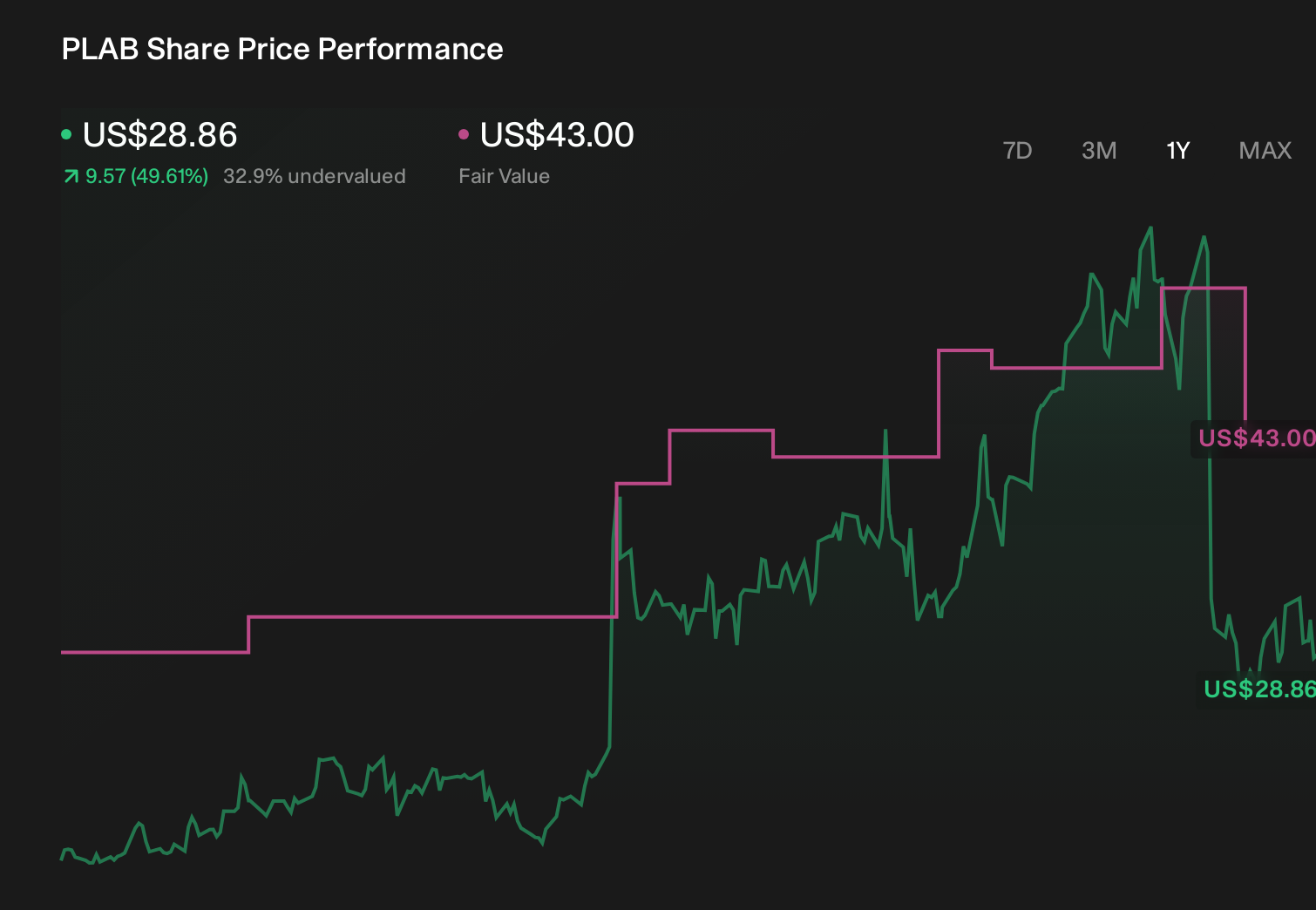

Photronics' narrative projects $950.2 million revenue and $131.6 million earnings by 2028. This requires 3.5% yearly revenue growth and a $23.1 million earnings increase from $108.5 million today.

Uncover how Photronics' forecasts yield a $48.00 fair value, a 30% upside to its current price.

Exploring Other Perspectives

Eight fair value estimates from the Simply Wall St Community span roughly US$19 to US$48 per share, showing how far apart individual views can be. When you set those opinions against Photronics’ ongoing facility expansion as the key catalyst, it becomes even more important to compare several perspectives before deciding how this business might fit into your portfolio.

Explore 8 other fair value estimates on Photronics - why the stock might be worth 48% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Photronics research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Photronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Photronics' overall financial health at a glance.

Searching For A Fresh Perspective?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 28 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.