Plains GP Holdings (PAGP) Stock Valuation Check After Strong Multi‑Year Returns

Plains GP Holdings LP Class A PAGP | 0.00 |

Recent share performance and business snapshot

Plains GP Holdings (PAGP) has seen relatively steady trading recently, with the stock roughly flat over the past week and showing positive returns over the past month and past 3 months.

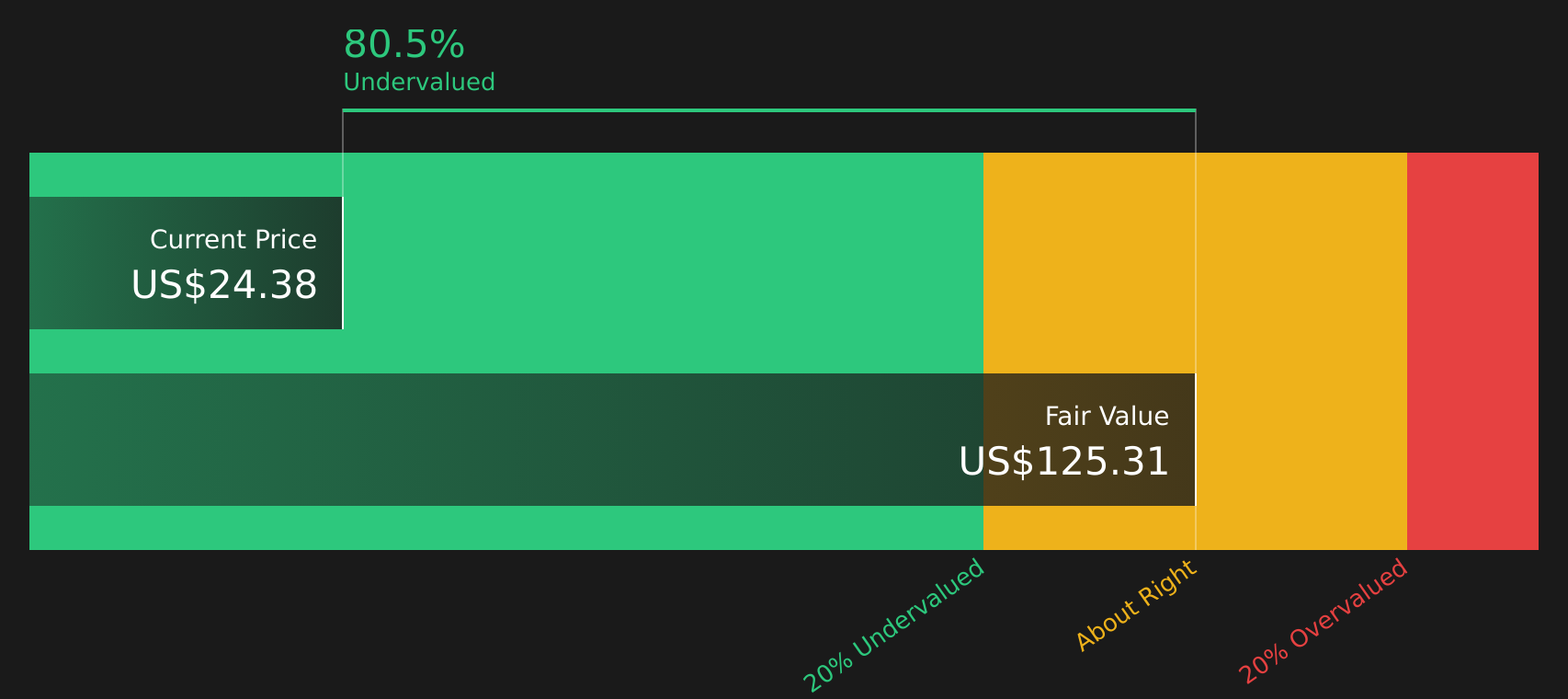

The company has a market value of about US$5.7b and last closed at US$24.38. Returns over the past year and longer periods indicate that the stock has already delivered meaningful gains for existing holders.

Plains GP Holdings operates midstream energy infrastructure through its crude oil and natural gas liquids segments, generating revenue primarily from gathering, transport, storage and related services across the United States and Canada.

At the current share price of US$24.38, Plains GP Holdings has paired a firm year to date share price return of 25.61% with a 1 year total shareholder return of 37.36%. This points to momentum that has been building over several years, as reflected in the 3 year and 5 year total shareholder returns of 116.95% and 206.05% respectively.

If midstream energy has your attention, it can be helpful to widen the lens and see what is happening across the wider infrastructure and grid space using the 35 power grid technology and infrastructure stocks

With a recent intrinsic value estimate suggesting the shares might trade at about an 80.56% discount, yet sitting just above the average analyst price target, is Plains GP a genuine opportunity or already priced for future growth?

Most Popular Narrative: 8% Overvalued

Against the latest fair value estimate of $22.57, Plains GP Holdings' last close at $24.38 reflects a premium that the most followed narrative treats as fully embedding bullish expectations.

The planned divestiture of the NGL segment and redeployment of ~$3 billion in proceeds into core crude oil operations and bolt-on acquisitions are expected to streamline operations, reduce commodity price exposure, and enhance financial flexibility, supporting growth in core revenue and improved net margins via higher-return investments and potential buybacks.

Curious what kind of revenue path, margin lift, and future earnings multiple are baked into that fair value math? The narrative leans on specific growth, profitability and valuation assumptions that could surprise you once you see them side by side.

Result: Fair Value of $22.57 (OVERVALUED)

However, tighter environmental rules or weaker long term crude demand could reduce throughput and pressure margins, which would challenge the assumptions behind that 8% overvaluation call.

Another angle on value: cash flows vs market signals

The analyst narrative treats Plains GP Holdings as about 8% overvalued against a fair value of $22.57, but the Simply Wall St DCF model points in the opposite direction, with a future cash flow value estimate of $125.42 and the shares trading at a very large discount to that figure. With such a wide gap between earnings based targets and cash flow based value, which signal do you treat as more credible for your own thesis?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Plains GP Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mix of optimism and concern in this story is clear, and the market will not wait while you make up your mind. To weigh those signals for yourself and see what stands out most, start with the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Plains GP Holdings has sharpened your thinking, do not stop here. Broaden your watchlist and let the data surface other stocks that fit your style.

- Target potential upside with companies that pair quality fundamentals with attractive pricing by running the 44 high quality undervalued stocks.

- Focus on income by scanning for companies with sturdy payouts and higher yields using the 8 dividend fortresses.

- Prioritise resilience by filtering for companies that show strong financial footing through the solid balance sheet and fundamentals stocks screener (48 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.